Types of ETFs are categories of exchange-traded funds grouped by the exposure they hold, the strategy they follow, the asset class they track, or the structure used inside the fund. The category label is useful, but it is only the first filter. The actual portfolio, weighting method, cost, tracking behavior, liquidity, distributions, and wrapper mechanics can change how the exposure works in practice.

A broad ETF label can point in the right direction, but it does not complete the review. An equity fund, a bond fund, a commodity fund, a sector fund, and an index-tracking fund can all be ETFs, yet each one answers a different exposure question.

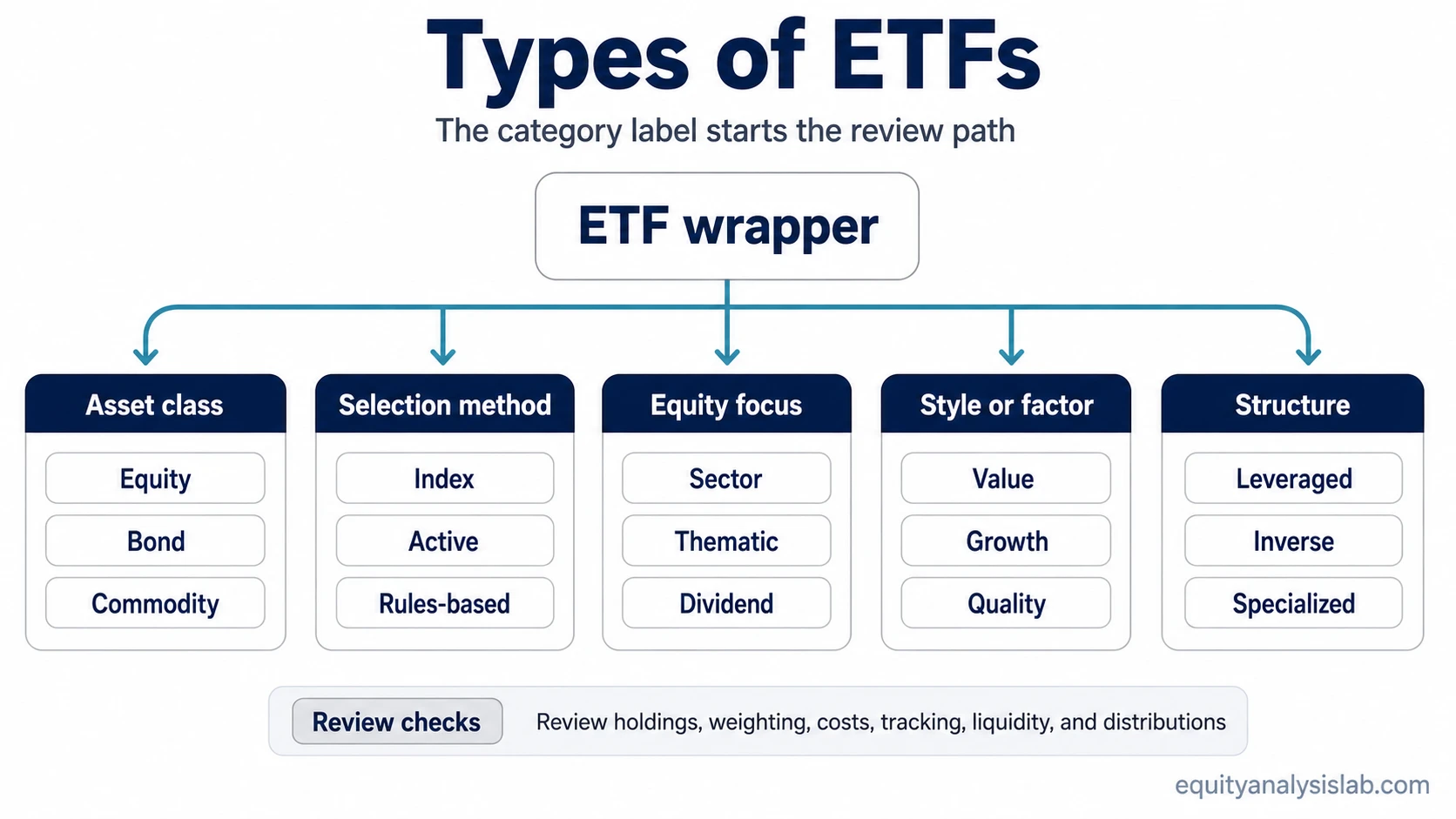

What ETF types mean

An ETF type describes the organizing principle behind the fund. Some ETF types organize exposure by asset class, such as stocks, bonds, or commodities. Others organize exposure by strategy, such as index tracking, active management, dividend focus, growth style, value style, sector concentration, or thematic selection.

The useful distinction is between the ETF category name and the fund’s underlying exposure. The label tells you where to begin the review. The holdings, weights, index or strategy rules, fees, liquidity, tracking behavior, and distribution policy tell you what the fund actually does.

Key points about ETF categories

- ETF types usually group funds by exposure, strategy, asset class, or structure.

- The same ETF label can still hide very different holdings, weights, costs, and risks.

- Index ETFs and actively managed ETFs are different selection methods, not separate asset classes.

- Sector, thematic, dividend, value, and growth ETFs narrow the equity universe in different ways.

- Leveraged and inverse ETFs require extra caution because their structure can change how the exposure behaves over time.

- Category review should be followed by checks on holdings, weighting, expense ratio, tracking difference, liquidity, spread, NAV behavior, distributions, and tax or domicile mechanics where relevant.

Main ETF type buckets

The main ETF categories can be understood by asking what the fund is trying to organize. Some ETFs organize an asset class. Some organize a selection method. Others organize a narrower investment theme, income style, market segment, or structural exposure.

| ETF type | What it organizes | What to inspect | Deeper category review |

