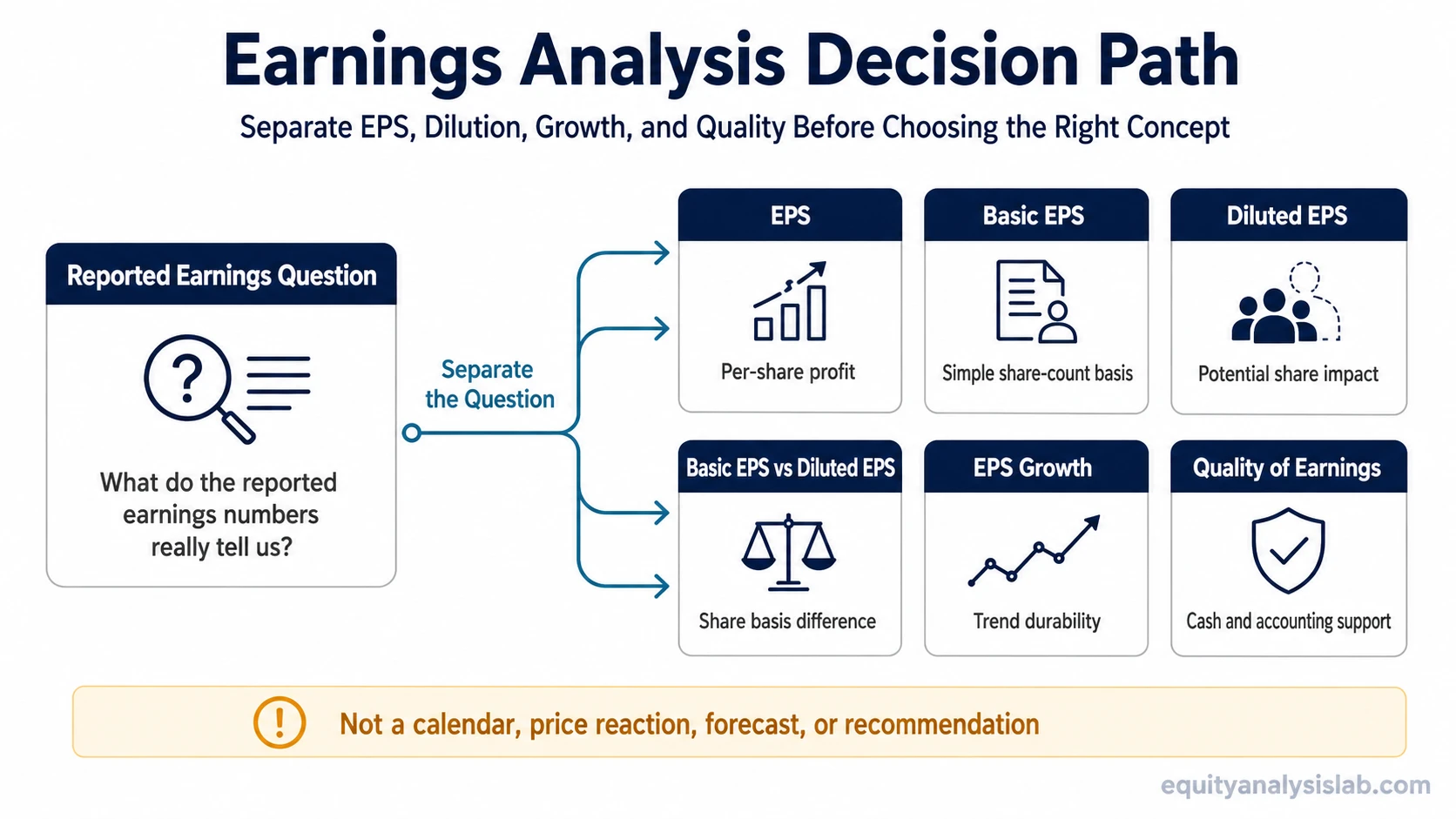

Earnings analysis starts by separating per-share profit, dilution, growth durability, and accounting quality. Each question points to a different concept, so the useful first step is deciding which part of earnings you are trying to understand.

Key Points

- Earnings analysis is most useful when it separates calculation, dilution, growth, and quality instead of treating earnings as one number.

- EPS answers a different question from earnings quality, because one focuses on per-share profit while the other checks the support behind reported profit.

- Growth should be read with cash flow, revenue support, margins, and share-count context instead of treated as a standalone conclusion.

- These concepts are not an earnings calendar, market reaction tool, or investment recommendation framework.

What Earnings Analysis Separates

Earnings can look simple at the headline level, but the underlying question changes the analysis. A per-share number, a dilution adjustment, a growth rate, and a cash-conversion check do not answer the same problem.

