Intrinsic value is a model-based estimate of what a business or share may be worth based on expected cash flows, growth, risk, and capital structure assumptions.

Market price is the observable price at which shares trade. Intrinsic value is an analytical estimate, so the gap between the two depends on the quality of the inputs, not just the size of the difference.

Definition: Intrinsic value is an estimate of economic value based on the cash a business may generate over time, adjusted for risk, growth, reinvestment needs, financing structure, and the share count used to convert business value into a per-share figure.

Key Points

- Intrinsic value is an estimate, not a directly observed market fact.

- The estimate changes when cash-flow forecasts, growth assumptions, discount rates, terminal assumptions, or share counts change.

- Market price can differ from intrinsic value because the market reflects current transactions, sentiment, liquidity, and competing expectations.

- A valuation gap does not automatically prove investment merit; the assumptions behind the estimate still need to be tested.

What Intrinsic Value Means in Valuation

Intrinsic value in company valuation starts with the business, not with the stock chart. The analyst estimates what the company can earn or convert into cash, then discounts or compares those future economics using assumptions about risk and time.

The result is usually a range rather than a single perfect number. Cash flow gives the estimate its base, while assumptions give it its range. A small change in growth, margins, reinvestment, discount rate, or share count can move the estimate materially.

The most useful interpretation separates four questions: what the business may be worth, where the stock trades, what assumptions support the estimate, and whether the evidence is strong enough to justify further investor work.

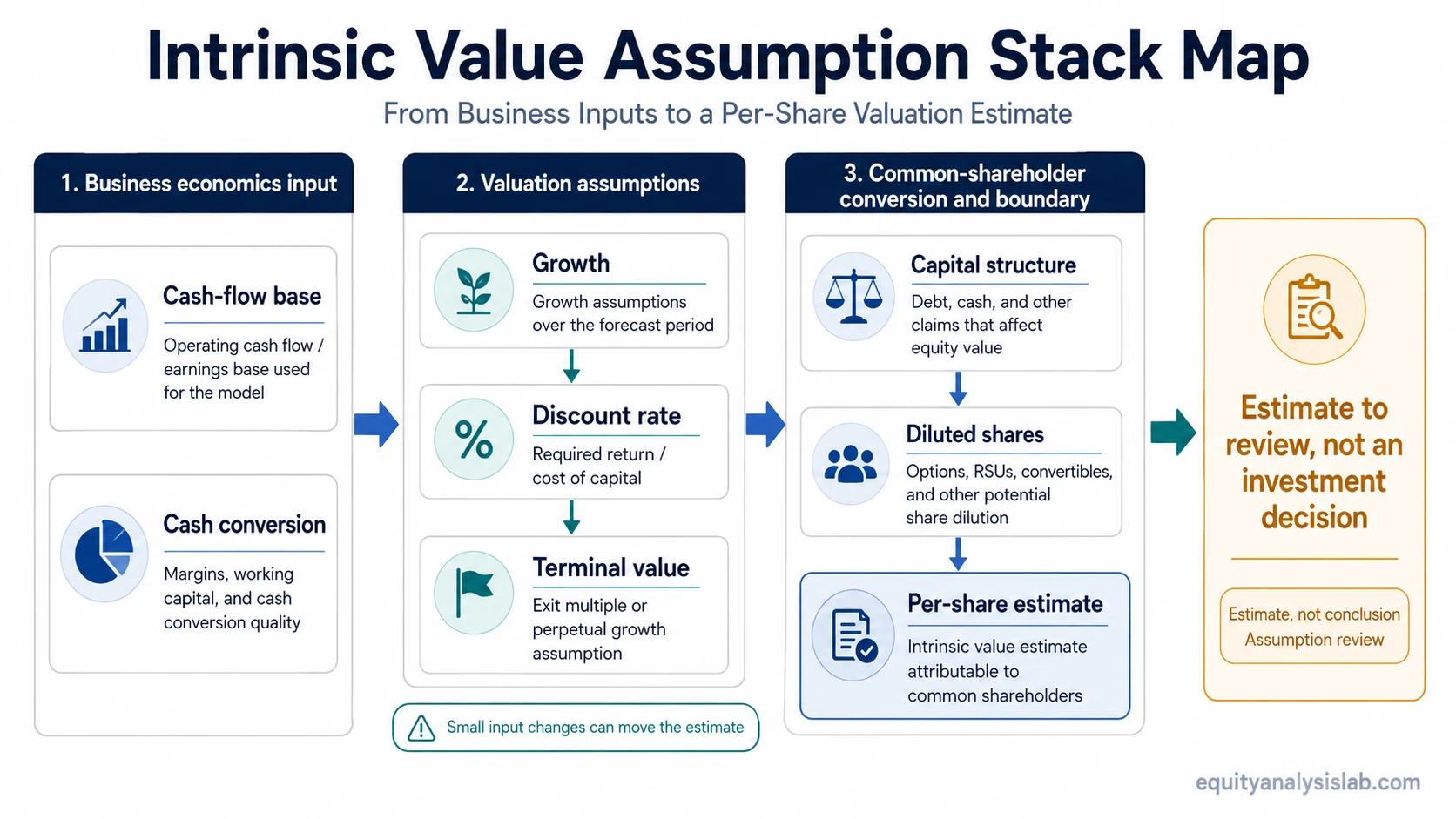

The Assumption Stack Behind Intrinsic Value

Intrinsic value depends on a stack of linked assumptions. A model can look precise while still being fragile if one major input is optimistic, stale, or mismatched to the business.

