A stock buying process is the sequence an investor uses to decide whether a stock is ready for capital before placing an order.

It is not the same as clicking a buy button, choosing an order type, or reacting to a price move. A useful process separates the investment thesis, valuation context, portfolio fit, risk boundary, and order placement so the decision is made before execution mechanics take over.

Key Points

- A stock buying process starts with investment readiness, not brokerage mechanics.

- The first unresolved layer usually determines the next action: thesis, valuation, portfolio fit, risk boundary, or execution.

- Order placement belongs near the end of the process, after the investor has defined why the stock belongs in the portfolio.

- The process does not turn a stock into a recommendation, a price target, or a guaranteed outcome.

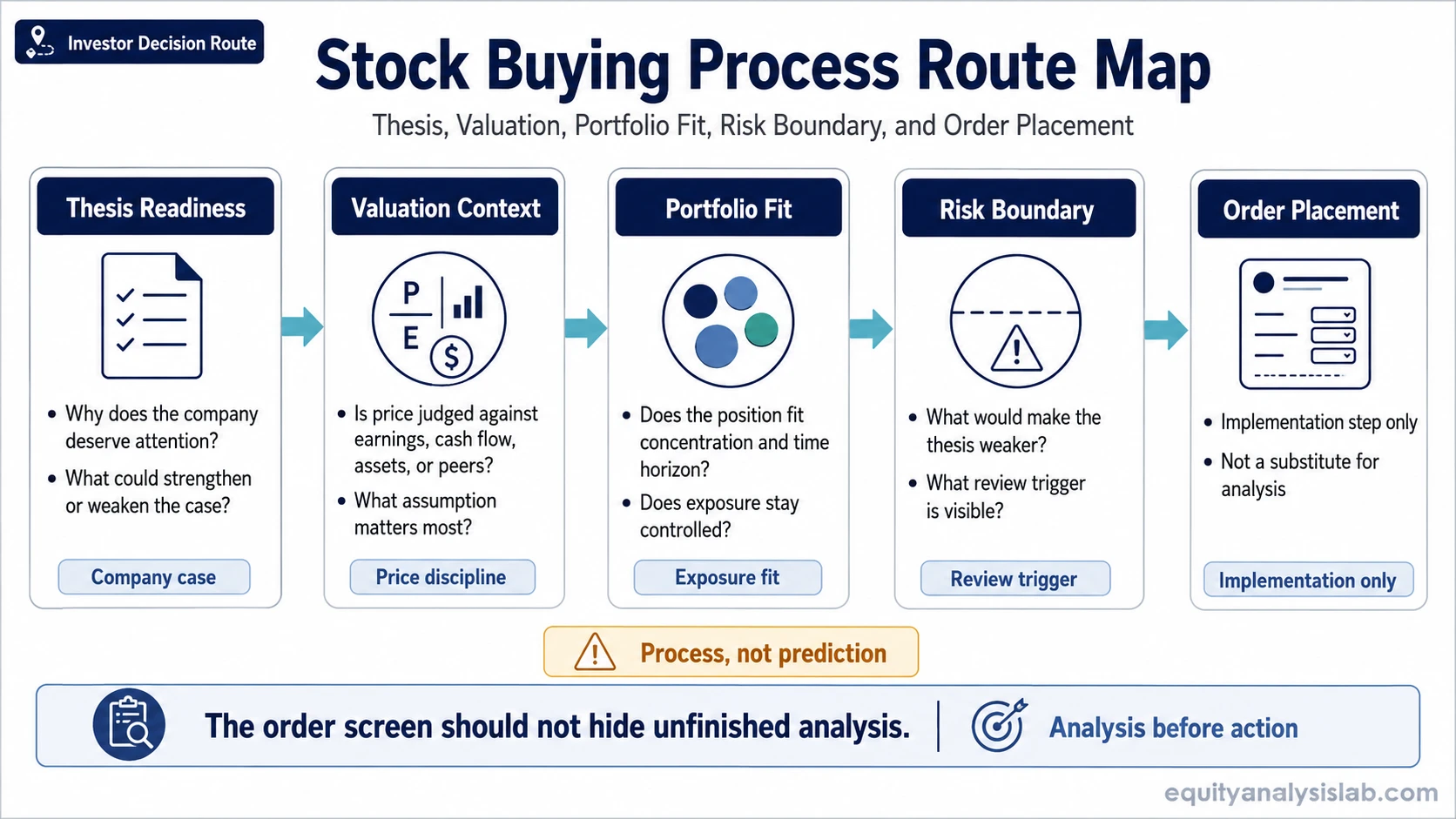

What Is the Stock Buying Process?

The stock buying process is an investor decision route for moving from interest in a company to a controlled purchase decision. It asks whether the business case is understandable, whether valuation gives enough context, whether the position fits the portfolio, and whether the risk boundary is clear enough before an order is placed.

This keeps the decision from becoming a reaction to one headline, one chart move, one valuation ratio, or one attractive story. A stock can look interesting and still fail the process if the thesis is unclear, valuation is stretched, portfolio exposure is already high, or the downside boundary is not defined.

