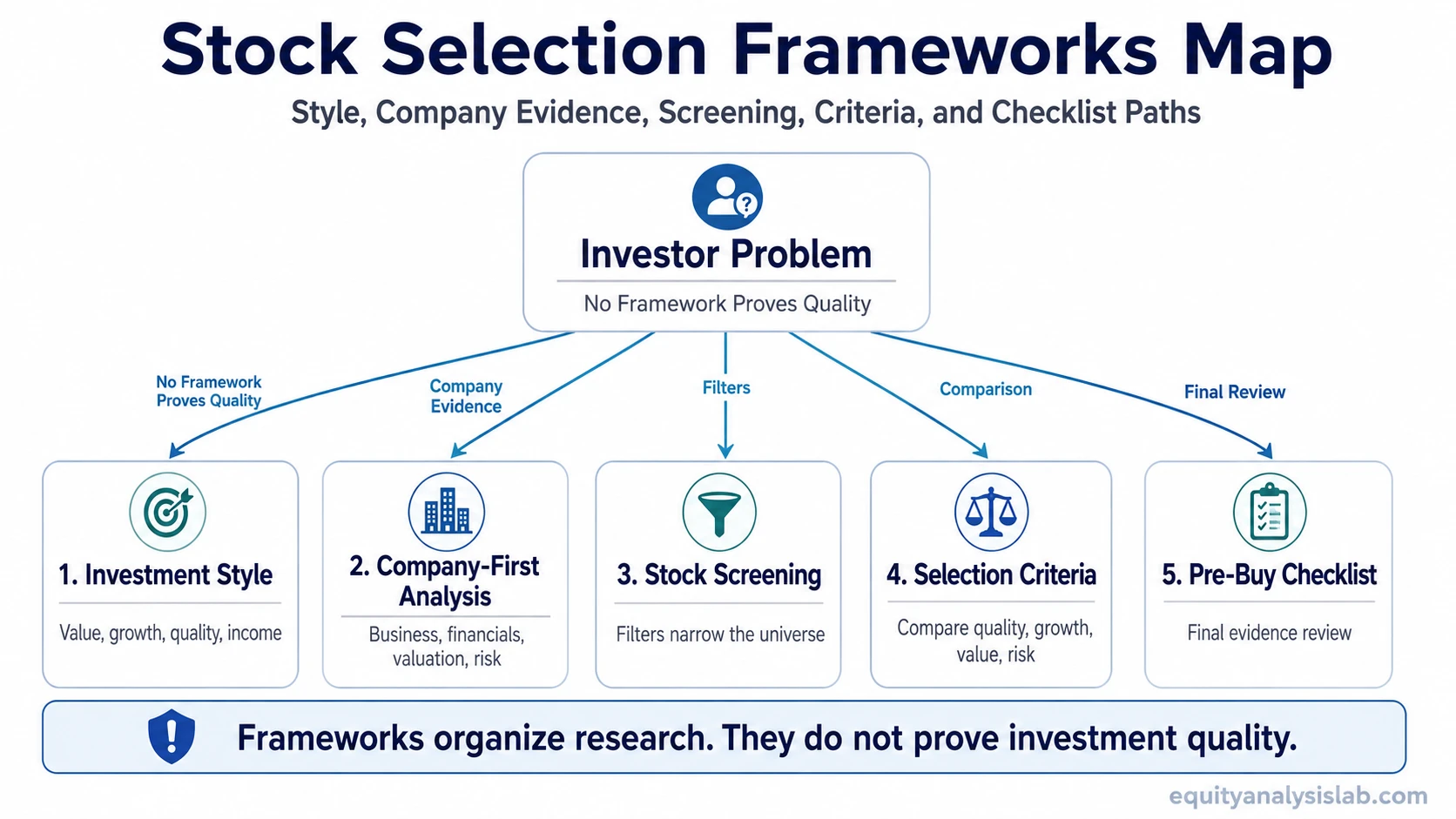

Stock selection frameworks are organized ways to narrow the equity universe, compare companies, and decide which deeper research process fits the investor’s objective.

The useful first choice is not one universal formula. It is deciding whether the next step should be an investment style, bottom-up company analysis, measurable screening, selection criteria, or a pre-buy checklist.

No framework removes uncertainty. A structured process can help investors ask better questions, but it cannot prove that a stock is attractive by itself.

Key Points

- Stock selection frameworks organize how investors narrow and compare stocks.

- Different frameworks answer different questions: style, company quality, measurable filters, or pre-buy review.

- A stock screener can narrow candidates, but it does not replace fundamental analysis.

- Bottom-up investing starts with company evidence rather than market themes.

- No framework removes valuation risk, business-model risk, or evidence-quality risk.

Choose a Framework by Investor Problem

A stock selection framework is most useful when it starts with the right problem. Some investors need a style category. Others need a way to screen a large universe, compare company evidence, or test whether a thesis is mature enough for deeper review.

| Reader problem | Better framework path | What it helps with | Main limitation | Suggested path |

|---|---|---|---|---|

| You need to choose the broad lens for comparing stocks. | Investment-style framework | Separates value, growth, quality, income, GARP, and other style-led approaches. | A style label does not prove that a company is attractive at the current price. | Investment styles |

| You want to start from company evidence rather than a market theme. | Company-first framework | Focuses on business quality, financial statements, valuation, management, and risk. | Company depth takes more work than a simple screen or style label. | bottom-up investing approach |

| You are starting with too many possible stocks. | Screening framework | Uses measurable filters to reduce a large universe into a smaller research list. | Screens can miss qualitative risk, accounting quality, and business-model durability. | stock screener |

| You need to compare candidates using repeatable criteria. | Criteria and comparison framework | Turns stock selection into a more consistent review of valuation, quality, growth, risk, and financial strength. | Criteria can become mechanical if they are not interpreted in context. | Screening and comparison |

| You already have a candidate and need a final review structure. | Checklist framework | Helps test whether the thesis, risks, valuation, and evidence quality have been reviewed. | A checklist can reduce omissions, but it cannot make a weak thesis strong. | Use after the relevant style, screening, and company-analysis path is clear. |

How Stock Selection Frameworks Differ

Stock selection frameworks differ by the kind of evidence they prioritize. A style-led framework starts with the type of opportunity an investor wants to study. A company-first framework starts with the business itself. A screening framework starts with measurable filters. A checklist framework tests whether enough evidence has been reviewed before moving further.

