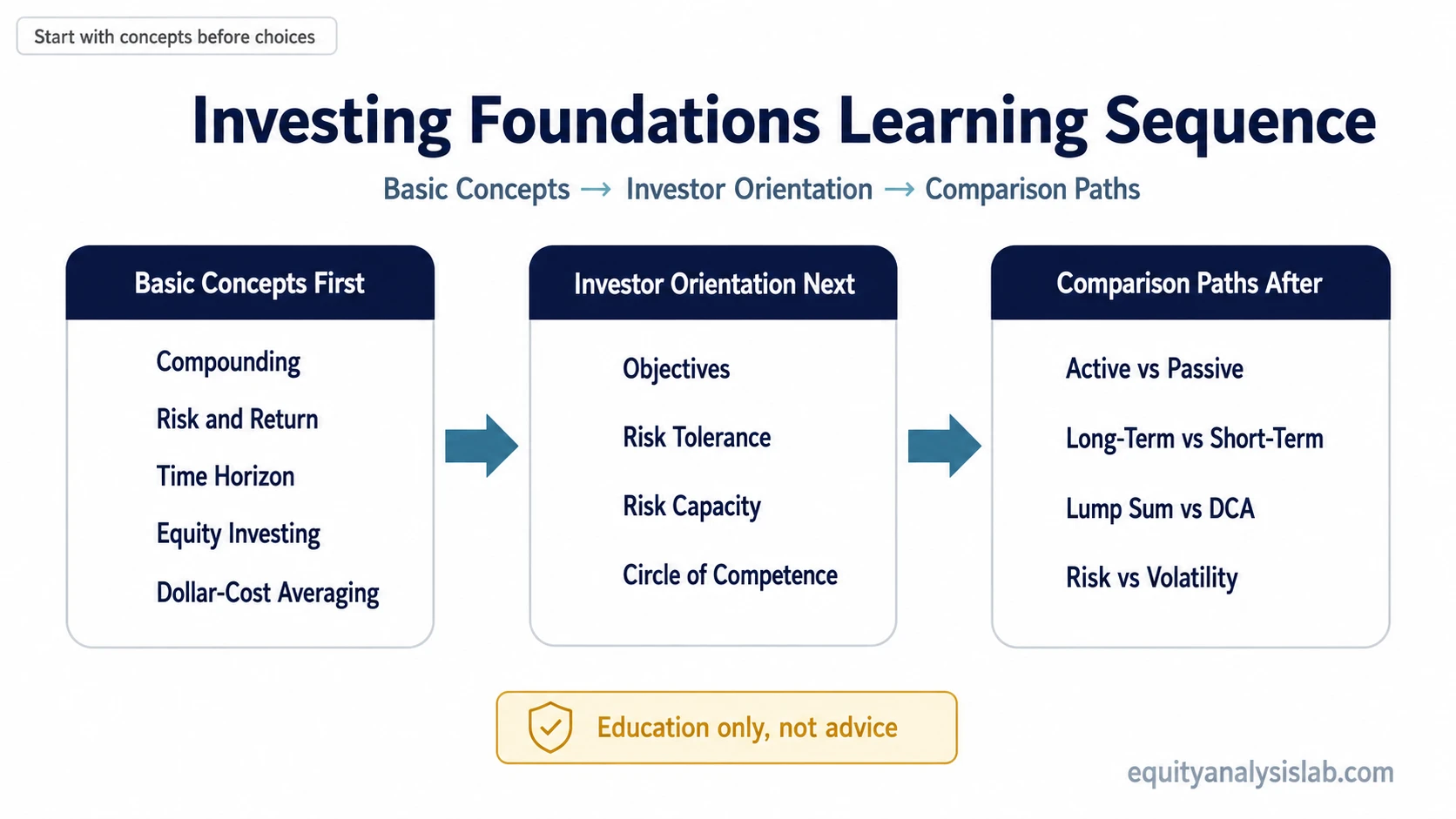

Investing foundations should start with the basic concepts that shape every later decision: compounding, risk and return, and time horizon.

Those concepts come before comparisons, product choices, portfolio construction, valuation work, or individual stock selection. A strong starting sequence makes time, uncertainty, ownership, and decision boundaries easier to understand before any single concept is treated as a recommendation.

Saving and investing are related, but they do not do the same job. Saving usually protects liquidity and near-term flexibility. Investing accepts uncertainty in exchange for possible long-term growth, income, or ownership exposure. Concept order matters because the first task is not choosing an investment, but understanding the ideas that shape later choices.

Key Points

- Start with compounding, risk and return, and time horizon before moving into more specific investing decisions.

- Use equity investing and dollar-cost averaging as follow-on concepts, not as shortcuts around risk.

- Move into investor objectives, risk tolerance, risk capacity, and circle of competence after the basic concept layer is clear.

- Use comparison topics only after the underlying concepts are understood.

- Investing concepts can improve decision structure, but they do not remove uncertainty or guarantee outcomes.

Start With Basic Investing Concepts

The first sequence through investing foundations should be simple: understand how long-term growth can compound, how return cannot be separated from risk, and how time horizon changes the way uncertainty is interpreted. These are not advanced topics. They are the base layer for reading the rest of the investing material without turning education into a decision rule.

