The investment research process turns an initial stock or security idea into organized evidence before an investor decides whether the idea deserves deeper due diligence, watchlist tracking, portfolio review, rejection, or no action.

It is not a buy or sell signal. The process gives structure to judgment by separating the story behind an idea from the evidence that can support, weaken, or change that idea.

Key Points

- The investment research process organizes evidence before an investment decision is considered.

- It usually includes idea intake, screening, business review, financial evidence, valuation context, risk review, portfolio fit, and monitoring.

- A strong process records what is known, what remains uncertain, and what would change the interpretation.

- Watchlists, templates, and due diligence checklists can support the process, but none of them replaces investor judgment.

What Is the Investment Research Process?

The investment research process is the structured sequence investors use to examine a potential investment before action. It connects the original idea to business evidence, financial statements, valuation context, risk factors, and portfolio fit.

The process matters because an attractive narrative can be incomplete. Revenue growth, product momentum, or a popular market theme may create a reason to investigate, but research has to test whether the story is supported by cash flow, earnings quality, balance-sheet strength, competitive position, valuation, and forward risk.

For a fundamental investor, the process is best understood as an evidence filter. It does not tell an investor what to own. It helps an investor decide whether the evidence is strong enough to keep studying the idea, place it on a research watchlist, compare it with alternatives, or discard it.

Why the Process Comes Before the Investment Decision

A stock idea often begins with a single observation. The company may appear cheap, earnings may be improving, the balance sheet may look safer than expected, or the business may be gaining market share. Those observations are not yet a complete investment case.

The research process forces the idea to move through separate checks. Business quality is examined separately from valuation. Financial evidence is examined separately from the market narrative. Risk is examined separately from upside potential. Portfolio fit is examined separately from whether the company looks interesting on its own.

This separation reduces a common mistake: treating the first attractive fact as if it resolves the full decision. A company can have strong current fundamentals and still face forward risk. A valuation can look reasonable and still depend on assumptions that are difficult to defend. A watchlist candidate can be worth monitoring without being ready for portfolio action.

