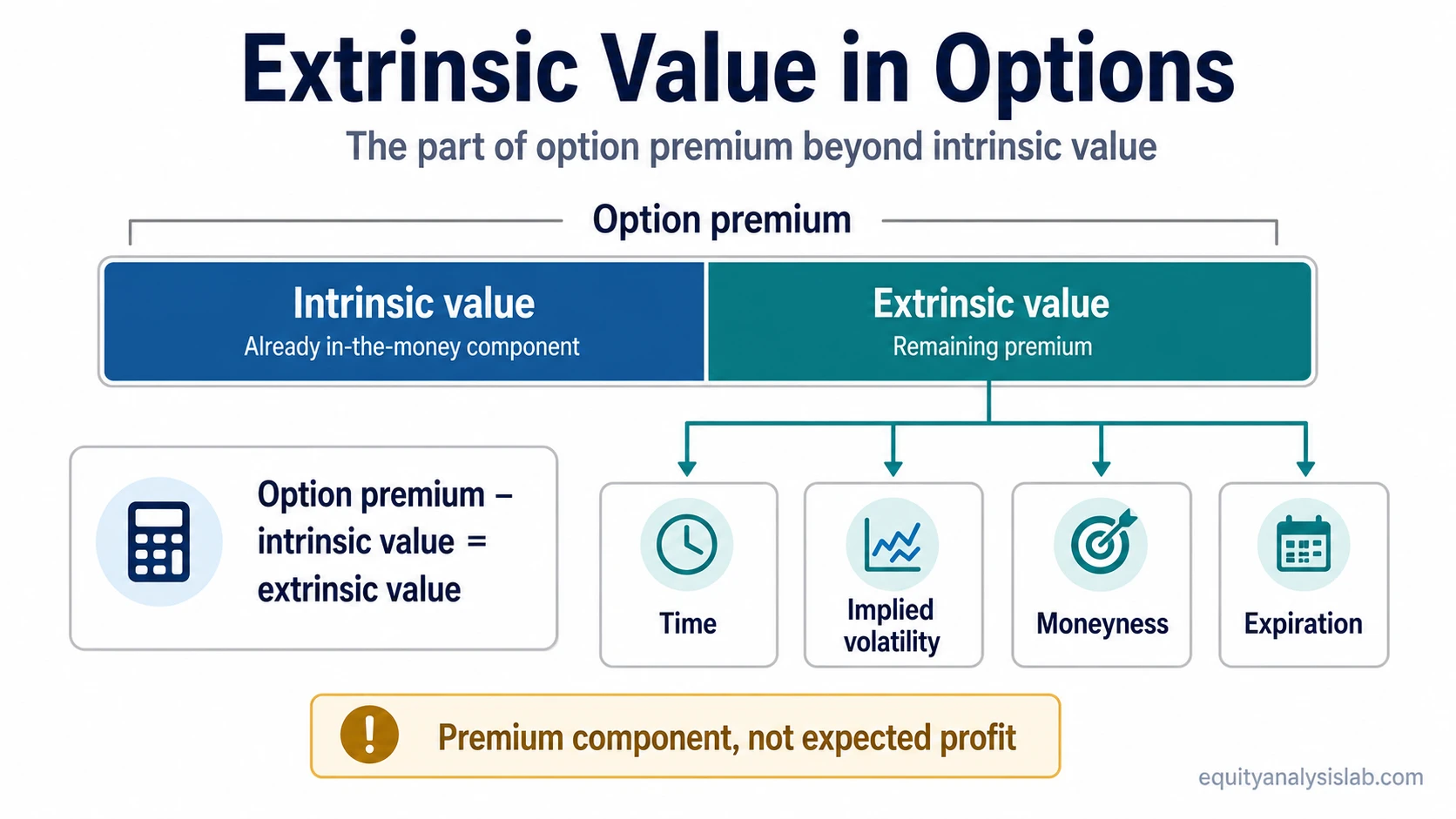

Extrinsic value in options is the part of an option premium that remains after intrinsic value is removed. It reflects what the market is pricing for time, uncertainty, implied volatility, moneyness, and the remaining path before expiration.

Definition: Extrinsic value = option premium − intrinsic value. If an option has no intrinsic value, its entire premium is extrinsic value.

Extrinsic value is sometimes described as time value, but that shorthand can be incomplete. Time matters, but the premium can also change when implied volatility rises or falls, when the option moves closer to or farther from the strike, and when expiration approaches.

A cleaner way to read extrinsic value is as the market-priced portion of premium that is not already explained by immediate exercise value. It is not expected profit, not certainty, and not an instruction to exercise, hold, sell, close, or write an option.

Key Points

- Extrinsic value is the option premium above intrinsic value.

- The basic formula is option premium minus intrinsic value.

- Time, implied volatility, moneyness, and expiration can all affect the extrinsic portion of premium.

- Extrinsic value usually declines as expiration approaches, but volatility changes can alter the path before expiration.

- Low or high extrinsic value does not automatically make an option attractive, risky, or suitable.

What Extrinsic Value Means

Option premium has two main components: intrinsic value and extrinsic value. Intrinsic value measures the amount by which an option is already in the money. Extrinsic value is everything else in the premium.

That “everything else” is not random. It reflects the market’s pricing of remaining uncertainty. More time before expiration can leave more room for the underlying price to move. Higher implied volatility can increase the premium because larger expected movement is being priced. Moneyness also matters because at-the-money options often carry meaningful extrinsic value when small price changes can affect whether the option finishes in or out of the money.