|---|---|---|---|

| Equity ETFs | Stock exposure across a market, region, segment, or style. | Underlying companies, country exposure, sector weights, market-cap weighting, concentration, and index or strategy rules. | Use equity ETF structure when the main question is stock-market exposure. |

| Bond and fixed income ETFs | Exposure to government bonds, corporate bonds, short-duration debt, long-duration debt, or other fixed income segments. | Duration, credit quality, issuer mix, yield source, interest-rate sensitivity, liquidity, and distribution behavior. | Use the bond ETF category when the main question is fixed income exposure. |

| Commodity ETFs | Exposure to commodities, commodity-linked instruments, or commodity-related structures. | Physical holding versus futures exposure, roll mechanics, storage or custody structure, tracking behavior, and tax treatment where relevant. | Use the commodity ETF category when the exposure is tied to raw materials or commodity-linked prices. |

| Sector ETFs | Exposure to one industry sector or a defined part of the equity market. | Sector classification, top holdings, concentration, overlap with broad equity funds, weighting rules, and company-level risk. | Use the sector ETF category when the fund narrows equity exposure to one sector. |

| Thematic ETFs | Exposure built around a theme, trend, technology, demographic shift, or long-term narrative. | Theme definition, inclusion rules, holdings purity, valuation sensitivity, concentration, overlap, and whether the label matches the actual portfolio. | Review thematic exposure separately when the category starts from a story rather than a standard sector or broad index. |

| Index ETFs | Exposure designed to track a stated index or benchmark. | Index methodology, replication method, tracking difference, tracking error, rebalancing rules, cost, and liquidity. | Use index ETF analysis when the main question is how closely the fund follows a benchmark. |

| Actively managed ETFs | Exposure selected by a manager or rule set that is not simply passive index tracking. | Manager discretion, portfolio turnover, mandate limits, transparency, cost, risk controls, and performance drivers versus the benchmark. | Compare the active process with the benchmark and the fund’s stated mandate before relying on the category as a simple exposure label. |

