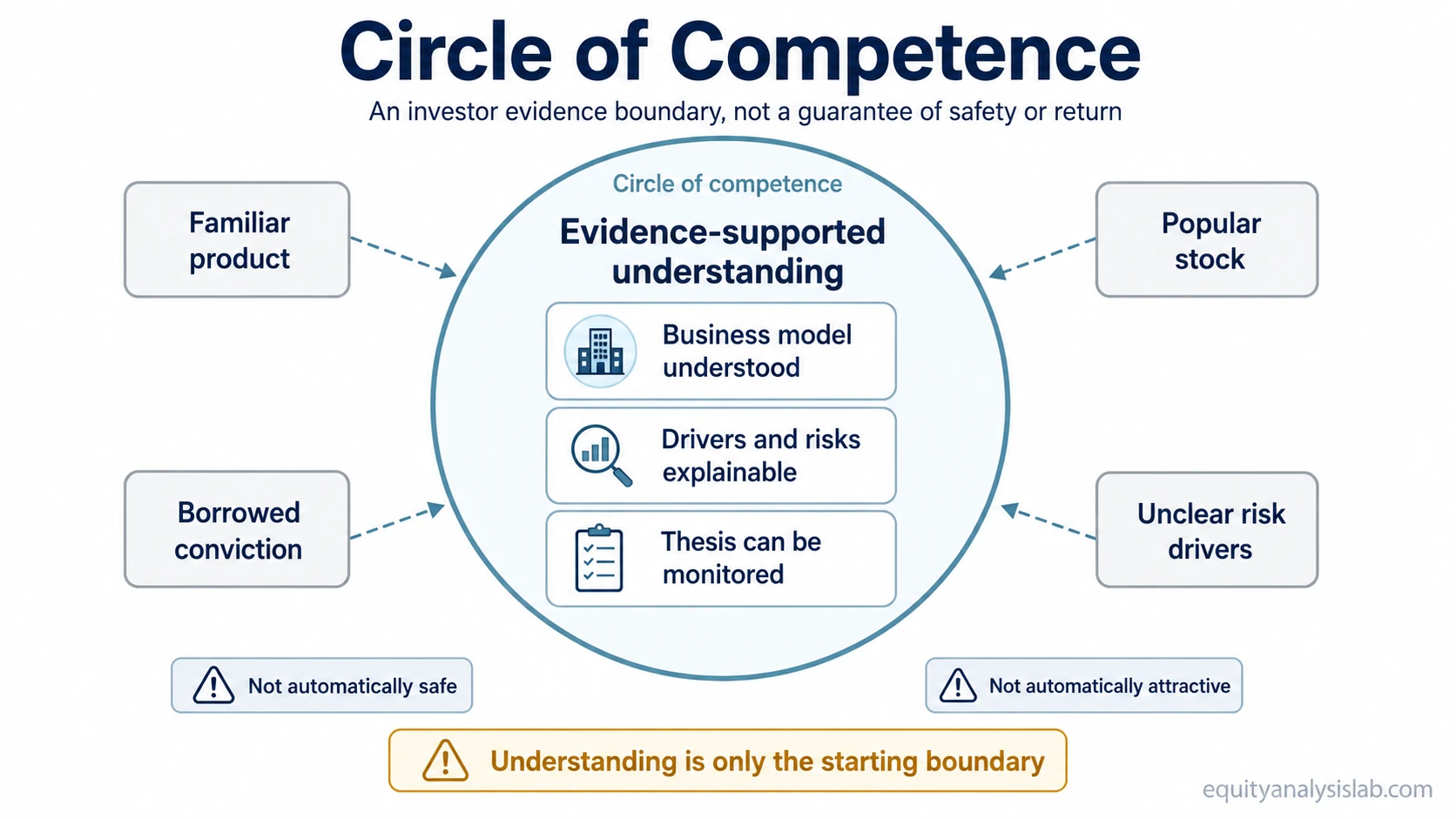

A circle of competence is the boundary around the businesses, industries, financial statements, risks, and decision factors an investor can understand well enough to evaluate with evidence. It is not a list of favorite companies or familiar products. It separates analysis that can be supported from uncertainty that is mostly being guessed.

For investors, the concept starts with a basic question: can the investor understand what drives the outcome? When that answer is weak, valuation, risk tolerance, and confidence cannot fully solve the problem. The investor may not yet have enough context to judge the business independently.

What Is a Circle of Competence?

Circle of competence: the range of businesses, industries, financial concepts, and risk factors an investor can understand, analyze, and monitor with enough evidence to make a reasoned judgment.

The term is commonly associated with the investing tradition around Warren Buffett and Charlie Munger, but the useful point is not biography. The useful point is the boundary. A business can be well known, widely owned, or easy to recognize and still sit outside an investor’s analytical competence if the investor cannot explain how it earns money, what could damage the thesis, and which evidence would change the view.

A circle of competence is not about appearing knowledgeable. It is about knowing where judgment is strong enough to be useful and where the investor should slow down, study more, or avoid treating familiarity as understanding.

Why Circle of Competence Matters for Investors

Circle of competence changes the investor’s process before the investor reaches a valuation conclusion. It asks whether the business can be evaluated in the first place. If the business model, accounting drivers, industry economics, competitive position, or main risks cannot be explained in plain terms, any valuation may rest on weak assumptions.

This does not mean an investment inside a circle of competence is automatically attractive. It only means the investor has a better chance of knowing what is being analyzed. A company can be understandable and still be overpriced, low quality, fragile, or unsuitable for the investor’s situation.