Core Concepts is the best starting point when the basic language of investing needs to come before objectives, behavior, comparisons, or portfolio decisions.

| Learning job | Start with | Why it comes first |

|---|---|---|

| Understand how time affects growth | compounding over time | Compounding explains how repeated gains or reinvested returns can build on earlier capital, while still depending on assumptions, time, and risk. |

| Understand uncertainty | Risk and return | Higher possible return usually comes with uncertainty, drawdown risk, business risk, valuation risk, or other tradeoffs. |

| Understand decision context | Time horizon | A short time horizon and a long time horizon can make the same investment exposure feel very different. |

| Understand ownership exposure | Equity investing | Equity ownership connects the investor to business performance, valuation, cash flows, and market pricing. |

| Understand implementation rhythm | Dollar-cost averaging | DCA can help structure repeated purchases, but it does not guarantee a better result or remove market risk. |

Basic Concepts First

The basic concept layer prevents a common mistake: jumping from “I want to invest” directly into products, stocks, forecasts, or performance comparisons. Compounding, risk and return, and time horizon create the vocabulary for asking better questions before those choices appear.

A useful beginner sequence treats compounding as the growth mechanism, risk and return as the uncertainty frame, and time horizon as the decision boundary. Equity investing and dollar-cost averaging can come after that because both depend on ownership exposure and time-based uncertainty.

Important limitation: A concept sequence is educational, not personal advice. It can help organize learning, but it does not identify a suitable investment, remove risk, or produce a forecast.

Investor Orientation Comes Next

After the basic concept layer, the next question is not “which investment is best?” The next question is what kind of investor decision is being made. Objectives, risk tolerance, risk capacity, and circle of competence help separate a general investing idea from a decision that fits a specific analytical boundary.

Investor Orientation is the second layer because it connects basic investing concepts to decision structure without turning the material into a recommendation.

| Orientation question | Concept path | How the concept helps |

|---|---|---|

| What is the investment meant to support? | Investment objectives | Objectives clarify the purpose of the decision before comparing possible investments. |

| How much uncertainty can the investor emotionally tolerate? | Risk tolerance | Risk tolerance helps explain discomfort with volatility, drawdowns, and uncertainty. |

| How much risk can the investor financially absorb? | Risk capacity | Risk capacity separates emotional comfort from financial ability to withstand loss or illiquidity. |

| Where is the investor’s analysis strongest? | circle of competence | Circle of competence keeps analysis closer to areas the investor can understand and monitor. |

Comparison Paths After the Foundations

Comparison topics become more useful after the underlying concepts are understood. Active versus passive investing, long-term versus short-term investing, lump sum versus dollar-cost averaging, and risk versus volatility can all create confusion if they appear before the basic terms are clear.

Use comparison paths to separate nearby ideas, not to skip the foundational concepts. Risk versus volatility is easier to understand after risk and return are clear. Lump sum versus dollar-cost averaging is easier to evaluate after compounding and time horizon are understood. Active versus passive investing is more meaningful after equity exposure, investor objectives, and the limits of prediction are clear.

What Investing Foundations Should Not Replace

Investing foundations are not a substitute for stock analysis, valuation, portfolio construction, or personal financial planning. They provide a cleaner starting map, but they do not determine which securities to own, how much to allocate, when to buy, or whether any investment is suitable.

The learning sequence should also stay separate from trading setups and short-term market timing. Equity Analysis Lab is focused on investor education, company analysis, valuation thinking, portfolio construction, and decision discipline, not buy or sell signals.

| Do not use investing foundations for | Use them for instead |

|---|---|

| Choosing individual stocks | Building the vocabulary needed before company analysis or valuation work. |

| Building a full portfolio | Understanding the basic concept layer before asset allocation, diversification, or position sizing. |

| Finding buy or sell signals | Separating investor education from trading execution or market timing. |

| Getting a personal recommendation | Clarifying the concepts that shape later decisions and questions. |

A Simple Learning Sequence

An investor who understands compounding but has not yet studied risk and return may still misread what long-term investing can and cannot do. A cleaner sequence moves from compounding into risk and return, then into time horizon, before comparing active versus passive approaches or lump sum versus dollar-cost averaging.

After that, investor orientation can add objectives, risk tolerance, risk capacity, and circle of competence. That order keeps early learning focused instead of mixing basic concepts with full portfolio or security-selection decisions.

FAQ

What should I learn first in investing foundations?

Start with compounding, risk and return, and time horizon. These concepts make later topics easier to understand because they explain growth, uncertainty, and decision context.

Is investing foundations the same as choosing investments?

No. Investing foundations organize the first concepts before investment selection. They do not decide which securities to own, how much to allocate, or whether an investment fits a specific investor.

Do investing concepts reduce risk?

No. Investing concepts can make risk easier to identify and discuss, but they do not remove uncertainty, prevent losses, or guarantee results.

Next Concepts to Study

Use the foundation sequence as an order of study: basic concepts first, investor orientation second, comparison paths after the foundations are clear.