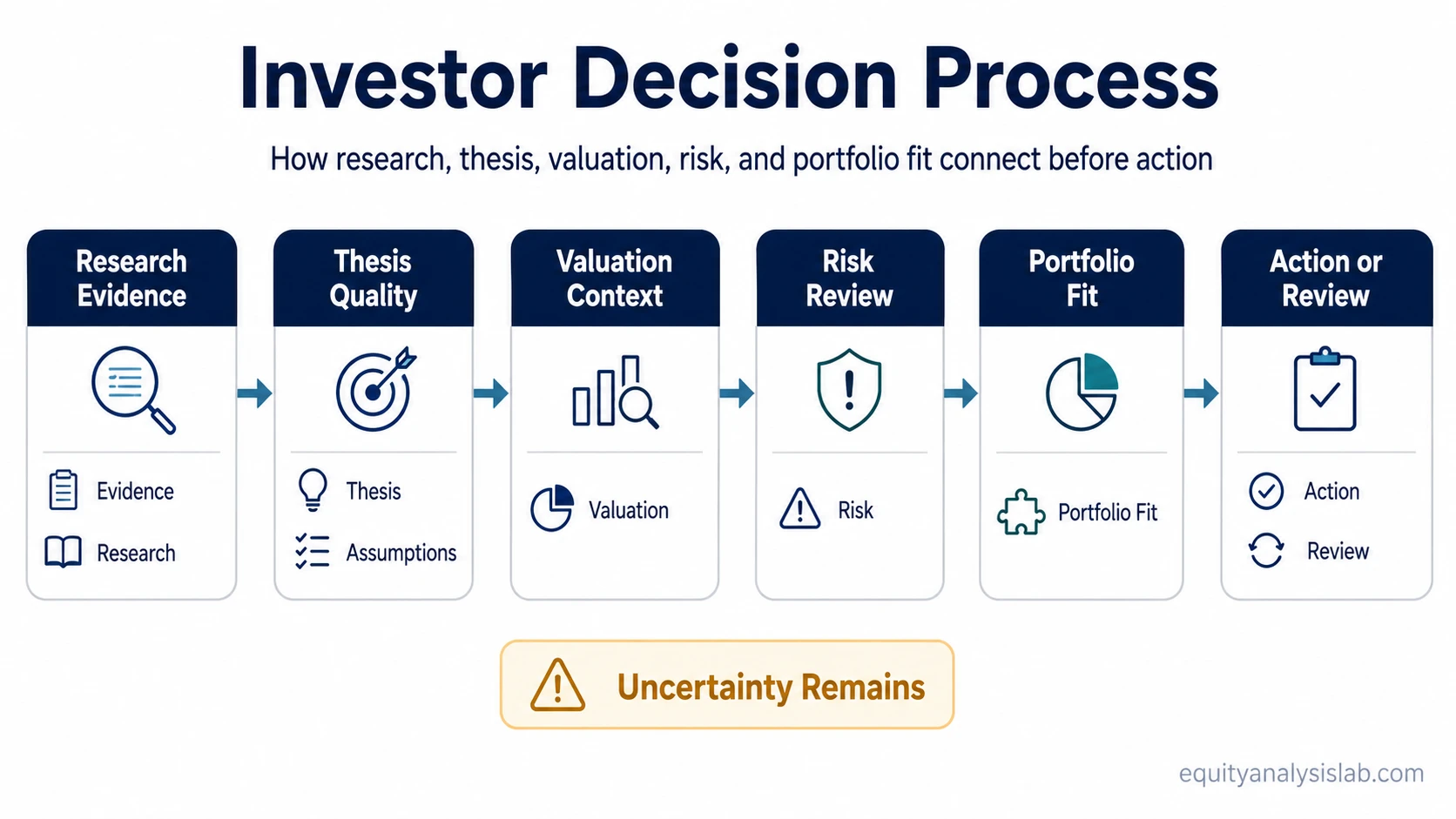

Investor decision making is the process of turning research, valuation, thesis quality, risk, and portfolio context into a clear investment action, watchlist decision, or rejection.

It is not one checklist and not a single moment of conviction. A useful decision process separates the reason to care, the evidence behind the idea, the valuation context, the risks that could weaken the case, and the role the position would play in a portfolio.

The purpose is to avoid jumping from an interesting stock idea straight to action. A stronger process makes the investor decide what is known, what is assumed, what still needs research, and what would change the conclusion.

Key Points

- Investor decision making connects evidence, thesis quality, valuation, uncertainty, and portfolio role.

- The process can lead to several outcomes: buy, wait, keep researching, hold, reduce, sell, or reject the idea.

- A good framework does not remove uncertainty. It makes the assumptions and trade-offs visible before capital is committed.

- Research can support a case, but risk limits and portfolio role decide whether the idea belongs in the investor’s process.

