An annual report should be read as a structured disclosure map: business model, management explanation, financial statements, risks, notes, and 10-K detail each answer a different investor question.

The useful reading order is not cover to cover. Start with what the company says it does, compare that explanation with the numbers, then check the risks and notes that can change the interpretation.

Annual report definition: An annual report is a company disclosure document that summarizes the business, management’s discussion of results, financial statements, key risks, and other information shareholders can use to review the company.

For investors, the annual report is not a final conclusion about quality or value. It is the first map for deciding which claims need to be checked against earnings quality, the balance sheet, cash flow, and the notes to the financial statements.

Key points when reading an annual report

- An annual report is a starting map, not proof that a company is attractive.

- The shareholder letter and MD&A should be checked against the statements, risks, and notes.

- The income statement, balance sheet, and cash flow statement answer different investor questions.

- In the United States, the Form 10-K usually gives more detailed disclosure than a glossy annual report.

- The next step after the first read is deeper analysis of earnings quality, financial position, and cash generation.

Annual report vs 10-K

An annual report and a Form 10-K can overlap, but they are not always the same reading experience. A company’s annual report may include shareholder-facing narrative, selected visuals, and management framing. A U.S. Form 10-K is a regulatory filing with a more standardized disclosure structure.

| Document | Main purpose | Investor reading use | Main limitation |

|---|---|---|---|

| Annual report | Shareholder communication and yearly business summary | Useful for understanding the company’s story, management framing, performance highlights, and financial statements | The presentation may emphasize the company’s preferred narrative |

| Form 10-K | Standardized annual regulatory disclosure in the U.S. | Useful for reviewing business description, risk factors, MD&A, audited financial statements, and notes in more detail | Longer and more technical, especially for beginners |

In U.S. company research, the Form 10-K is often the more standardized source for disclosure review because it follows SEC filing requirements. A shareholder-facing annual report may overlap with it or incorporate parts of it, but the exact presentation can vary by company.

Where to start reading an annual report

The first pass should answer four questions in order: what the company does, how management explains the year, whether the numbers support that explanation, and what could weaken the interpretation.

| Reading step | What to look for | Why it matters |

|---|---|---|

| Business description | Products, services, segments, customers, geography, and revenue drivers | Financial numbers are easier to interpret when the business model is clear first |

| Management discussion and analysis | Management’s explanation of revenue, margins, costs, cash flow, capital spending, and known trends | It shows how management frames performance, but the explanation still needs verification |

| Financial statements | Income statement, balance sheet, cash flow statement, and statement of equity where available | The statements test whether the story is visible in revenue, profitability, assets, liabilities, and cash generation |

| Risk factors | Customer concentration, debt, regulation, competition, cyclicality, supply chain, technology, litigation, or financing risks | Risks show what could make a clean narrative less reliable |

| Notes and audit opinion | Accounting policies, revenue recognition, debt terms, leases, contingencies, share-based compensation, and auditor language | Important interpretation details often appear outside the headline statements |

For U.S. Form 10-Ks, this reading sequence commonly maps to Item 1 for Business, Item 7 for MD&A, and Item 8 for Financial Statements and Supplementary Data. Outside U.S. filings, labels and presentation can differ, so the same reading logic matters more than the document label.