| Dividend ETFs | Equity exposure filtered around dividend yield, dividend growth, payout history, or income characteristics. | Dividend screen, payout durability, sector concentration, valuation, distribution policy, and whether income focus reduces or increases concentration. | Use dividend ETF review when the category is built around dividend-focused equity exposure. |

| Style, factor, value, and growth ETFs | Equity exposure selected or weighted by traits such as valuation, growth, quality, momentum, size, or volatility. | Factor definition, rebalance rules, overlap with broad equity funds, sector bias, valuation sensitivity, and how the style is measured. | Use the specific style or factor category when the fund’s construction depends on a defined equity characteristic. |

| Leveraged and inverse ETFs | Exposure designed to magnify or reverse the daily movement of an index or asset. | Daily reset mechanics, compounding effects, volatility path, holding-period risk, fees, and whether the structure matches the intended use. | Treat leveraged and inverse structures as advanced ETF categories that require a separate structural review. |

How to compare ETF types without ranking them

ETF categories are not a ranking system. A bond ETF is not automatically safer than an equity ETF, a dividend ETF is not automatically higher quality than a broad equity ETF, and an index ETF is not automatically better than an actively managed ETF. Each category answers a different exposure question.

A more useful comparison starts with four questions:

- What exposure is inside? Check the holdings, asset class, sector mix, country mix, issuer mix, or commodity structure.

- How is the exposure selected and weighted? Review whether the fund follows an index, manager discretion, market-cap weighting, equal weighting, factor rules, dividend screens, or theme rules.

- What mechanics change the behavior? Look at expense ratio, tracking difference, liquidity, bid-ask spread, NAV premium or discount, distribution policy, tax treatment, and domicile where relevant.

- Which category needs deeper review? After the broad type is identified, the specific ETF category should be inspected on its own terms.

