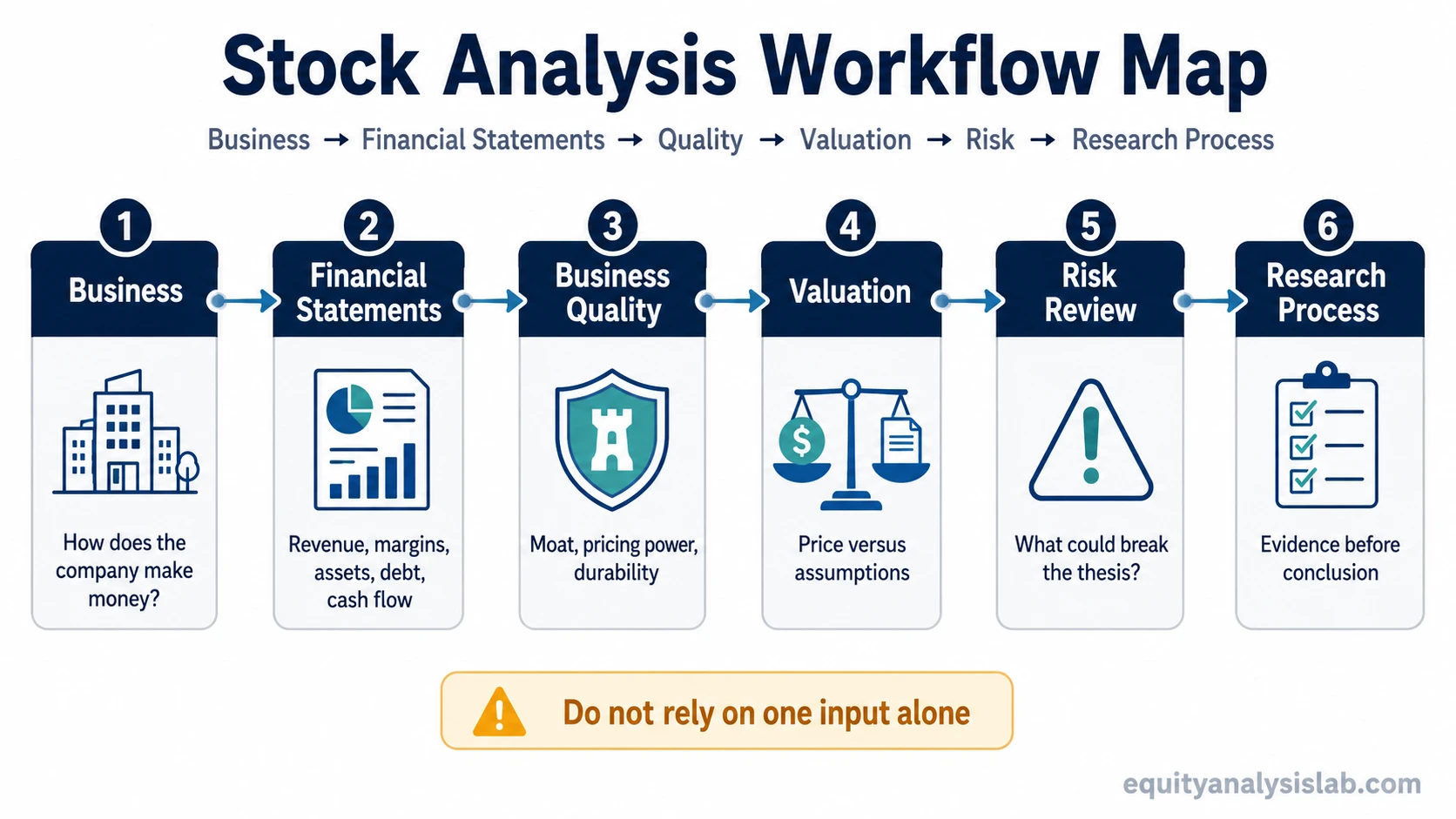

How to analyze a stock: start by understanding the business, then review the financial statements, cash flow, valuation, risks, and research evidence before forming an investor view.