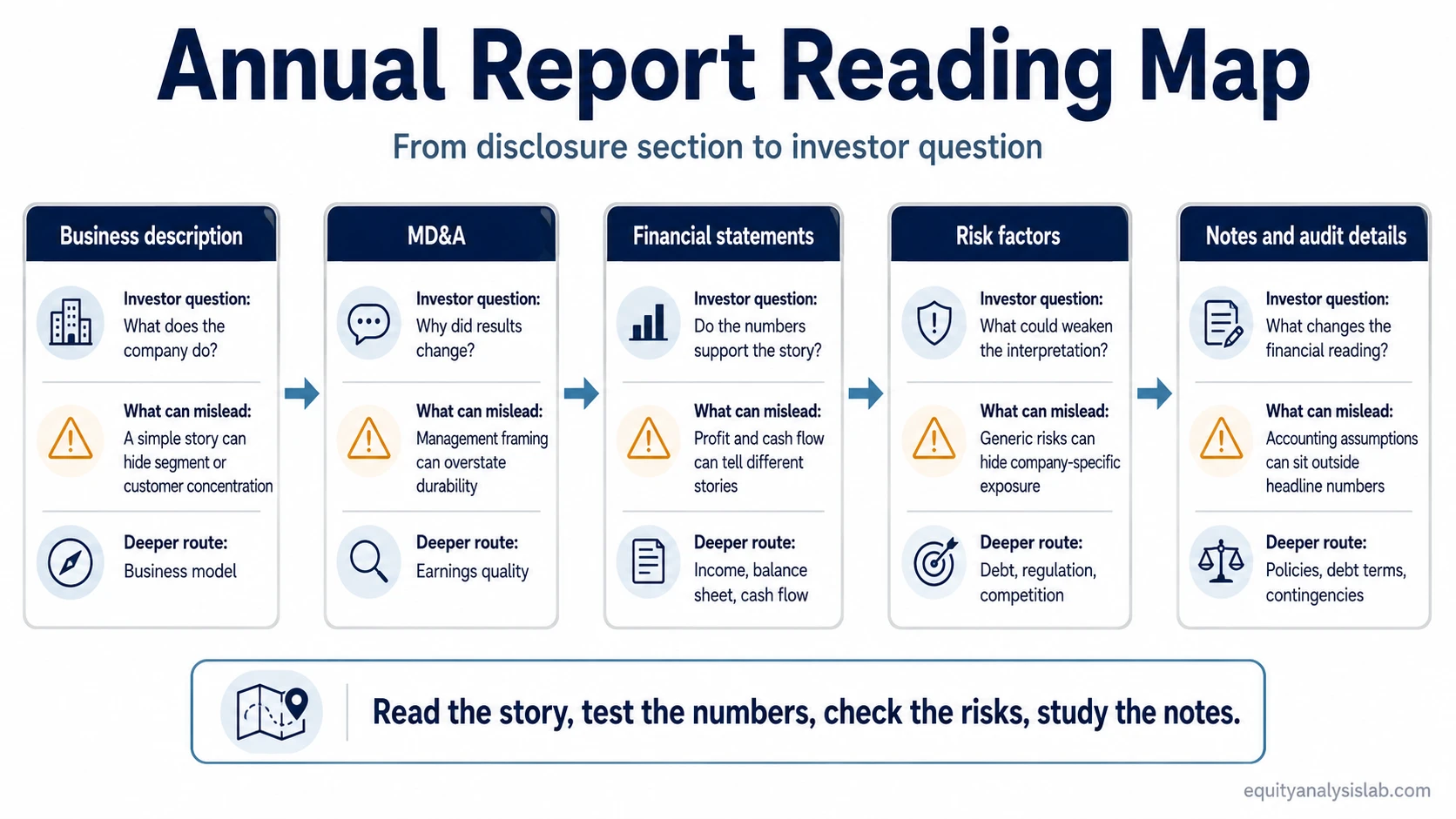

Annual report section-to-investor-question map

A useful annual report review connects each section to a specific investor question. A section becomes more useful when it is tested against what could mislead the interpretation.

| Report section | Investor question it helps answer | What can mislead | What to study next |

|---|---|---|---|

| Shareholder letter | How does management describe the year and the company’s priorities? | Positive framing can make temporary improvement sound more durable than it is | Compare the narrative with quality of earnings |

| Business overview | How does the company make money? | Segment descriptions can hide which activities actually drive profit or cash flow | Check revenue mix, margin structure, and business-model quality |

| MD&A | Why did revenue, margins, cash flow, or capital spending change? | Management may emphasize one explanation while other factors are visible in the statements | Compare management’s explanation with statement trends |

| Income statement | Is the company growing revenue and converting sales into profit? | Accounting profit can improve even when cash conversion is weak or one-time items are important | Review the income statement in context |

| Balance sheet | What does the company own, owe, and rely on financially? | A profitable company can still carry liquidity, debt, or working-capital risk | Review the balance sheet |

| Cash flow statement | Is reported profit turning into cash? | Strong net income can look less convincing if operating cash flow is weak or capital spending is heavy | Compare profit with the cash flow statement |

| Risk factors | What could weaken the investment thesis? | Risk sections are often long, but repeated or unusually specific risks deserve attention | Separate generic legal disclosure from business-specific risk |

| Notes to financial statements | Which accounting details change the meaning of the headline numbers? | Revenue recognition, debt terms, leases, pension assumptions, or contingencies can change interpretation | Use the notes to check whether the statements are as clean as they first appear |

| Audit opinion | Did the auditor raise any qualification, emphasis, or going-concern concern? | A clean opinion does not make an investment conclusion; it addresses the financial reporting standard | Use audit language as a reporting-quality check, not as an investment conclusion |

