Decision discipline in investing is the practice of keeping each investment decision tied to current evidence, risk limits, and portfolio fit instead of letting emotion, market noise, or a familiar thesis lower the evidence-review threshold. It does not remove uncertainty. It helps an investor avoid accepting supportive evidence too quickly, delaying contrary evidence, or treating confidence as a substitute for review.

Decision discipline means: the investor has a defined way to pause, check evidence, compare the decision with the portfolio plan, and decide whether the action still fits the facts available now.

It does not mean: ignoring new information, refusing to change a thesis, or staying with an investment simply because the original plan felt convincing.

Key points

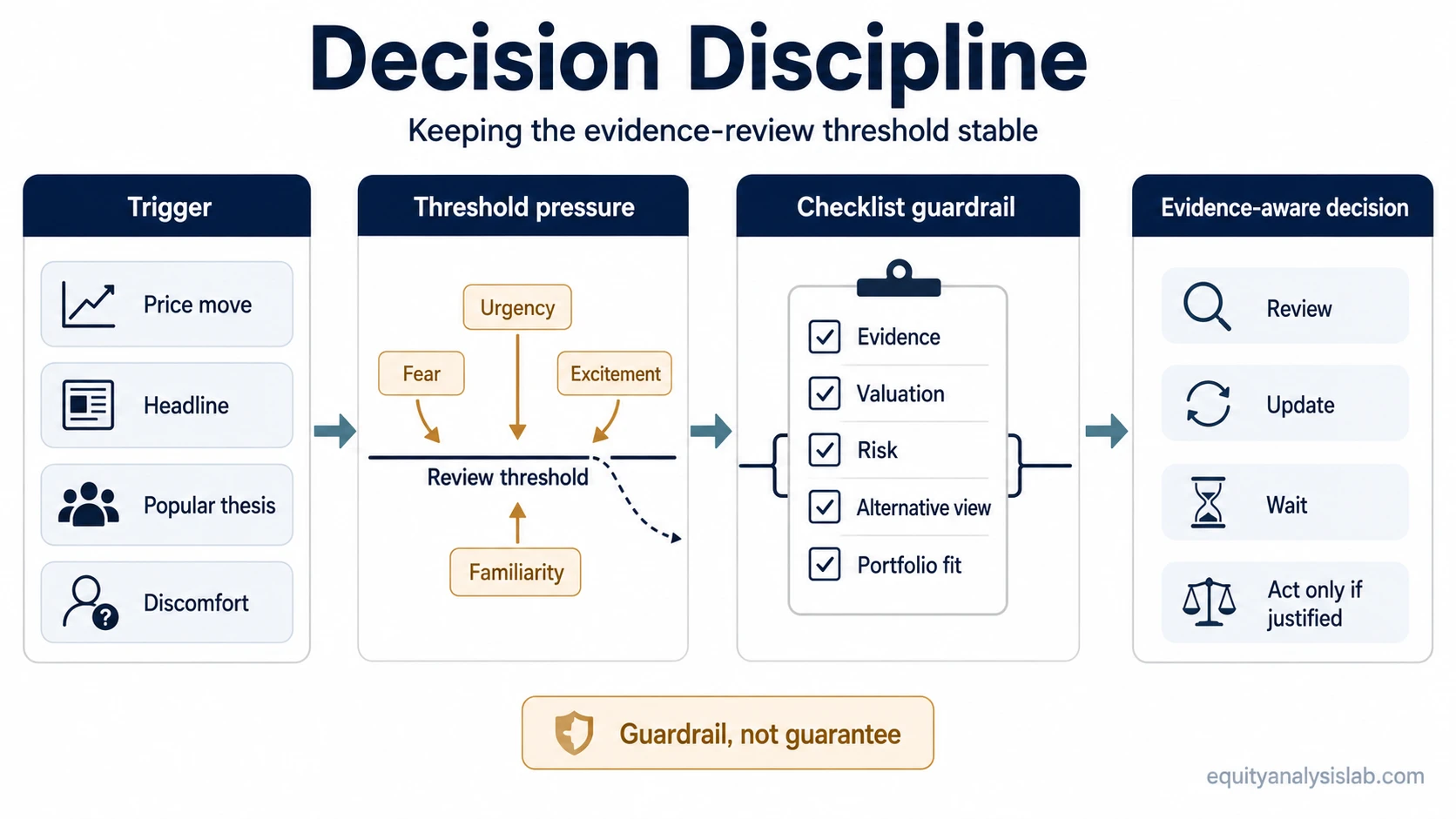

- Decision discipline protects the evidence-review threshold when price movement, fear, excitement, or narrative pressure makes action feel urgent.

- It separates the trigger for a decision from the evidence required to act on that trigger.

- It works best when the investor has written rules for business evidence, valuation, risk limits, position size, and portfolio fit.

- It can make impulsive action easier to catch before it becomes a portfolio decision, but it cannot guarantee better outcomes or remove market risk.

What decision discipline means in investing

In investing, decision discipline is less about willpower and more about process quality. A disciplined decision keeps three questions visible: what evidence has changed, what risk is being accepted, and how the action fits the portfolio.

Many investment decisions begin with a trigger rather than a complete review. A price drop, a strong earnings headline, a popular thesis, a market selloff, or a sudden gain can all create pressure to act before the evidence has been checked.

Decision discipline creates a pause between the trigger and the action. The pause is not meant to slow every decision unnecessarily. It is meant to prevent the investor from lowering the standard of proof simply because the decision feels emotionally easier, socially reinforced, or urgent.