Stock Buying Process vs Order Placement

Order placement is the mechanical step of submitting an instruction through a brokerage platform. The buying process is the analytical sequence that should happen before that instruction exists.

| Area | Decision-process question | Execution-mechanics question |

|---|---|---|

| Company view | What business, earnings, cash flow, or asset-quality reason supports interest in the stock? | None. This is not solved by the order screen. |

| Valuation | What price discipline or valuation context makes the idea worth considering? | None. The order ticket only submits the chosen price or order instruction. |

| Portfolio fit | How would the position affect concentration, diversification, and time horizon? | None. The platform does not decide whether the exposure is appropriate. |

| Risk boundary | What would make the thesis weaker or no longer worth owning? | Execution may express the decision, but it does not create the reasoning. |

| Order placement | Has the investment decision already been made clearly enough? | What order instruction is being used to implement the decision? |

Which Decision Comes First?

The first decision is not usually “how do I buy this stock?” It is “why would this stock deserve capital at all?” That question forces the process to start with the investment case instead of the transaction.

A clean route usually moves through five layers: thesis readiness, valuation context, portfolio fit, risk boundary, and execution mechanics. If any earlier layer is unresolved, the later layer should not be treated as the solution.

| Decision question | What must be resolved | Next route |

|---|---|---|

| Do I understand the company case? | The decision needs a clear view of what drives the business, what could improve or weaken results, and why the stock is being considered. | Stay in company analysis until the thesis is clear enough to test. |

| Does valuation give enough context? | The decision needs valuation context across earnings, cash flow, assets, growth durability, or another relevant input. | Move to valuation work before treating interest as a purchase decision. |

| Does the stock fit the portfolio? | The decision needs a portfolio-fit check across concentration, diversification, time horizon, and changes to the portfolio’s risk profile. | Adjust sizing logic or decline the idea if the exposure is not justified. |

| Is the risk boundary clear? | The decision needs a defined review trigger for thesis weakness, evidence changes, and loss of confidence. | Define the boundary before order placement. |

| Is this a new position or an addition? | A first purchase asks whether the stock deserves initial capital. An add decision asks whether the existing thesis still supports more exposure. | Use a separate route for when to add to a stock position. |

| Is the order only an implementation step? | The rationale, size logic, risk boundary, and purchase constraint should already be clear. | Only then should execution mechanics enter the process. |

What to Resolve Before Buying

The process becomes more useful when each layer has a clear job. The goal is not to remove uncertainty. The goal is to make the unresolved uncertainty visible before capital is committed.

Thesis readiness: The investor should be able to state why the company is being considered and what evidence would make the case stronger or weaker.

Valuation context: The investor should understand whether the price makes sense against earnings, cash flow, assets, growth, or peer context.

Portfolio fit: The investor should know whether the position improves the portfolio or adds unwanted concentration, style exposure, or time-horizon mismatch.

Risk boundary: The investor should define what would trigger review, reduction, or rejection of the idea.

Order placement: The investor should treat the order as implementation, not as the decision itself.

What Does Not Belong in This Process

A stock buying process should not become a list of reasons to justify a purchase after the decision has already been made. It should also avoid treating every attractive story, recent decline, or popular catalyst as a complete investment case.

A low price, a popular catalyst, a valuation discount, or a recent pullback does not automatically make a stock ready to buy. Those inputs may belong inside the analysis, but they do not replace the full route.

Common mistake: treating “I like the company” as the same thing as “the stock deserves capital now.” The first statement is interest. The second requires valuation context, portfolio fit, and risk definition.

Priority Path Notes

When the process is unclear, the next step should follow the weakest unresolved layer. If the business case is vague, the next step is analysis. If the business case is clear but price discipline is missing, the next step is valuation. If valuation looks reasonable but portfolio exposure is already heavy, the next step is portfolio review. If the investor cannot name what would weaken the thesis, the next step is risk-boundary work.

This route prevents the order screen from hiding unfinished analysis. A purchase may still involve uncertainty, but the uncertainty should be visible before capital is committed.

Short Route Example

An investor finds a profitable company with a business model they understand. The first route is not order placement. The investor first checks whether the thesis depends on durable earnings, temporary margin improvement, one-time news, or a changing balance-sheet condition.

If the thesis survives that check, the investor then asks whether valuation is reasonable for the quality and risk of the business. If valuation still makes sense, the next question is whether the position would create too much concentration. Only after those layers are clear does the order become an implementation detail.

After Buying, the Process Changes

After a first purchase, the decision route changes from “should this stock receive initial capital?” to “does the thesis still justify holding, reducing, or adding exposure?” That second question should not be mixed into the first-buy process too early.

Adding to a position usually needs a stricter review because the investor is increasing exposure to a risk already present in the portfolio. That is why a first-buy decision and an add-position decision should be separated.

Limitations of a Stock Buying Process

A stock buying process is a decision framework, not a guarantee. It can improve discipline by separating thesis, valuation, portfolio fit, risk boundary, and order placement, but it cannot remove uncertainty or prove that a stock will perform well.

The process should also avoid false precision. A model can be wrong, a thesis can deteriorate, a portfolio can become too concentrated, and an order can still be poorly timed. The value of the process is that these issues are surfaced before the investor acts, not that they disappear.

FAQ

Is the stock buying process the same as learning how to buy stocks?

No. Learning how to buy stocks usually focuses on accounts, platforms, and order placement. The stock buying process focuses on the investor decision sequence before an order is placed.

What is the first step in a stock buying process?

The first step is clarifying why the stock deserves consideration. That usually means understanding the company case before moving into valuation, portfolio fit, risk boundaries, and execution mechanics.

Does a stock buying process recommend a stock?

No. It organizes the decision, but it does not create a recommendation, target price, return forecast, or buy signal.

Where does order placement fit?

Order placement comes after the investment decision is clear enough to implement. It should not replace thesis work, valuation context, portfolio review, or risk definition.