| Input | What it changes | Why it matters | What can go wrong |

|---|---|---|---|

| Revenue and cash-flow base | The starting economics of the business | Intrinsic value needs a cash-producing base, not only a narrative about future growth. | Revenue growth may not convert into durable free cash flow. |

| Margins and cash conversion | The amount of profit or cash available from each dollar of sales | Higher margins only support value if they are sustainable and visible in cash generation. | Accounting profit can overstate business quality when working capital or capital spending consumes cash. |

| Growth assumptions | The future size of the company’s earnings or cash-flow stream | Growth drives much of the upside in long-duration valuation estimates. | Small growth changes can produce large valuation changes when projected too far into the future. |

| Discount rate | The present value assigned to future cash flows | Higher required return or perceived risk reduces the value of future cash. | A rate that is too low can make uncertain cash flows look more valuable than the evidence supports. |

| Terminal value or exit assumption | The value assigned after the explicit forecast period | Many long-horizon DCF-style models can place a large share of the estimate in the terminal period. | An aggressive terminal assumption can dominate the estimate and hide weak near-term economics. |

| Capital structure and claims | The bridge from business value to shareholder value | Debt, cash, preferred claims, and minority interests can change the value attributable to common shareholders. | Using business value as if it were common equity value can overstate or misclassify the shareholder claim. |

| Diluted share count | The per-share value assigned to common shareholders | Share-based compensation, options, convertibles, and other dilutive securities can spread value across more shares. | A per-share estimate can be overstated if dilution is ignored. |

Why Intrinsic Value Changes When Inputs Change

A valuation estimate is not fixed once it is calculated. The same company can receive a different intrinsic value when the forecast period, discount rate, terminal assumption, margin path, or share count changes.

| Input change | Usual directional effect | Reason the estimate moves |

|---|---|---|

| Higher durable free-cash-flow growth | Raises the estimate, if supported by reinvestment and margins | More future cash is being valued. |

| Higher discount rate | Lowers the estimate | Future cash flows are worth less when required return or risk rises. |

| Lower terminal value assumption | Lowers the estimate | The value assigned beyond the forecast period declines. |

| Weaker cash conversion | Lowers the estimate | Reported earnings are less valuable when they do not turn into cash. |

| Higher diluted share count | Lowers the per-share estimate | The same common-shareholder value is divided across more shares. |

Interpretation note: A precise model output can still be fragile. The more value depends on distant growth or terminal assumptions, the more important sensitivity testing becomes.

Intrinsic Value vs Market Price, Fair Value, Equity Value, and Enterprise Value

Intrinsic value is often confused with nearby valuation concepts because all of them can appear in the same company analysis. The distinctions matter because each concept answers a different question.

| Concept | Main question | Boundary |

|---|---|---|

| Intrinsic value | What might the business or share be worth under a set of valuation assumptions? | It is a model-based estimate, not a market quote or recommendation. |

| Market price | Where are shares currently trading? | It is observable, but it may reflect short-term flows, sentiment, liquidity, or changing expectations. |

| fair value language | What reference value is being used for reporting, exchange, or market-comparison purposes? | It can overlap with valuation work, but it is not always the same as a private intrinsic-value estimate. |

| equity value for common shareholders | What value belongs to common shareholders after other claims are considered? | It is a claim-mapping concept, not automatically a full investment conclusion. |

| enterprise value | What is the value of the operating business available to all capital providers? | It must be bridged to equity value before making a common-shareholder or per-share interpretation. |

Simple Intrinsic Value Example in Context

A company may report stable revenue and rising accounting earnings, but the intrinsic value estimate still depends on whether those earnings turn into durable free cash flow. If the estimate assumes higher margins, lower reinvestment needs, and a lower discount rate at the same time, the result may look attractive before the assumptions have been tested.

The estimate becomes more defensible when cash conversion supports reported earnings, growth assumptions match reinvestment needs, the discount rate reflects business risk, and the diluted share count is not ignored. The estimate remains fragile when most of the value comes from one optimistic growth path or from a calculator output whose inputs are not explained.

When Intrinsic Value Can Mislead

Intrinsic value becomes less useful when the model output is treated as proof instead of as an estimate. A higher estimate is only as strong as the cash-flow base, growth assumption, discount rate, terminal assumption, and share-count treatment behind it.

Common mistake: Treating one model output as proof that a stock is attractive. A valuation gap can be a useful research signal, but it still needs assumption review, business-quality evidence, balance-sheet context, and risk interpretation.

Several situations require extra caution: unstable cash flows, cyclical margins near a peak, weak cash conversion, large terminal-value dependence, changing debt levels, dilution risk, or business models where near-term growth requires heavy reinvestment.

Calculator outputs can be useful for organizing inputs, but they do not remove the need to understand those inputs. The analytical work is not only the final number; it is the reason each assumption belongs in the model.

FAQ

What is intrinsic value in simple terms?

Intrinsic value is an estimate of what a business or share may be worth based on expected cash flows, growth, risk, and other valuation assumptions.

Is intrinsic value the same as market price?

No. Market price is the observable trading price. Intrinsic value is an analytical estimate, so it can be above, below, or close to market price depending on the assumptions used.

How is intrinsic value usually estimated?

It is often estimated with valuation methods that connect cash flows, growth, risk, terminal value, capital structure, and share count. A discounted cash flow model is one common method, but the quality of the assumptions matters more than the label of the model.

Does a higher intrinsic value estimate mean a stock should be bought?

No. A higher estimate can justify further research, but it does not by itself create an investment decision. The assumptions, business quality, risks, and available alternatives still need to be evaluated.