The useful distinction is between discipline and stubbornness. Discipline keeps the review process consistent. Stubbornness protects the old conclusion even when the evidence has changed. A disciplined investor can hold, add, trim, wait, or change view, but the action must come from current evidence rather than from discomfort or attachment to the prior thesis.

Where investor decisions lose discipline

Investor decisions usually lose discipline before the final action happens. The problem often starts when the investor changes the evidence standard without noticing it.

| Decision pressure | How discipline weakens | What the investor should review |

|---|---|---|

| Panic after a price decline | The investor treats discomfort as evidence that the thesis has failed. | Business evidence, valuation change, balance-sheet risk, and original invalidation conditions. |

| Chasing after a strong move | The investor accepts a popular narrative without checking whether expected return has worsened. | Valuation, margin of safety, thesis durability, and position-size risk. |

| Familiar thesis or favorite company | Supportive evidence is accepted quickly while contrary evidence is softened or delayed. | Contrary evidence, base rates, changing competition, earnings quality, and capital allocation. |

| Market noise or headline pressure | The investor reacts to the latest information without separating signal from volatility. | Whether the information changes long-term business value, portfolio risk, or the original decision case. |

| Need to “do something” | Activity becomes a way to reduce anxiety rather than a response to new evidence. | The decision rule, the cost of action, the cost of waiting, and whether no action is a valid choice. |

The repeated pattern is not simply emotion. It is a change in review quality. Fear can make an investor demand too much certainty before holding a sound thesis. Excitement can make an investor demand too little evidence before buying into a crowded story. Familiarity can make contrary evidence feel less urgent than supportive evidence.

Decision trigger, evidence threshold, and checklist guardrail

A decision trigger is the event that makes the investor want to act. The evidence threshold is the amount and quality of review required before action is justified. A checklist guardrail keeps the threshold from moving just because the trigger feels emotionally strong.