The concept also helps separate analytical limits from emotional comfort. An investor may feel comfortable owning a familiar brand while still lacking the ability to evaluate the economics behind that brand. The opposite can also happen: an investor may understand a business clearly but still decide that the risk, valuation, or portfolio role does not fit.

The Competence Boundary Test

A practical way to use the concept is to test whether the investor can explain the business, the evidence, and the failure conditions without relying on vague confidence. The purpose is not to prove expertise. It is to locate the edge of the circle before the decision becomes a guess.

| Question | What it tests | If the answer is weak, what it means |

|---|---|---|

| Can I explain how the business makes money? | Business model understanding | The investment may be familiar, but the economics are not yet clear. |

| Can I identify the main drivers of revenue, margins, cash flow, and capital needs? | Financial statement interpretation | The analysis may depend on surface-level metrics rather than underlying economics. |

| Can I name the most important risks that could damage the thesis? | Risk recognition | The investor may be seeing upside more clearly than failure conditions. |

| Can I explain what evidence would change my view? | Thesis discipline | The position may be driven by attachment, narrative, or outsourced conviction. |

| Can I compare the business with relevant alternatives? | Industry and competitive context | The investor may understand the company in isolation but not its competitive setting. |

| Can I monitor the thesis after purchase? | Ongoing evidence quality | The investor may be able to enter the idea but not evaluate whether the thesis is improving or weakening. |

The test is intentionally simple. If several answers are weak, the investment is not automatically bad. The more precise conclusion is that the investor may not yet have enough competence to judge it independently.

What Falls Outside a Circle of Competence?

Something falls outside a circle of competence when the investor cannot connect the investment idea to evidence. The boundary is crossed when the investor relies mainly on reputation, popularity, product use, borrowed conviction, or a simplified story that cannot be tested.

Common mistake: treating product familiarity as investment competence. Using a product, liking a brand, or seeing a company in daily life can create useful curiosity, but it does not automatically explain margins, capital intensity, dilution risk, cyclicality, competitive pressure, or valuation.

Outsourced conviction is another warning sign. Reading a strong thesis from another investor may help the learning process, but it does not put the idea inside the investor’s own circle of competence unless the investor can explain the assumptions and monitor whether they remain valid.

Overconfidence can make the boundary harder to see. The investor may understand one part of a business and then assume the rest is equally clear. A narrow area of knowledge should not be stretched into broad certainty.

A Simple Investor Scenario

An investor may understand a mature retailer because the revenue model, store economics, margins, inventory risk, and competitive pressures are relatively clear to them. The same investor may not understand a specialized biotechnology company, even if the stock is popular, because the outcome depends on clinical, regulatory, and scientific factors they cannot evaluate independently.

This comparison does not rank one company above the other. It shows that the investor’s ability to evaluate evidence can differ sharply across businesses. Circle of competence is a boundary around understanding, not a ranking of investment opportunities.

Circle of Competence vs Related Investor Concepts

Circle of competence is part of investor orientation, but it should not absorb nearby concepts. It answers a different question from goals, policy rules, financial ability to absorb risk, and emotional comfort with uncertainty.

| Concept | Main question | How it differs from circle of competence |

|---|---|---|

| Investment objectives | What is the investor trying to achieve? | Objectives define the purpose of capital; circle of competence defines what the investor can evaluate with evidence. |

| Investment policy statement | What rules guide the investor’s process? | An IPS can document boundaries and rules, but circle of competence is the understanding boundary itself. |

| Ability to financially absorb risk | How much risk can the investor’s financial situation bear? | Risk capacity is about financial resilience; circle of competence is about analytical understanding. |

| Emotional tolerance for risk | How much uncertainty can the investor tolerate emotionally? | Risk tolerance is about comfort with volatility or loss; circle of competence is about whether the investor understands what they own. |

| Investment goals | What milestones or needs should the plan serve? | Goals describe desired outcomes; circle of competence describes the boundary of analyzable decisions. |

Can an Investor Expand a Circle of Competence?

An investor can expand a circle of competence, but expansion should come from study, repetition, and evidence rather than confidence alone. Reading financial statements, learning industry economics, comparing companies, reviewing past mistakes, and tracking how assumptions change over time can gradually make a subject more analyzable.

The safest expansion is usually deliberate and narrow. Learning one business model deeply is different from assuming that knowledge transfers to every company in the same sector. The boundary moves when the investor can explain the drivers, risks, and evidence more clearly than before.

Common Misuse

Misuse warning: circle of competence does not prove that an investment is high quality, undervalued, safe, or likely to produce a good return. It only describes whether the investor is operating in an area they can understand and evaluate.

The concept can also be misused as an excuse not to learn. Staying inside a circle of competence is useful when it prevents careless guessing. It becomes limiting when the investor treats today’s knowledge boundary as permanent and never builds the ability to analyze new areas.

A stronger use is to separate three decisions: what the investor can understand, whether the investment is attractive, and whether it fits the investor’s broader process. Those decisions are related, but they are not the same.

FAQ

Is circle of competence the same as risk tolerance?

No. Circle of competence is about what an investor can understand and evaluate with evidence. Risk tolerance is about how much uncertainty, volatility, or potential loss the investor can emotionally tolerate.

Can an investor expand a circle of competence?

Yes. It can expand through focused study, repeated analysis, industry comparison, financial statement work, and honest review of mistakes. Confidence alone does not expand it.

Does staying within a circle of competence make an investment safe?

No. It only means the investor is more likely to understand what is being evaluated. A business can be understandable and still be risky, overvalued, low quality, or unsuitable for the investor’s objectives.