Financial statements inside the annual report

The financial statements are the test layer of the annual report. Management may describe a strong year, but the statements show whether that strength appears in profitability, financial position, and cash movement.

| Statement | Main question | Useful first check | Common misread |

|---|---|---|---|

| Income statement | Did the company generate revenue and profit? | Revenue growth, gross margin, operating margin, net income, and unusual items | Treating profit growth as automatically high quality |

| Balance sheet | How strong or fragile is the financial position? | Cash, debt, working capital, inventory, receivables, equity, and obligations | Ignoring leverage or liquidity because earnings looked good |

| Cash flow statement | Did the business generate cash? | Operating cash flow, capital expenditures, free cash flow, debt repayment, dividends, and buybacks | Assuming accounting profit and cash generation are the same thing |

A simple first-pass test is to compare the income statement with cash flow. A company can report accounting profit while cash flow tells a weaker story. That does not automatically mean the business is poor quality, but it does mean the profit needs more checking before it becomes part of an investment thesis.

Annual reports are disclosure documents, not neutral verdicts

An annual report can be accurate and still selective in emphasis. Management chooses how to describe the year, which achievements to highlight, and which risks to frame as manageable. That is why the document should be read as evidence to compare, not as a conclusion to accept.

The practical boundary is simple: a positive narrative becomes stronger when the financial statements, notes, and risk disclosures support it. The same narrative becomes weaker when profits rely on one-time items, cash flow does not follow earnings, debt risk increases, or key assumptions are buried in the notes.

Common mistakes when reading annual reports

- Reading the shareholder letter as neutral proof: the letter can be useful, but it is management’s framing of the year.

- Skipping the notes: accounting policies, debt terms, leases, contingencies, and share-based compensation can change the interpretation of the statements.

- Treating profit as cash: net income and operating cash flow can move differently, especially when working capital, accruals, or capital spending matter.

- Ignoring risk factors: risks may look repetitive, but company-specific changes or unusually direct language can be important.

- Reading one year in isolation: annual reports become more useful when the same terms, margins, risks, and cash-flow patterns are compared across several years.

- Stopping at the headline numbers: growth, margins, and earnings need context from segments, notes, balance sheet strength, and cash conversion.

How to study the company after the first read

The first annual report pass should leave a short list of follow-up questions. The next step is to check whether reported performance is durable, financially supported, and consistent with the company’s own risk disclosures.

| Question after the first read | Why it matters | Concept to study |

|---|---|---|

| Are earnings supported by recurring operations and cash conversion? | Reported earnings can look strong even when quality is weak | Quality of earnings |

| Is the company financially resilient? | Debt, liquidity, working capital, and obligations can change risk | Balance sheet analysis |

| Is profit turning into cash? | Cash flow often reveals pressure that profit alone does not show | Cash flow statement analysis |

| Where did revenue, expenses, and margins actually change? | Profitability needs to be separated from one-time gains, cost timing, or accounting effects | Income statement analysis |

The annual report is most useful when each section is tied to a testable question. The business description explains what to analyze, MD&A explains management’s view, the statements test the numbers, the notes add accounting detail, and risk factors show what could break the thesis.

Annual report reading FAQ

What is the fastest way to read an annual report?

Start with the business overview, then read MD&A, the financial statements, risk factors, and notes. The goal is to understand the business first, then test management’s explanation against the numbers and disclosures.

Is an annual report the same as a 10-K?

Not always. In the United States, a Form 10-K is a standardized annual regulatory filing, while an annual report may include more shareholder-facing presentation. Some companies combine or closely align the two, but the 10-K usually contains the more detailed disclosure structure.

Can an annual report tell whether a stock is a good investment?

An annual report can support company analysis, but it does not answer valuation, portfolio fit, or expected return by itself. It helps identify the business model, financial condition, earnings quality, risks, and questions that need deeper review.

What should beginners not skip in an annual report?

Beginners often skip the notes, risk factors, and cash flow statement. Those sections can reveal accounting assumptions, financing risk, cash conversion issues, and business-specific risks that are not obvious from the shareholder letter or headline earnings.