Investor psychology is the study of how bias, emotion, mental shortcuts, and decision pressure can affect how investors interpret evidence and make investment decisions.

The practical use is to identify whether bias, emotional pressure, anchoring, or weak decision discipline is changing which evidence an investor accepts, ignores, or overweights before making an investment decision.

Definition: Investor psychology describes the behavioral side of investment decisions, including how investors react to uncertainty, volatility, recent information, prior beliefs, and pressure to act.

Key Points

- Investor psychology connects behavioral finance to practical investment decisions.

- Bias can change which evidence receives attention before valuation, risk, or portfolio review is complete.

- Emotion can pressure timing, position size, confidence, patience, and willingness to update a view.

- Decision discipline helps separate evidence from reaction, but it does not guarantee better results.

What Investor Psychology Means in Investment Decisions

Investor psychology affects the evidence-filtering step before an investment conclusion is formed. A company may have financial statements, valuation inputs, earnings expectations, risk factors, and market prices, but the investor still has to decide which evidence deserves weight.

Behavioral finance studies these decision patterns. In an investor process, that means watching how bias, emotion, and mental shortcuts can influence interpretation before the final conclusion is reached.

A disciplined investor does not treat psychology as a replacement for analysis. Psychology is a review layer that asks whether the decision process is being pulled away from evidence by comfort, fear, recent price action, prior estimates, or social pressure.

How Investor Psychology Shows Up Before the Spreadsheet

Many investor psychology problems appear before the model, checklist, or valuation work begins. The investor may already prefer one conclusion, dislike one type of evidence, or feel pressure to act before the full review is complete.

One common scenario is an investor who sees a sharp price decline and immediately treats the lower price as better value. That reaction may be reasonable to investigate, but it is incomplete if the investor has not checked whether earnings quality, business risk, debt, dilution, or a changed thesis explains the decline.

The same problem can appear in the opposite direction. A rising price can make recent evidence feel stronger than it is. Investor psychology becomes useful when the decision is translated into observable checks:

- What triggered the decision?

- Which evidence is being ignored?

- Which evidence is being overweighted?

- Is emotion changing timing, confidence, or position size pressure?

- Was the checklist skipped?

- What review trigger would change the interpretation?

