ETF selection is the process of narrowing funds by the role they should play, the exposure they actually hold, and the fund mechanics that can change investor outcomes. A useful ETF selection process starts with portfolio role, then checks exposure, index or strategy, holdings, cost, tracking, liquidity, currency, distribution, domicile, and tax mechanics before comparing specific funds.

An ETF is the wrapper, not the full decision. The selection question is whether that wrapper gives the investor the intended exposure in a structure that fits the portfolio, trading conditions, income treatment, and tax context.

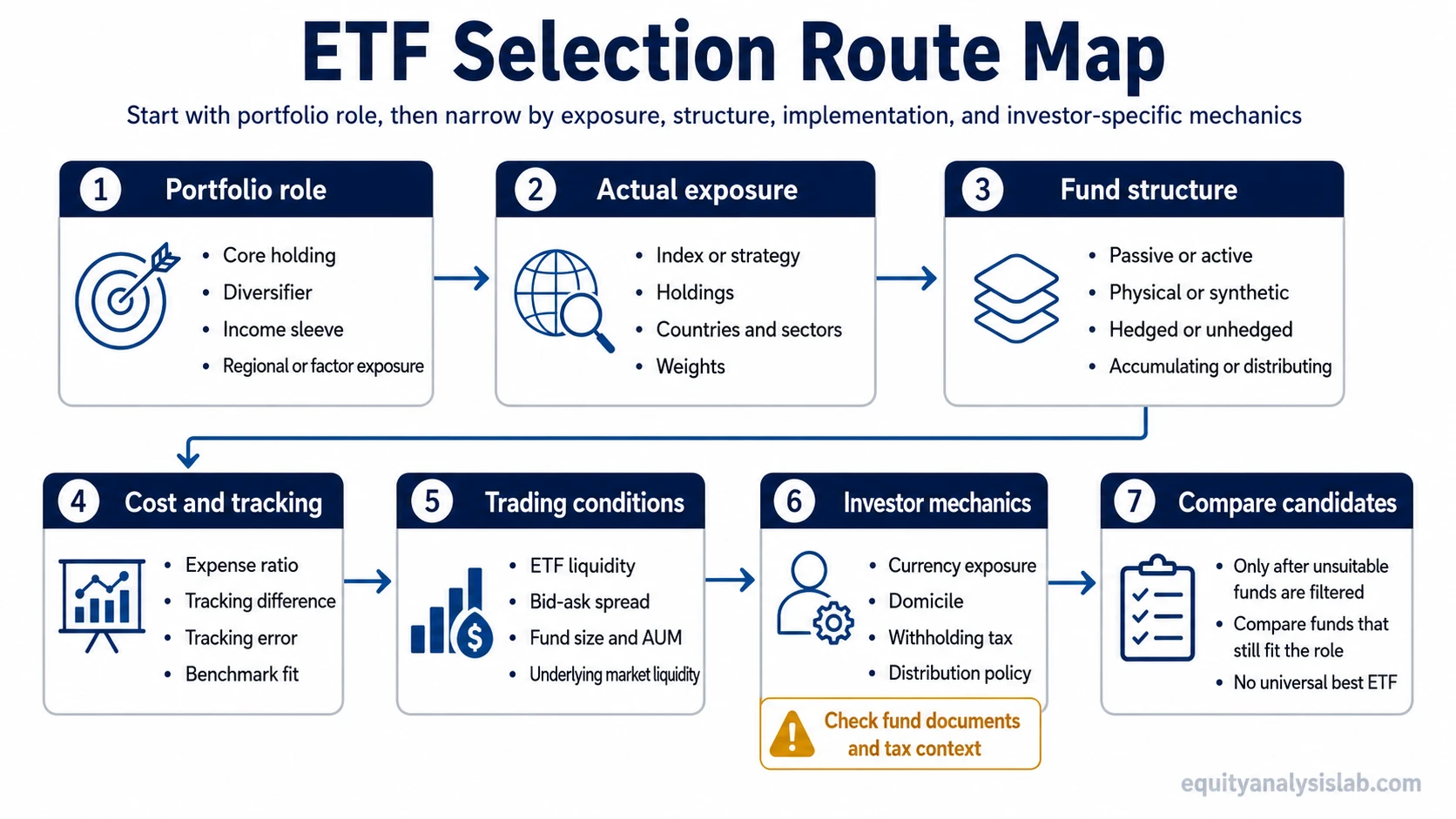

ETF selection is not a search for one universal best ETF. The stronger process is to identify which criteria can change the decision, remove unsuitable funds early, and compare only the candidates that still fit the intended job.

ETF selection criteria that change the decision

- Portfolio role comes first: a fund used as a core holding is judged differently from a satellite exposure, income sleeve, regional allocation, or narrow tactical position.

- Exposure needs document-level confirmation: similar fund names can hide different regions, sectors, weights, securities, replication methods, and currency exposures.

- Cost belongs with implementation quality: the stated fee is useful, but it should be read alongside benchmark fit, trading conditions, spread, and tax mechanics.