When timing or price behavior enters the discussion, technical analysis vs fundamental analysis helps separate market-behavior evidence from business, valuation, and economic evidence.

Investment-style path: Start here when the first question is what kind of stock belongs in the research universe. Value, growth, quality, income, and GARP lenses can help organize expectations, but each still needs company-level evidence.

Company-first path: This path begins with the business, not the screen. It usually emphasizes financial statements, earnings quality, cash flow, competitive position, valuation, and company-specific risk.

Screening and criteria path: Use this path when the starting universe is too large. Filters can sort for valuation, profitability, growth, leverage, margins, liquidity, or other measurable traits.

Checklist path: This fits after a stock has already passed an initial review. It checks whether the thesis, valuation, risks, and evidence quality have been examined clearly enough for deeper work.

Quantitative stock selection belongs inside this broader map, but it is not the whole topic. Ranking models, factor screens, and scoring systems can be useful, but they depend on input quality, factor choice, time period, liquidity, turnover, and whether the model is being used as a research filter or as an investment rule.

Screening, Selection, and Checklist Boundaries

Screening, selection, and checklist review are often treated as one process, but they answer different questions. Keeping the boundary clear helps prevent a simple filter from being mistaken for complete investment analysis.

| Stage | Question it answers | Useful output | What it cannot prove |

|---|---|---|---|

| Screening | Which stocks are worth looking at first? | A smaller research list. | That any company on the list is a good investment. |

| Selection | Which candidates have stronger evidence? | A comparison across quality, valuation, growth, risk, and financial strength. | That the investment outcome will be favorable. |

| Checklist review | Has the thesis been tested against the main risks? | A more disciplined final review before deeper action. | That a stock is sufficient on its own. |

A reader comparing profitable but slow-growing companies may need a value or quality path, while a reader starting from a large universe of stocks may first need screening criteria. The framework choice depends on the question being asked, not on a universal ranking of methods.

When a Framework Helps and When It Can Mislead

A framework helps when it makes the research process more explicit. It can force the investor to identify the evidence being used, the risks being ignored, and the area that deserves deeper review.

A framework can mislead when it becomes a shortcut. A cheap-looking stock can be a value trap if the business is deteriorating. A strong screen can miss customer concentration, accounting quality, cyclicality, dilution, or weak cash conversion. A quantitative ranking can look precise while still depending on stale inputs, overfitted factors, or poor assumptions.

Technical analysis can appear as secondary timing or context for some investors, but it should not dominate this Equity Analysis Lab page. The core job here is investor-oriented stock selection, not trading setup design, entry timing, exits, or signals.

Investment-Style and Company-First Paths

Use the style path when the first decision is the kind of company or opportunity being studied. A style lens can separate value, growth, quality, income, and GARP ideas, but it should not replace business analysis.

Use the company-first path when the investor wants to build the analysis from the business upward. That path is better suited to questions about revenue quality, margins, cash flow, balance-sheet strength, competitive advantage, management decisions, valuation, and risk.

The main distinction is sequence. A style framework begins by classifying the opportunity. A company-first framework begins by examining the company and then deciding whether any style label is justified.

Screening and Criteria Paths

Use the screening path when the first job is to reduce a broad universe into a smaller candidate list. This is where measurable filters, ratios, growth metrics, profitability thresholds, leverage limits, and valuation ranges can help.

Use the criteria path when the question has moved from “what should I look at?” to “how should I compare candidates?” At that stage, the process needs interpretation, not only numbers. A company can pass a valuation filter and still fail a quality, durability, or risk review.

The strongest use of screening is usually as a starting point. It can show where to look, but deeper selection still needs company analysis, valuation context, and risk assessment.

Suggested Starting Points

For a style-led starting point, begin with investment styles and use that path to separate the major families of stock selection. For a company-first approach, move into bottom-up investing and build the analysis from business evidence.

For measurable filters, use the stock screener path first, then move into screening and comparison when the candidate list needs interpretation. The goal is to keep each tool in its proper role: style for orientation, screening for narrowing, company analysis for evidence, and checklist review for discipline.

FAQ

What are stock selection frameworks?

Stock selection frameworks are structured ways to narrow, compare, and review stocks. They can be based on investment style, company analysis, measurable screening criteria, or checklist-based thesis review.

Is a stock screener the same as a stock selection framework?

No. A stock screener is usually one tool inside a broader framework. It can reduce a large universe into a smaller research list, but it does not replace company analysis, valuation judgment, or risk review.

Which stock selection framework is best?

No single framework is best in all conditions. The better choice depends on the investor’s objective, time horizon, evidence needs, and whether the starting point is style, company fundamentals, screening data, or checklist review.

Can stock selection criteria prove investment quality?

No. Criteria can make comparison more consistent, but they cannot prove investment quality on their own. Valuation risk, business-model risk, accounting quality, and forward uncertainty still need separate review.