| Trigger | Risk to decision discipline | Checklist guardrail |

|---|---|---|

| The stock falls sharply | The investor may confuse price pain with thesis failure. | Review whether business quality, earnings power, balance-sheet strength, and valuation assumptions changed. |

| The stock rises quickly | The investor may chase because waiting feels like missing out. | Check whether expected return still compensates for risk after the move. |

| A thesis becomes popular | The investor may treat consensus enthusiasm as confirmation. | List the strongest contrary evidence before increasing exposure. |

| A negative headline appears | The investor may react before identifying whether the issue is temporary or structural. | Separate short-term noise from evidence that changes cash flow, competitive position, or risk. |

| The investor wants a cleaner process | The checklist may become mechanical if it replaces judgment. | Use written rules as guardrails, not as a guarantee that every rule produces the right outcome. |

A useful checklist does not need to be complicated. It should force the investor to identify the decision, the evidence, the risk, the alternative interpretation, and the portfolio consequence. The value is not that the checklist predicts the future. The value is that it makes the investor show the reasoning before acting.

How decision discipline differs from related concepts

Decision discipline sets the decision-quality frame. Related investor-psychology concepts address different parts of the same problem, including emotional pressure, long-term process adherence, practical guardrails, and rule design.

| Concept | What it answers | Use it when the main problem is… |

|---|---|---|

| emotional investing | How fear, greed, regret, or excitement can shape investor behavior. | The decision is being pulled by emotion more than by evidence. |

| investment discipline | How an investor maintains a broader investment process over time. | The issue is portfolio process, plan adherence, review cadence, or long-term methodology. |

| how to avoid emotional investing | How to reduce emotion-driven mistakes with practical guardrails. | The investor needs a narrower support path for handling fear, excitement, or impulsive action. |

| rules-based investing | How written rules, checklists, and predefined conditions can support consistency. | The investor needs structure so decisions are not rebuilt from emotion each time. |

The distinction matters because decision discipline is the central control point for decision quality. Emotional investing explains the behavioral pull. Investment discipline explains broader process consistency. Rules-based investing explains how written conditions and checklists can reduce avoidable inconsistency.

A practical decision-discipline scenario

An investor owns a company after building a thesis around business quality, expected cash flow, valuation, and portfolio fit. The stock then falls after a disappointing headline. The immediate trigger is discomfort: the loss is visible, the news feels negative, and selling would reduce the emotional pressure.

A decision without discipline may treat the price decline itself as proof that the thesis failed. A disciplined review separates the trigger from the evidence. The investor checks whether the headline changes the company’s long-term economics, whether the valuation now reflects a different risk, whether the original thesis had an invalidation condition, and whether the position still fits the portfolio.

The same framework also works in the opposite direction. If a popular company rises quickly and the story becomes more exciting, decision discipline asks whether expected return has improved or whether the higher price has simply made the thesis feel socially safer. In both cases, the investor is not trying to predict the next move. The investor is trying to keep the evidence standard stable.

Limits of decision discipline

Decision discipline is a guardrail, not a guarantee. A disciplined process can still lead to a losing investment because uncertainty remains. The role of discipline is to make the decision more evidence-aware, not to remove risk.

It also does not mean staying invested regardless of new information. If business evidence, valuation, risk, or portfolio fit changes materially, discipline may require changing the decision. Holding a position only because the original thesis felt convincing is not discipline; it is attachment.

Decision discipline does not replace valuation, business analysis, earnings-quality review, risk limits, or portfolio construction. It organizes when and how those checks are used so the investor does not skip them under emotional pressure.

FAQ

Is decision discipline the same as investment discipline?

No. Decision discipline focuses on the quality of a specific decision: what evidence is reviewed, what risk is accepted, and whether the action fits the portfolio. Investment discipline is broader and covers the investor’s overall process, plan adherence, review cadence, and long-term methodology.

Does decision discipline mean never changing an investment thesis?

No. Decision discipline does not mean protecting the original thesis at all costs. If business evidence, valuation, risk, or portfolio fit changes materially, a disciplined investor may need to update the thesis or change the decision.

Can rules or checklists guarantee better investment results?

No. Rules and checklists can support a more consistent review process, but they cannot guarantee better investment results. Their role is to keep evidence, risk, and portfolio fit visible before action is taken.