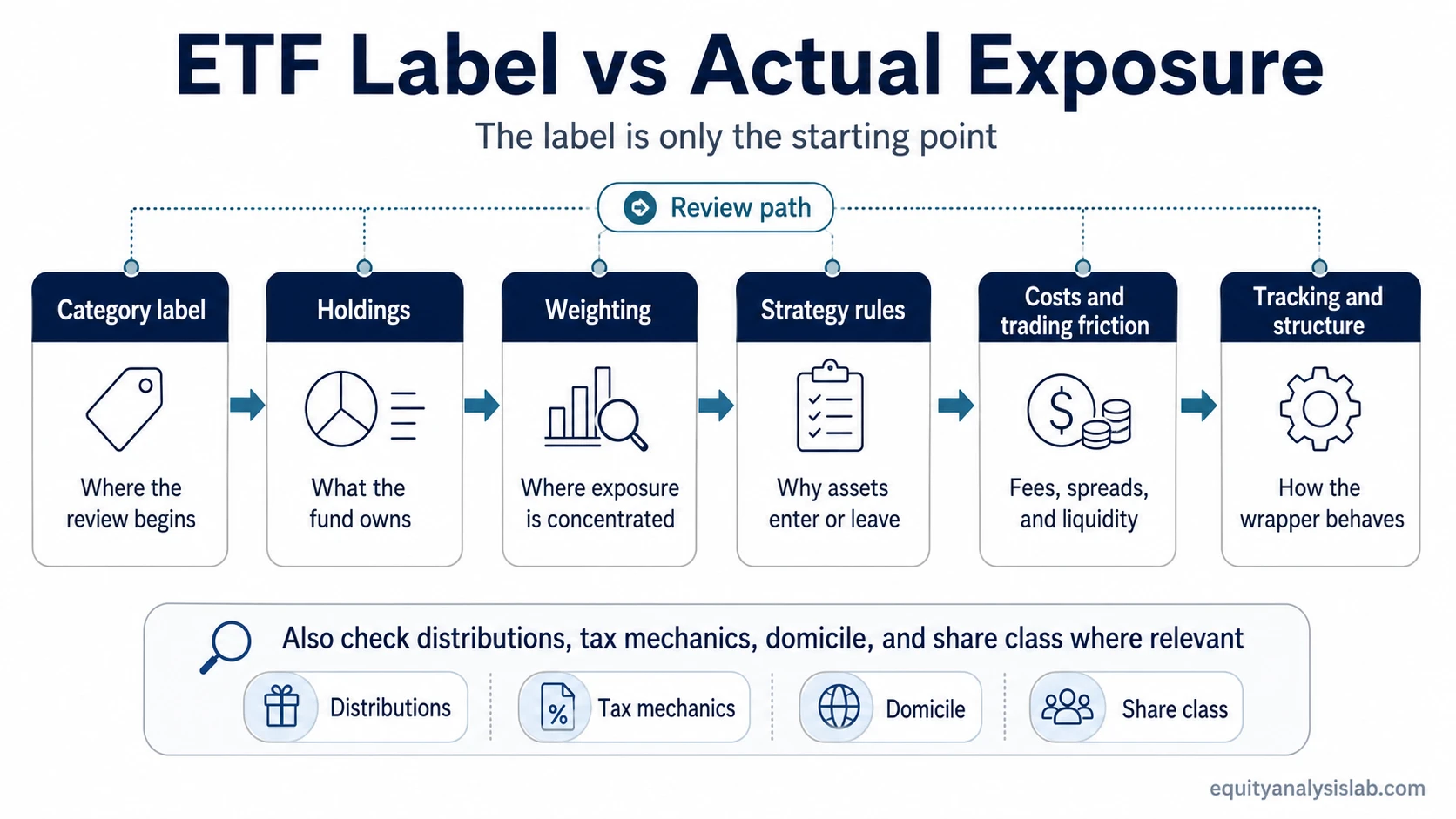

ETF type label versus actual exposure

The category label is the starting point, not the conclusion. A fund can carry a broad label while behaving differently from another fund in the same category because the holdings, weights, costs, and structure are different.

| Label check | Why it matters | What can change the result |

|---|---|---|

| Category name | Shows the broad exposure family. | The same category can include different subsegments, rules, and portfolio construction methods. |

| Holdings | Shows what the investor owns through the fund. | Two similarly named ETFs may hold different companies, bonds, commodities, or instruments. |

| Weighting | Shows where the largest exposure sits. | Market-cap weighting, equal weighting, factor weighting, and active weighting can create different concentration profiles. |

| Selection method | Shows why assets enter or leave the fund. | Index rules, manager discretion, dividend screens, sector classifications, and thematic rules can lead to different portfolios. |

| Cost and trading friction | Shows how much of the exposure may be reduced by fees or transaction costs. | Expense ratio, bid-ask spread, fund liquidity, and trading volume can affect the practical ownership profile. |

| Tracking and structure | Shows whether the ETF behaves like the exposure it claims to follow. | Tracking difference, replication method, derivatives, futures, leverage, inverse exposure, and premium or discount behavior can all matter. |

| Distributions and tax mechanics | Shows how income, capital gains, withholding, and fund domicile can affect interpretation. | Distribution policy, accumulating versus distributing share classes, tax domicile, and local tax rules can change the ownership profile. |

A simple example of why the label is not enough

Two ETFs can both use the same broad category label and still give different exposure. One may spread holdings across hundreds of securities, while another may concentrate most of its weight in a smaller group of large positions. One may follow a transparent index, while another may rely on an active process or a narrower screen.

The label can make the two funds look similar at first glance. The actual review begins when holdings, weights, strategy rules, costs, tracking behavior, liquidity, and distributions are compared side by side.

Beginner mistake: treating the ETF label as the whole analysis

A common mistake is stopping after the category name. The label may say equity, bond, dividend, commodity, sector, or index, but the label does not show the full exposure by itself.

This mistake is most visible when a category contains many different construction methods. A dividend-focused ETF may be concentrated in a few sectors. A sector ETF may overlap heavily with a broad market fund. A commodity ETF may hold physical exposure, futures exposure, or a structure that behaves differently from the spot commodity. An index ETF may track an index cleanly, but the index methodology still determines what the fund owns.