A common beginner mistake is treating one input as the whole analysis. A chart, headline, low valuation ratio, strong story, or social-media claim can create interest, but none of them can show whether the company is financially sound, competitively durable, reasonably valued, and exposed to manageable risks.

A stronger stock analysis process moves from business reality to financial evidence, then to valuation and risk. Technical timing can be useful later, but it should not replace company analysis when the goal is to understand a stock as an investment.

Key Points

- Stock analysis begins with the company, not only with the ticker symbol or recent price movement.

- Financial statements show revenue, margins, assets, liabilities, cash generation, and funding pressure.

- Business quality helps separate a durable company from a company with only a strong narrative.

- Valuation is an assumption framework, not a standalone investor conclusion.

- Risk review should look for thesis breakers before any investor conclusion is formed.

How to Analyze a Stock Step by Step

The basic sequence is simple: understand what the company does, check the financial statements, evaluate business quality, compare valuation with evidence, identify the main risks, and place the conclusion inside a repeatable process.

| Step | Question to answer | Why it matters |

|---|---|---|

| Business model | How does the company make money? | Revenue quality is easier to judge when the source of revenue is clear. |

| Financial statements | What do revenue, margins, debt, and cash flow show? | Financial evidence tests whether the story is supported by numbers. |

| Business quality | Does the company have durable advantages or weak economics? | Quality affects how much confidence an investor can place in future assumptions. |

| Valuation | What expectations are already reflected in the price? | A good business can still be a poor investment if the price assumes too much. |

| Risk | What could break the thesis? | Risk review prevents a one-sided conclusion from becoming overconfident. |

| Research process | What evidence should be checked before deciding? | A repeatable process reduces the chance of reacting to noise. |

Start With the Business, Not Just the Ticker

A stock represents ownership in a business. Before reviewing ratios or price action, identify what the company sells, who pays it, which costs matter most, and what drives growth or decline.

Useful first questions include: Is revenue recurring or cyclical? Are customers concentrated or diversified? Does growth require heavy reinvestment? Are margins stable, improving, or weakening? A stock story becomes more useful only when it can be connected to these business drivers.

The goal is not to decide quickly whether the company is “good” or “bad.” The goal is to understand what would need to be true for the business to become more valuable, less valuable, or more uncertain over time.

Review the Financial Statements

Financial statements convert the business story into evidence. They show whether revenue growth is profitable, whether profits convert into cash, and whether the company is carrying financial pressure that could limit future flexibility.

- Revenue, margins, and earnings show how sales flow through the business and whether profitability is improving or deteriorating.

- The balance sheet shows assets, liabilities, debt, liquidity, and the financial cushion available to the company.

- The cash-flow statement helps test whether accounting profits are supported by actual cash generation.

For a first pass, avoid reading one statement in isolation. A company can show rising earnings while cash flow weakens, or revenue growth while the balance sheet becomes more fragile. The statements need to be read together.

Check Business Quality and Competitive Position

Business quality asks whether the company has durable economics or only temporary momentum. Strong revenue growth is less useful if the company lacks pricing power, depends on one product, faces heavy competition, or needs constant capital to defend its position.

An economic moat is one way to think about durable competitive advantage, but it should be supported by evidence such as customer retention, switching costs, cost advantages, network effects, brand strength, scale, or superior unit economics.

Management and capital allocation also matter. A company can create value through disciplined reinvestment, debt reduction, acquisitions, dividends, or buybacks, but those choices should be judged against cash flow, balance-sheet strength, and the price paid for capital decisions.

Compare Valuation With the Evidence

Valuation connects the company’s evidence to the stock price. A low multiple does not automatically mean the stock is cheap, and a high multiple does not automatically mean it is expensive. A structured how to value a stock process helps compare the market price with the assumptions behind growth, margins, cash flow, and risk.

Simple ratios such as price-to-earnings, price-to-sales, and enterprise value to EBITDA can help create a first comparison, but they need context. A company with weak margins, declining cash flow, or heavy debt may deserve a lower multiple than a stronger peer.

For deeper work, cash-flow-based valuation can help connect future assumptions to an estimated value range. The useful point is not to produce a precise number. The useful point is to see which assumptions drive the conclusion.