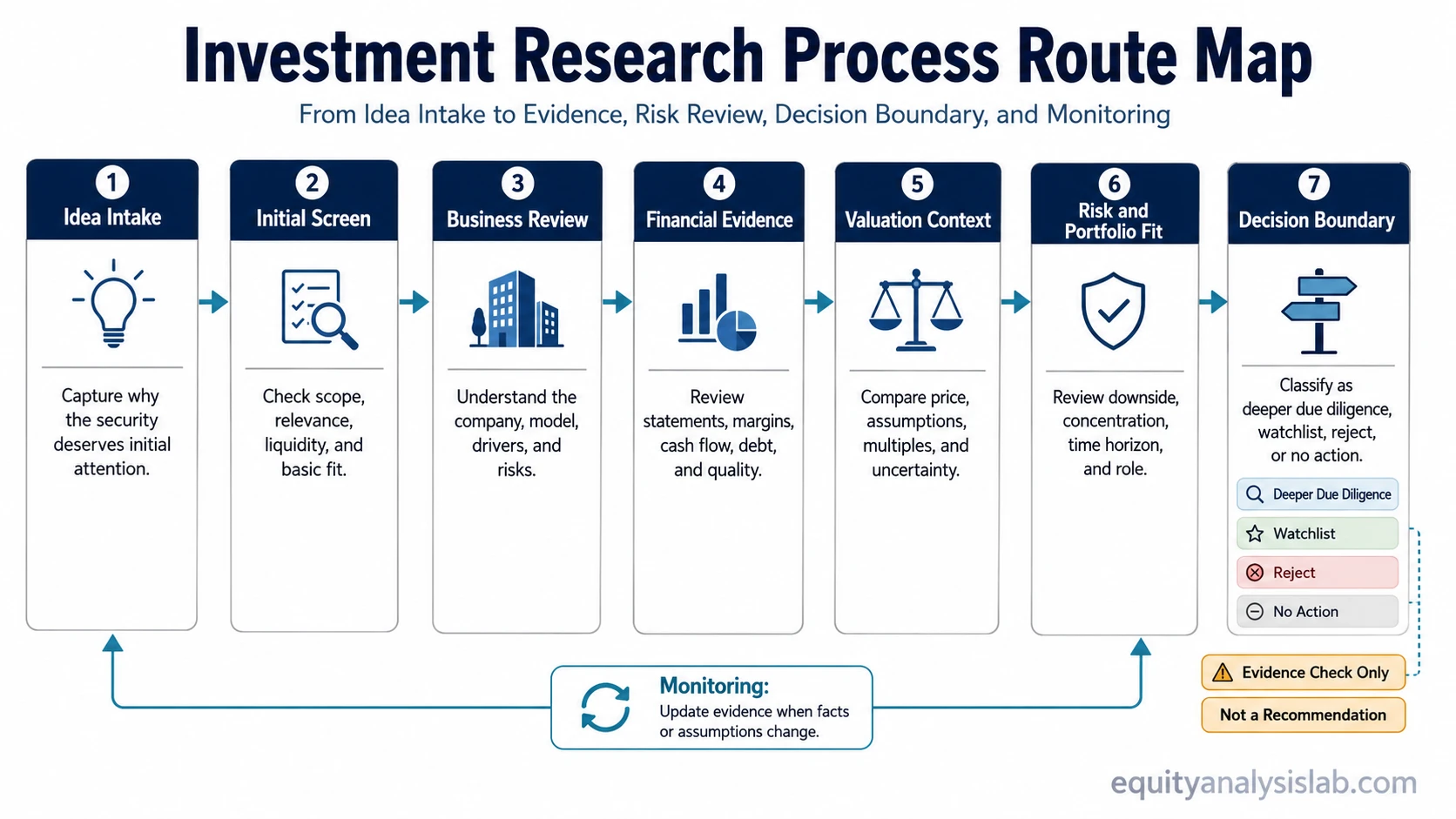

The Core Stages of an Investment Research Process

A practical investment research process usually moves from idea capture to evidence review, then toward decision boundaries. The exact format can vary by investor, but the core logic is consistent: each stage should answer a different question.

| Stage | Question Answered | Evidence Used | Decision Boundary |

|---|---|---|---|

| Idea intake | Why is this security worth initial attention? | Business change, valuation screen, earnings change, industry trend, or investor observation | The idea is only a candidate, not a conclusion. |

| Initial screening | Is there enough relevance to continue? | Market capitalization, liquidity, sector, basic financial metrics, business description, and availability of reliable information | Weak or off-scope ideas can be rejected early. |

| Business review | What does the company do, and what drives the economics? | Revenue model, customer base, competitive position, industry structure, pricing power, and operating risks | A clear business model is needed before valuation has much meaning. |

| Financial evidence | Does the financial record support the story? | Revenue, margins, cash flow, debt, working capital, share count, and earnings quality | Numbers should either support, challenge, or narrow the thesis. |

| Valuation context | What expectations appear to be embedded in the price? | Multiples, DCF assumptions, peer context, historical ranges, and scenario sensitivity | Valuation is context, not proof of exact value. |

| Risk and portfolio fit | What could go wrong, and does the idea fit the portfolio? | Downside drivers, concentration, time horizon, liquidity needs, position role, and alternative uses of capital | A good company can still be a poor portfolio fit. |

| Decision boundary | What is the next research classification? | Evidence strength, uncertainty, valuation range, risk review, and portfolio constraints | The idea can move to due diligence, watchlist, rejection, or no action. |

| Monitoring | What evidence would change the view? | Earnings releases, guidance, filings, competitive changes, valuation changes, and thesis milestones | The research view should update when facts or assumptions change. |

For macro-sensitive ideas, the research process should also separate company evidence from the global liquidity cycle, because financing conditions can change the market backdrop without proving or disproving the company thesis by themselves.

Investment Research Process vs Due Diligence

The investment research process and due diligence are related, but they are not identical. Research is the broader workflow that moves an idea from discovery to evidence organization. Due diligence is the deeper verification stage that tests the most important assumptions before a final investment decision.

| Concept | Main Role | Typical Timing | Output |

|---|---|---|---|

| Investment research process | Organizes the full path from idea to evidence and decision boundary | Begins before deep verification | Research notes, thesis questions, watchlist status, or rejection |

| Due diligence | Tests the strongest and weakest parts of a potential thesis | Comes after an idea appears relevant enough to justify deeper work | Higher-confidence evidence, unresolved risks, and decision-ready assumptions |

A due diligence checklist can help prevent skipped questions, but it should not replace the broader process. The checklist is a tool. The research process is the framework that decides when the checklist is needed, what evidence matters most, and whether the answer changes the decision boundary.

How Investment Research Connects to Valuation

Valuation is one part of the investment research process, not the whole process. A valuation model can estimate a range of possible outcomes, but the usefulness of that range depends on the quality of the business evidence behind the assumptions.

For example, a discounted cash flow model may depend heavily on margin assumptions, reinvestment needs, revenue durability, and terminal value. If the business review is weak, the valuation may look precise while resting on fragile inputs. A comparable-company analysis can provide market context, but it can also hide important differences in growth quality, leverage, margins, accounting, and cyclicality.

Research should therefore connect valuation back to evidence. If the valuation case depends on margin expansion, the process should ask what supports that margin improvement. If the thesis depends on cash generation, the process should review free cash flow rather than relying only on headline earnings. If the company appears cheap on a multiple, the process should ask whether the multiple reflects temporary fear, structural decline, or a risk that the initial screen missed.

How to Document the Research Process

Documentation turns research from a loose opinion into a reviewable record. It does not need to be complicated, but it should be clear enough that the investor can revisit the original reasoning later.