- Liquidity affects the realized trade: exchange volume, underlying-market liquidity, and spread conditions can matter when entering, exiting, or rebalancing.

- Tax and income mechanics can change the investor result: domicile, withholding tax, distribution policy, and investor residence can make similar funds behave differently after tax.

- Comparison works best after filtering: side-by-side comparison is more useful after the investor has already narrowed role, exposure, structure, and practical constraints.

ETF selection route map

Each ETF selection criterion changes a different part of the decision. The useful next check depends on the remaining uncertainty: portfolio fit, exposure, structure, cost, tracking, trading conditions, currency, tax, or income treatment.

| Selection criterion | Decision impact | Deeper check |

|---|---|---|

| Portfolio role | Sets the job of the fund: core allocation, satellite exposure, income sleeve, risk reduction, or a narrower portfolio position. | |

| Exposure and holdings | Clarifies what the investor actually owns: countries, sectors, issuers, weights, securities, derivatives, or other instruments inside the fund. | how to choose an ETF |

| Index or strategy | Separates benchmark tracking, factor methods, active processes, thematic screens, equal-weight rules, and other selection approaches. | how to compare ETFs |

| Cost | Shows the stated ongoing charge, while leaving room for tracking, trading, and tax effects to influence the final result. | expense ratio |

| Tracking quality | Checks whether the fund follows the intended benchmark closely and whether the return gap is persistent, volatile, positive, or negative. | |

| Liquidity and trading conditions | Highlights whether the investor may face avoidable spread cost, thin trading, or weak execution conditions when buying or selling. | |

| Fund size | Adds scale context without treating size as an automatic quality score or a substitute for exposure review. | fund size and AUM |

| Currency mechanics | Separates foreign asset performance from currency movement and hedge overlays that can change the home-currency return path. | |

| Domicile and withholding tax | Connects fund domicile, treaty access, withholding tax, and investor residence to possible after-tax differences. | ETF domicile and withholding tax |

| Distribution policy | Distinguishes distributing and accumulating structures, income treatment, and fit with the investor’s portfolio and tax situation. | ETF dividends |

A practical order for narrowing ETF choices

ETF selection becomes cleaner when broad fit is filtered before individual funds are compared. Starting with cost or recent performance can skip the more important question: whether the fund is the right exposure for the intended job.

- Define the portfolio role. Decide whether the fund is meant to be a core holding, diversifier, income sleeve, regional exposure, factor tilt, sector exposure, or temporary allocation.

- Check the actual exposure. Read the index, strategy, and holdings rather than relying on the fund name alone.

- Confirm the structure. Review whether the fund is passive or active, physical or synthetic where relevant, distributing or accumulating, hedged or unhedged, and domiciled in a structure that fits the investor’s situation.

- Review cost and tracking together. A low stated fee is useful, but realized tracking, benchmark fit, and implementation can also affect the investor’s outcome.

- Review liquidity before trading. A fund may look suitable on paper while still having wider spreads, thin trading, or underlying-market timing issues that matter for execution.

- Check currency, tax, and distribution mechanics. These details can make similar funds behave differently for different investors.

- Compare the remaining candidates. Side-by-side comparison works best after unsuitable exposures and structures have already been removed.

Document checks for ETF selection

Fund documents matter most for fund-specific facts. Holdings, index methodology, fees, distribution policy, domicile, securities lending, replication method, tax treatment, and share-class details should be checked in the fund documents, KID or KIID where applicable, prospectus, issuer materials, exchange data, and relevant tax guidance. Generic ETF criteria can frame the review, but they do not replace fund-specific documents or personal tax context.

What ETF selection should not rely on alone

Expense ratio is only one input. A lower stated cost can help long-term compounding, but it does not settle the decision by itself. Tracking, spreads, securities lending, tax mechanics, and benchmark construction can also affect outcomes.

Past performance needs explanation. A fund can outperform over one period because of index composition, currency movement, factor exposure, timing, or market regime. The reason for the result matters more than the result alone.

Fund name is not full exposure analysis. Similar labels can sit on different securities, indexes, weights, currency exposures, and domicile structures.

Provider brand is context, not proof of fit. Issuer quality may be part of operational review, but the fund’s exposure, structure, documents, costs, tracking, liquidity, and tax treatment still need to match the investor’s objective.

Ratings and screeners are starting points. A rating, list, or filter can narrow research, but it cannot know every investor’s role, tax position, currency exposure, trading size, income need, or portfolio constraint.

Example: similar ETF labels, different mechanics

Two broad international equity ETFs can look similar at first glance. One may track developed markets only, while another may include all-world exposure with emerging markets. One share class may distribute income, while another accumulates it. One version may leave currency exposure unhedged, while another may use a hedge overlay. The fund label may look close, but the investor result can differ because exposure, currency path, income treatment, domicile, and tax mechanics are not the same.

Final ETF selection sequence

A clean ETF shortlist usually starts with portfolio role and exposure, then moves through index or strategy, holdings, cost, tracking, liquidity, fund size, currency, domicile, withholding tax, and distribution policy. The final comparison is strongest when only funds that still fit those requirements remain.