That estimated value range should still be treated as conditional. Intrinsic value depends on the quality of the assumptions behind it, especially revenue durability, margin stability, reinvestment needs, discount rate, and terminal expectations.

Identify Risks and Thesis Breakers

Risk review should happen before confidence builds. A stock analysis is incomplete if it only explains the upside case and ignores what could make the thesis wrong.

| Risk area | What to check | Why it can change the conclusion |

|---|---|---|

| Debt and liquidity | Maturity schedule, interest expense, leverage, and available cash | Financial pressure can limit reinvestment or force unfavorable decisions. |

| Margins | Gross margin, operating margin, input costs, and pricing power | Growth can become less valuable if profitability is weakening. |

| Cash flow | Operating cash flow, capital expenditure, and free cash flow direction | Weak cash conversion can make reported earnings less useful. |

| Dilution | Share count, stock compensation, convertibles, and capital raises | Business growth may not fully benefit shareholders if ownership is diluted. |

| Customer or product concentration | Reliance on one customer, product, region, or supplier | A narrow revenue base can make the company more fragile. |

| Valuation assumptions | Growth, margins, discount rate, terminal value, and multiple expectations | A small change in assumptions can materially change the valuation view. |

Analysis can reduce confusion, but it does not remove uncertainty. The best use of risk review is to identify what must remain true for the investment thesis to stay intact.

Avoid Common Beginner Stock Analysis Mistakes

Many weak stock conclusions begin with the wrong starting point. The issue is not that charts, ratios, stories, or investor discussions are useless. The issue is treating any one of them as enough.

| If the analysis starts with… | What to check next | Better next step |

|---|---|---|

| A price move or chart setup | Business evidence and financial statements | Test whether the company evidence supports the price interest. |

| A strong story | Cash flow, margins, debt, and risk factors | Separate narrative from measurable financial support. |

| A low P/E or cheap-looking valuation | Assumptions, durability, and valuation method | Ask whether the low price reflects risk, decline, or temporary pessimism. |

| A popular social-media claim | Filings, reports, and independent research | Use outside claims as prompts to verify, not as conclusions. |

| A “great company” label | Competitive advantage and price paid | Check whether quality is already fully reflected in the stock price. |

Turn the Analysis Into a Research Process

A stock analysis becomes more useful when the same sequence can be repeated across companies. That does not mean every company should be judged with identical numbers. It means the investor should know which evidence was checked, which assumptions were made, and which risks would change the conclusion.

A repeatable research workflow can organize the work into stages: business understanding, financial statement review, quality assessment, valuation, risk review, source verification, and decision documentation.

Technical analysis can still have a secondary role for investors who use it to study timing, trend behavior, or market reaction. It should be kept separate from business quality. A better-looking chart does not repair weak fundamentals, and a weaker chart does not automatically disprove a durable company.

What Good Stock Analysis Does Not Do

Good analysis does not guarantee returns, identify the best stock, or remove the possibility of being wrong. It also does not turn a valuation estimate into a certain outcome.

Its practical value is narrower and more useful: it clarifies what the company does, what the financial evidence shows, what expectations are reflected in the stock price, what could break the thesis, and what additional research is needed before forming a decision.

FAQ

What is the first step in analyzing a stock?

The first step is to understand the business. Identify how the company makes money, what drives revenue, who its customers are, and which costs or risks could affect future results.

Which financial statements should be reviewed?

Review the income statement, balance sheet, and cash-flow statement together. The income statement shows revenue and profitability, the balance sheet shows financial position, and the cash-flow statement shows cash generation and cash use.

Is valuation enough to form an investor view?

No. Valuation needs to be compared with business quality, growth durability, balance-sheet risk, cash flow, and the assumptions behind the valuation. A low-looking valuation can still be risky if the business evidence is weak.

Should technical analysis be part of stock analysis?

Technical analysis can be used as a secondary timing or market-behavior lens, but it should not replace business analysis, financial statement review, valuation, and risk assessment.

Can stock analysis predict future returns?

No. Stock analysis can improve understanding of a company, valuation, and risk, but it cannot predict returns with certainty or eliminate uncertainty.