What Investor Decision Making Includes

An investor decision usually starts with a question: does the business, valuation, risk profile, and portfolio role justify further action? The answer depends on several inputs working together rather than one attractive metric or one persuasive story.

| Decision input | What it tests | Common weak point |

|---|---|---|

| Research evidence | Whether the investor understands the business, financials, industry position, and key assumptions. | The idea is based on a narrative before the financial evidence is strong enough. |

| Thesis quality | Whether there is a clear reason the investment could create value over the intended time horizon. | The thesis sounds attractive but does not define what would prove it wrong. |

| Valuation context | Whether the expected return is reasonable relative to growth, cash flow, risk, and alternatives. | The valuation uses assumptions that are precise in the model but fragile in reality. |

| Risk and uncertainty | Whether downside drivers, balance-sheet risk, competitive pressure, dilution, or execution risk are visible. | The decision treats uncertainty as a detail instead of a core part of the case. |

| Portfolio fit | Whether the idea has a clear role alongside existing holdings, concentration, liquidity needs, and time horizon. | The stock looks interesting alone but does not improve the overall portfolio structure. |

| Action discipline | Whether the next step is clear: buy, wait, hold, reduce, sell, reject, or continue research. | The investor confuses interest in an idea with permission to act immediately. |

The Main Stages of an Investor Decision Process

A practical investor decision process moves from understanding to judgment. Each stage should narrow the question instead of adding more disconnected information.

| Stage | Main question | Possible result |

|---|---|---|

| Idea screening | Is there a business, valuation, quality, or portfolio reason to study this further? | Add to research list or reject quickly. |

| Research workflow | What facts, filings, financial statements, and business drivers matter most? | Move into deeper research workflows or stop if the evidence is too weak. |

| Thesis development | What must be true for the investment case to work? | Develop a thesis, identify missing evidence, or reject the idea. |

| Valuation and risk review | Does the potential return compensate for uncertainty and downside risk? | Keep analyzing, adjust assumptions, or decide the margin is not sufficient. |

| Portfolio fit | Does the idea improve the portfolio, or does it add unwanted concentration and complexity? | Define the position role, wait, avoid, or compare the idea against existing holdings. |

| Decision rule | What action is justified now, and what would change the decision later? | Buy, hold, sell, wait, reduce, monitor, or reject. |

Where Each Decision Path Leads

Investor decisions become clearer when each question leads to the right next process. A research problem, a thesis problem, a buy decision, and a sell decision are related, but they are not the same job.

| Decision need | Use this path when | Next concept |

|---|---|---|

| Deciding whether an idea deserves action | The research is strong enough to consider position entry, but timing, valuation, and risk still need structure. | buy process |

| Building the evidence base | The investor needs a repeatable way to move from raw information to business understanding. | investment research process |

| Organizing the research workflow | The problem is not one stock decision yet; it is how to collect, compare, and prioritize research inputs. | research workflows |

| Turning evidence into a clear case | The investor understands the business but still needs to define what must happen for the idea to work. | thesis development |

| Writing the investable case | The decision depends on a clear statement of value drivers, risks, assumptions, and invalidation points. | investment thesis |

| Reviewing an existing position | The question is no longer whether the idea is interesting, but whether the original case still holds. | sell process |

How Research, Thesis, and Action Fit Together

Research collects and tests the evidence. Thesis development turns that evidence into a clear investment case. The buy or sell decision applies that case to price, downside, alternatives, and portfolio role.

A stock can be interesting without being actionable. A business can be high quality but too expensive. A valuation can look attractive while the case remains incomplete. A thesis can also remain a scenario until the evidence is strong enough to monitor and review.

A stronger investor decision separates these layers. The reason to care is not the same as proof. The thesis is not the same as position role. A sell decision is not always a negative view on the company; it can reflect changed assumptions, better alternatives, portfolio concentration, or a risk profile that no longer fits.

A Simple Investor Decision Framework

A compact decision framework can organize the investment question, but it should not be treated as a formula that produces certainty.

| Framework question | What a stronger answer includes |

|---|---|

| Why does the idea deserve attention? | A clear business, valuation, quality, cash-flow, or portfolio reason. |

| What evidence supports the case? | Financial statement evidence, business model analysis, earnings quality, or other research inputs. |

| What assumptions drive the decision? | Growth, margins, reinvestment, competitive position, valuation multiple, or cash-flow durability. |

| What could weaken or break the thesis? | Specific risks, evidence gaps, balance-sheet issues, dilution, changing industry conditions, or execution problems. |

| What role would the position play? | Core holding, smaller satellite idea, watchlist candidate, replacement candidate, or rejected idea. |

| What action is justified now? | Buy, wait, hold, reduce, sell, continue research, or reject. |

Example Scenario

An investor may find a company with improving revenue growth, healthy margins, and a strong market position. That can justify deeper research, but it does not automatically justify buying the stock.

The decision changes if cash conversion is weak, debt risk is rising, or the valuation already assumes unusually strong growth. In that case, the stronger outcome may be to keep the company on a watchlist, define what evidence would improve the case, or reject the idea until the thesis becomes easier to verify.

What Can Weaken an Investment Decision

No decision framework removes uncertainty. Its value is that it exposes uncertainty before the investor acts.

- Weak evidence: The conclusion depends on a story more than financial or business evidence.

- Unclear thesis: The investor cannot explain what must be true for the investment to work.

- Valuation fragility: The outcome depends on optimistic growth, margin, or multiple assumptions.

- Ignored downside: Balance-sheet risk, dilution, cyclicality, customer concentration, or competitive pressure is treated as secondary.

- Poor portfolio fit: The idea increases concentration or complexity without improving the overall portfolio.

- No review rule: The investor knows why they entered but not what would make them change the decision.

Related Investor Workflow Concepts

Related investor workflow concepts separate the main jobs inside the decision process. Research builds the evidence base, thesis development defines the case, the buy process tests actionability, and the sell process reviews whether the original case still deserves capital.

FAQ

Is investor decision making the same as stock picking?

No. Stock picking is the act of selecting investments. Investor decision making is the broader process that tests research, thesis quality, valuation, risk, portfolio fit, and review rules before deciding what action is justified.

What is the difference between a buy decision and an investment thesis?

An investment thesis explains why an idea may create value. A buy decision asks whether the thesis, valuation, risk, and portfolio role justify committing capital now.