What it is: the non-intrinsic portion of option premium.

What it is not: guaranteed profit, expected return, a complete valuation of the option, or a decision rule by itself.

How to Calculate Extrinsic Value

The calculation is simple once the option premium and intrinsic value are known.

Formula: Extrinsic value = option premium − intrinsic value.

For a call option, intrinsic value depends on how far the underlying price is above the strike price. For a put option, intrinsic value depends on how far the underlying price is below the strike price. If the option is out of the money, intrinsic value is zero, so the premium is entirely extrinsic.

Simple extrinsic value example: A stock is at $52. A call has a $50 strike price and trades for $3.20. The call has $2.00 of intrinsic value because the stock is $2 above the strike. The remaining $1.20 is extrinsic value.

The $1.20 is a premium decomposition, not a position evaluation. It reflects remaining time, uncertainty, volatility expectations, and the possibility that the option’s value may change before expiration.

What Affects Extrinsic Value

Extrinsic value changes because option premium is sensitive to more than the current gap between the underlying price and the strike. The most important drivers are time, implied volatility, moneyness, and the approach of expiration.

Extrinsic value can also change even if the underlying price barely moves, because implied volatility and remaining time can change independently of the current stock price.

| Driver | What it affects | How to read it safely |

|---|---|---|

| Time to expiration | How much uncertainty remains before the contract expires | More time can support more extrinsic value, but it does not guarantee a favorable result. |

| Implied volatility | The market-priced expectation of future movement | Higher implied volatility can raise extrinsic value, but it can also fall and reduce premium. |

| Moneyness | The relationship between the strike price and the underlying price | At-the-money options often carry meaningful extrinsic value because small price changes can affect final status. |

| Expiration | The time boundary of the contract | Extrinsic value approaches zero at expiration because no future time remains in the contract. |

| Rates and dividends | Secondary pricing inputs in some option models | They can matter in pricing, but the first reading usually starts with time, implied volatility, moneyness, and expiration. |

Theta and vega are common labels for sensitivity to time decay and implied volatility. Those labels help describe the mechanics, but they are not needed to understand the core definition of extrinsic value.

Extrinsic Value vs Intrinsic Value

The boundary is straightforward: intrinsic value is the portion of premium already explained by the option’s in-the-money amount, while extrinsic value is the remaining premium beyond that amount.

Intrinsic value in options answers a different question: how much value exists from the current relationship between the underlying price and the strike. Extrinsic value answers what the market is pricing beyond that immediate exercise value.

| Component | Core question | Main inputs |

|---|---|---|

| Intrinsic value | How much value exists if the option is already in the money? | Underlying price, strike price, option type |

| Extrinsic value | How much premium remains beyond intrinsic value? | Time, implied volatility, moneyness, expiration |

A high extrinsic value reading can reflect more uncertainty priced into the contract. A low extrinsic value reading can reflect less remaining time, lower implied volatility, deeper in-the-money status, or a combination of factors.

Extrinsic Value Near Expiration

Extrinsic value tends to shrink as expiration gets closer because the option has less time left for the underlying price to move. At expiration, extrinsic value is zero. Any remaining option value is intrinsic value, if the option finishes in the money.

The path into expiration is not always smooth. A change in implied volatility can offset or accelerate the decline in extrinsic value before the final expiration boundary. That is why time decay should be read with volatility conditions, not as a mechanical straight-line process.

Limitation: Time decay describes pressure on the extrinsic portion of premium. It does not say whether an option position is favorable, whether the premium is “cheap” or “expensive,” or whether a specific action is appropriate.

Exercise and Assignment Nuance

Extrinsic value can matter when comparing exercise value with market premium, because exercising an option can give up remaining extrinsic value. The same boundary also helps explain why assignment discussions should not be reduced to intrinsic value alone.

Low extrinsic value may change the incentives around exercise, especially near expiration or around special contract conditions, but it does not create an automatic rule. Assignment depends on contract terms, holder behavior, broker processes, and the option’s status near expiration.

Broader contract mechanics, rights, obligations, strike price, expiration, and premium fit together inside how options work. Extrinsic value is one pricing component inside that larger contract structure.

Common Mistakes With Extrinsic Value

| Mistake | Safer interpretation |

|---|---|

| Confusing extrinsic value with profit | Extrinsic value is part of premium, not a guaranteed return. |

| Reading low extrinsic value as an automatic instruction | Low extrinsic value does not by itself decide whether to exercise, hold, sell, close, roll, or write an option. |

| Treating time value as the whole explanation | Time is important, but implied volatility and moneyness can also change extrinsic value. |

| Ignoring expiration | Extrinsic value can remain meaningful before expiration, but it disappears at expiration. |

The cleanest reading is component-based: extrinsic value explains the premium beyond intrinsic value, while contract terms, expiration, and position context remain separate questions.

FAQ

Is extrinsic value the same as time value?

Extrinsic value is often called time value, but that shorthand is incomplete. Time matters, but implied volatility, moneyness, and expiration conditions can also affect the extrinsic portion of premium.

Does extrinsic value go to zero at expiration?

Yes. At expiration, no future time remains in the contract, so extrinsic value is zero. Any remaining value is intrinsic value if the option finishes in the money.

Can an out-of-the-money option have extrinsic value?

Yes. An out-of-the-money option has no intrinsic value, so its premium is entirely extrinsic value before expiration.

Does low extrinsic value mean an option should be exercised?

No. Low extrinsic value can affect exercise incentives, but it is not an automatic instruction. Contract terms, expiration, option status, and the holder’s situation all matter.