The better sequence is to use the label as a filter, then test the portfolio and mechanics before drawing conclusions.

Key checks before relying on an ETF category

The ETF type tells you which review path to use. The following checks help separate a category name from the fund’s practical exposure.

| Check | Question to ask | Why it matters |

|---|---|---|

| Holdings | What assets, companies, bonds, commodities, or instruments are inside? | The holdings define the real exposure behind the label. |

| Index or strategy | Does the ETF track an index, follow an active process, or apply a rules-based screen? | The selection method explains why the portfolio looks the way it does. |

| Weighting | Are positions market-cap weighted, equal weighted, factor weighted, or actively weighted? | Weighting can create concentration even when the fund appears diversified. |

| Expense ratio | What is the ongoing cost of holding the ETF? | Costs reduce the return captured from the underlying exposure. |

| Tracking difference | How closely has the ETF followed the index or exposure it claims to represent? | Tracking behavior shows whether the fund has delivered the intended exposure after costs and mechanics. |

| Liquidity and spread | How actively does the ETF trade, and how wide is the bid-ask spread? | Trading friction can matter even when the underlying idea is sound. |

| NAV behavior | Does the ETF trade close to net asset value, or can premiums and discounts appear? | Premiums and discounts can affect entry and exit pricing, especially in less liquid segments. |

| Distribution policy | Does the ETF distribute income, accumulate it, or follow a specific payout policy? | Distribution treatment can affect income expectations and tax interpretation. |

| Tax and domicile mechanics | Where is the ETF domiciled, and what tax or withholding rules may apply? | Tax treatment can differ by investor location, fund domicile, asset class, and distribution structure. |

Review path by ETF category

After the broad type is clear, the category with the main exposure question should be inspected first.

- Stock-market exposure: Review equity ETF structure, then inspect geography, sector mix, holdings, concentration, and weighting.

- Fixed income exposure: Review bond ETF structure, then inspect duration, credit quality, issuer mix, yield source, and liquidity.

- Commodity-linked exposure: Review commodity ETF structure, then inspect whether the fund uses physical holdings, futures, derivatives, or another wrapper.

- Sector concentration: Review sector ETF structure, then inspect overlap with broad equity funds and concentration in the largest holdings.

- Benchmark tracking: Review index ETF structure, then inspect methodology, tracking difference, costs, and rebalancing rules.

- Dividend-focused exposure: Review dividend ETF structure, then inspect dividend screen, payout durability, sector bias, valuation, and distribution policy.

What ETF type comparisons cannot tell you

ETF categories help organize the research process, but they do not decide whether a fund is suitable, cheap, diversified, tax-efficient, or low risk. Those questions depend on the investor’s objective, portfolio context, tax situation, time horizon, risk capacity, and the specific ETF being reviewed.

A category map can narrow the field, but it cannot replace fund-level analysis. The same label can point to different portfolios, different risks, different costs, and different ownership profiles.

FAQ

Is every ETF an index ETF?

No. Many ETFs track indexes, but an ETF is a wrapper, not automatically an index strategy. Some ETFs are actively managed, some use rules-based screens, and some use structures designed around commodities, leverage, inverse exposure, or other specialized objectives.

Are leveraged ETFs long-term exposure tools?

Leveraged ETFs need separate review because many are designed around daily exposure, daily reset mechanics, and compounding effects. Their long-term behavior can differ from a simple multiple of the underlying index, especially when volatility is high.

Can two ETFs in the same category behave differently?

Yes. Two ETFs can share a category label but differ in holdings, weights, costs, liquidity, tracking, distributions, tax treatment, and structure. The category label helps identify the review path, but the fund details determine the exposure.

What is the first thing to check after the ETF type?

Start with holdings and weighting. Those two checks show what the fund owns and where the largest exposures sit. After that, review strategy rules, cost, tracking behavior, liquidity, distributions, and structure.