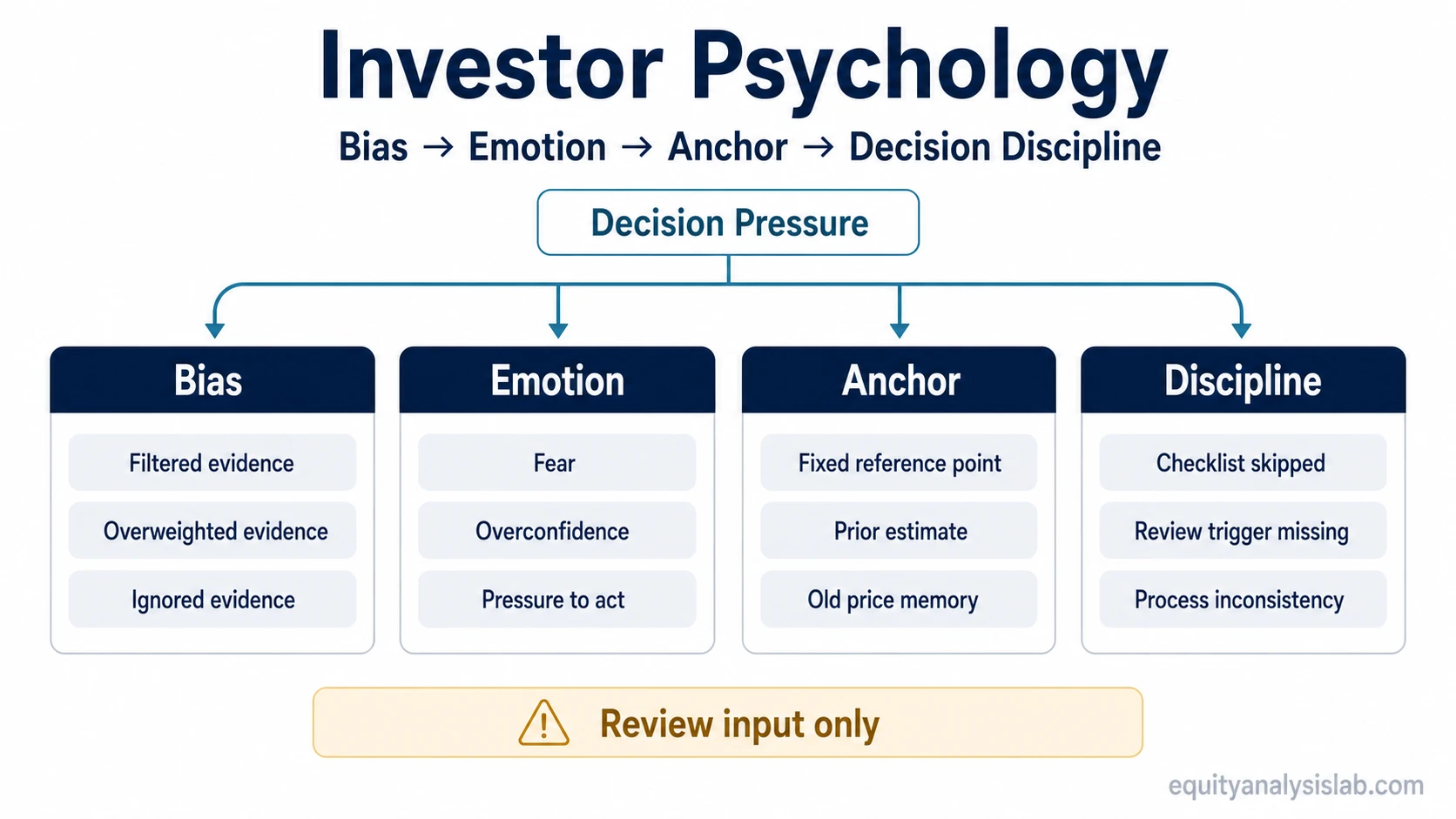

Investor Psychology Decision Areas: Biases, Emotions, and Decision Discipline

Different decision problems require different review tools. Some problems come from cognitive shortcuts, some from emotional pressure, and some from the absence of a repeatable decision process.

Start with the decision problem that is most visible: filtered evidence points toward bias review, urgent reaction points toward emotional investing, fixed reference points point toward anchoring, and inconsistent review points toward decision discipline.

| Investor decision problem | What it can distort | Concept to study next | Decision use |

|---|---|---|---|

| Evidence is filtered to support an existing view | Research quality, thesis review, and willingness to update | behavioral biases | Identify recurring mental shortcuts before they shape the conclusion. |

| The investor reacts to volatility, regret, or pressure to act | Timing pressure, confidence, position size, and patience | emotional investing | Separate evidence-based review from emotional urgency. |

| A prior estimate becomes the reference point for every later decision | Valuation updates, downside review, and new evidence weighting | anchoring bias | Check whether old numbers are still justified by current facts. |

| The process changes from one decision to the next | Checklist consistency, risk review, and post-decision learning | decision discipline | Use a repeatable review structure before, during, and after decisions. |

What Investor Psychology Does Not Prove

Limitation: Investor psychology does not prove that an investor is wrong, irrational, or unable to make a sound decision. It also does not prove the correct portfolio, the right allocation, the best investment, or a future return outcome.

Bias awareness is useful only when it improves the review process. An investor can feel fear and still be responding to real risk. An investor can feel confidence and still have evidence that supports the view. The distinction depends on whether the decision is anchored in current evidence, realistic uncertainty, and a consistent review process.

Psychology can also change across companies, sectors, time horizons, and market environments. A reaction that is unhelpful in one situation may be a valid warning in another if the underlying evidence has changed.

FAQ

What is investor psychology in simple terms?

Investor psychology is the way bias, emotion, mental shortcuts, and decision pressure can affect how investors interpret evidence and make investment decisions.

Is investor psychology the same as behavioral finance?

They are closely related. Behavioral finance is the broader field that studies how behavior affects financial decisions, while investor psychology focuses on how those patterns appear in an investor’s own decision process.

Does understanding investor psychology guarantee better investment results?

No. It can improve review discipline and make decision risks easier to notice, but it cannot guarantee returns, prove suitability, or identify the correct investment.

Can emotion ever be useful in investing?

Emotion is not automatically wrong. It becomes risky when it replaces evidence, compresses review time, changes position size pressure, or prevents an investor from updating a view when facts change.