A useful research note should record:

- the original reason the idea entered the process;

- the business model and main economic drivers;

- the most important financial evidence;

- the valuation context and key assumptions;

- the main risks and what would change the view;

- the portfolio role, if the idea ever becomes eligible for action;

- the current classification: reject, monitor, research further, or decision-ready.

The purpose of the note is not to create a perfect document. It is to preserve the logic. Without documentation, it becomes easy to forget why an idea was attractive, which assumptions were uncertain, and which facts were supposed to be monitored.

Common Mistakes in the Investment Research Process

Most research mistakes come from collapsing separate stages into one conclusion. A process helps only if each stage is allowed to challenge the previous one.

| Mistake | Why It Weakens the Process | Cleaner Research Behavior |

|---|---|---|

| Starting with a conclusion | The investor looks only for confirming evidence. | Write the initial thesis as a hypothesis, then record what could disprove it. |

| Treating valuation as proof | A model can look precise even when its assumptions are fragile. | Connect each major valuation input to business and financial evidence. |

| Ignoring portfolio fit | A strong standalone idea can still increase concentration or liquidity risk. | Review position role, time horizon, and portfolio exposure before action. |

| Confusing a watchlist with research | A list of names does not explain evidence quality or decision criteria. | Use the watchlist as a tracking tool, not as the research process itself. |

| Failing to update assumptions | The original thesis may remain in place after the facts have changed. | Define the evidence that should trigger review, downgrade, or removal. |

Where Watchlists and Templates Fit

Watchlists and templates are useful, but they are not substitutes for research. A watchlist helps organize securities that may deserve future review. A research template helps make evidence easier to compare across companies. A checklist helps reduce the chance of skipping obvious risks.

The distinction matters because tools can create a false sense of completeness. A spreadsheet full of tickers does not show whether the investor understands the business. A filled-out template does not prove that the assumptions are defensible. A checklist does not decide whether the risk is acceptable.

The research process gives those tools a role. A stock watchlist can hold ideas that are not decision-ready. A template can preserve notes. A checklist can support due diligence. The final judgment still depends on evidence quality, valuation context, risk, and portfolio fit.

A Practical Research Process Example

Consider a company that appears on a screen because its valuation multiple has fallen below its historical range. That fact alone does not create an investment case. The first research question is why the multiple fell.

The process might begin by checking whether revenue growth has slowed, margins are under pressure, debt has increased, or the market is discounting a permanent business change. If the financial statements show stable cash generation and the business review suggests the problem may be temporary, the idea may deserve deeper due diligence. If the same review shows weakening demand, rising leverage, and poor cash conversion, the low multiple may reflect real risk rather than opportunity.

The decision boundary is not “buy” or “do not buy” at the first screen. A cleaner classification might be: reject because the business risk is structural, monitor because the evidence is mixed, or continue research because the initial concern is explainable and the valuation context remains relevant.

What Makes the Process Useful?

The investment research process becomes useful when it prevents premature certainty. It should make the investor slower to accept a narrative, faster to identify missing evidence, and more disciplined about separating interest from action.

Process limitation: A structured process cannot remove uncertainty. It can only make uncertainty more visible. Even careful research can miss future events, management decisions, accounting issues, competitive shifts, and valuation changes.

That limitation is why monitoring belongs inside the process. Research should not end after the first decision boundary. If the company reports new results, changes guidance, issues shares, loses a major customer, takes on more debt, or trades into a different valuation range, the original notes should be reviewed against the new evidence.

Bottom Line

The investment research process is a structured way to move from an initial idea to organized evidence. It separates business understanding, financial review, valuation context, risk assessment, portfolio fit, and monitoring so that an investor does not confuse interest with a completed investment case.

The process becomes more useful when each tool has a clear job. A watchlist helps track ideas after they pass an initial relevance screen. A template helps store notes. A due diligence checklist helps prevent skipped questions. The investment decision remains separate because it has to combine evidence quality, valuation context, risk, and portfolio constraints.

The strongest workflow keeps those roles distinct. Research organizes the evidence. Monitoring updates the evidence. Portfolio review decides whether the idea fits the investor’s constraints.

FAQ

What is the investment research process?

The investment research process is the sequence investors use to turn an initial security idea into organized evidence. It usually includes idea intake, screening, business analysis, financial review, valuation context, risk review, portfolio-fit checks, and a decision boundary.

What are the main stages of investment research?

The main stages are idea intake, initial screening, business review, financial evidence review, valuation context, risk and portfolio-fit review, decision boundary, and monitoring. The exact format can vary, but each stage should answer a different question.

Is investment research the same as a watchlist?

No. Investment research is the evidence process. A watchlist is a tracking tool for securities that may deserve monitoring or later review. A watchlist can support research, but it does not replace the process.

Does the investment research process tell investors what to buy?

No. The process supports judgment by organizing evidence, risks, assumptions, and portfolio-fit considerations. It does not create a buy or sell signal by itself.