A company can show improving reported earnings while the interpretation remains incomplete. The analysis may need to ask whether the improvement came from stronger operations, lower share count, margin expansion, temporary adjustments, or weaker expenses that may not repeat.

The cleanest approach is to separate the evidence before drawing conclusions. EPS shows one lens. Dilution changes the ownership basis. EPS growth introduces time comparison. Earnings quality asks whether the reported number is supported by cash flow and business fundamentals.

Choose the Right Earnings-Analysis Path

Use the path below to match the earnings question with the concept that should be reviewed first.

| Reader question | Read next | Why this path fits |

|---|---|---|

| What does profit per share mean? | earnings per share | Use this when the main question is how net income is expressed on a per-share basis. |

| How is the basic per-share number calculated? | basic EPS | Use this when the question is about the basic share count and the standard per-share calculation. |

| How do options, convertibles, or other potential shares affect EPS? | diluted EPS | Use this when potential share issuance could change the per-share earnings picture. |

| Why are basic EPS and diluted EPS different? | basic EPS vs diluted EPS | Use this when the same earnings period shows two EPS figures and the difference needs to be separated. |

| Is the earnings trend improving over time? | EPS growth | Use this when the question is about comparison across periods, growth durability, and trend interpretation. |

| Are the reported earnings supported by cash flow and accounting quality? | quality of earnings | Use this when the concern is whether reported profit reflects durable operating performance. |

Earnings Concepts to Read First

Start with the concept that matches the narrowest question. If the number itself is unclear, begin with EPS. If the share-count basis is unclear, compare basic and diluted figures. If the reported number looks strong but cash flow is weak, move toward earnings quality.

Per-share profit: Use the EPS path when the question is how profit is translated into a shareholder-level number.

Calculation basis: Use the basic EPS path when the analysis needs the simplest share-count basis before considering potential dilution.

Dilution: Use the diluted EPS path when options, convertibles, warrants, or other potential shares could change the per-share result.

Growth: Use the EPS growth path when the important question is whether earnings are improving, stalling, or becoming less reliable over time.

Quality: Use the quality-of-earnings path when cash conversion, adjustments, accruals, or one-time items may change the meaning of reported earnings.

How to Avoid Mixing Earnings Questions

A common mistake is treating EPS growth as proof that the business itself is improving. EPS growth is stronger when revenue, margins, cash flow, and business quality support it. If EPS improves while revenue weakens or share count changes materially, the analysis should ask what actually drove the per-share improvement.

Another common mistake is treating dilution as a side detail. Dilution can change the shareholder basis of the earnings number, which means two companies with similar net income trends can create different per-share outcomes for investors.

Accounting quality also needs a separate check. Adjusted earnings, one-time items, accruals, and weak cash conversion can all change how much confidence a reader should place in the reported figure.

What Not to Treat as Earnings Analysis

Earnings analysis is not the same as an earnings calendar, earnings-season trading setup, price reaction forecast, or buy/sell decision. A report date can tell when information arrives, but it does not explain the quality, dilution impact, or durability of the earnings themselves.

It is also not a full earnings-report walkthrough. Revenue, margins, cash flow, guidance, and management commentary can all matter, but they are supporting evidence categories. They should be used to clarify the right concept rather than turn the analysis into a broad report-reading tutorial.

Limitations of Earnings Analysis

Limitation: Earnings analysis can organize the evidence, but it does not create a valuation conclusion by itself. EPS, dilution, growth, and quality each answer a narrower question.

Interpretation boundary: Strong reported earnings do not automatically mean the stock is attractive, and weak reported earnings do not automatically mean the business is permanently impaired. The result depends on durability, cash flow support, valuation context, balance-sheet risk, and future expectations.

FAQ

What is earnings analysis?

Earnings analysis is the process of separating reported earnings into the questions that matter most: per-share profit, dilution, growth durability, and earnings quality.

Should earnings analysis start with EPS or earnings quality?

Start with EPS when the per-share number is unclear. Move to earnings quality when the question is whether the reported profit is supported by cash flow, operating performance, and accounting quality.

When does diluted EPS matter more than basic EPS?

Diluted EPS matters when potential shares from options, convertibles, warrants, or similar instruments could reduce the earnings available on a per-share basis.

Why can EPS growth be misleading?

EPS growth can be misleading when it comes mainly from share-count changes, temporary adjustments, or cost effects rather than durable revenue, margin, cash-flow, or business-quality improvement.

Is earnings analysis an investment recommendation?

No. Earnings analysis organizes company evidence. It does not provide a buy, sell, target-price, or return forecast.