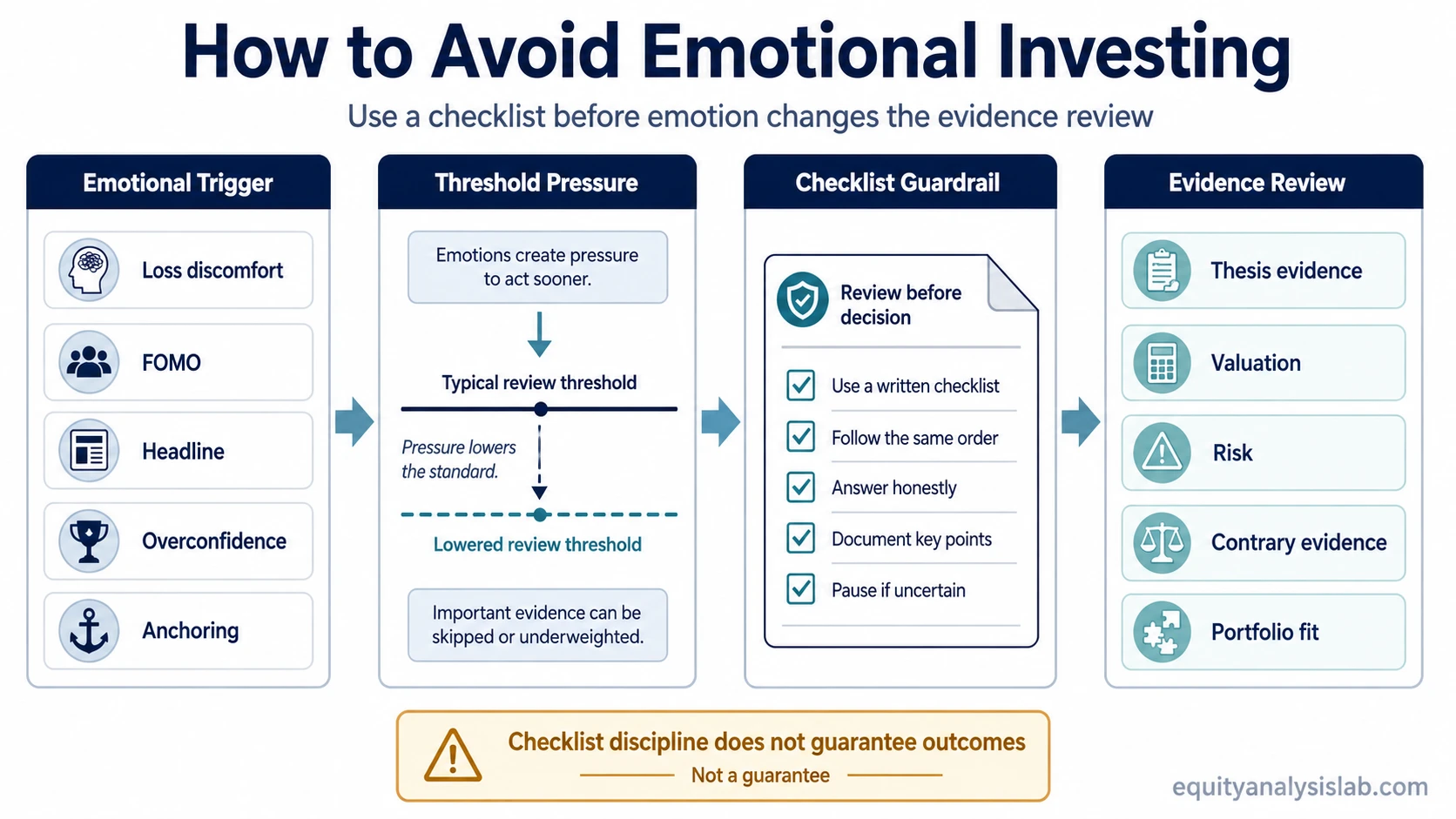

Avoiding emotional investing means slowing the decision before fear, FOMO, loss discomfort, headlines, or overconfidence changes how evidence is reviewed. The goal is not to remove emotion from investing. The goal is to stop emotion from replacing the checklist that reviews thesis evidence, valuation, risk, and portfolio fit.

Emotional investing becomes most dangerous when a feeling starts to act like evidence. A falling portfolio value can feel like proof that the thesis is broken. A fast rally can feel like proof that an investor must act immediately. A confident recent decision can make contrary information feel less important than it is.

Definition: Avoiding emotional investing is the process of reviewing investment evidence before emotion is allowed to change the decision. It is a review guardrail, not an attempt to become emotionless.

Key Points

- Emotional triggers are not automatically investment evidence.

- A written checklist slows the decision before the thesis is changed.

- The review separates business evidence, valuation, risk, time horizon, and portfolio fit.

- An urge to act is a warning sign when it appears before evidence review.

- A checklist can improve process discipline, but it cannot make outcomes certain.

Why Emotional Triggers Change Investment Decisions

An emotional trigger changes the decision process by making one piece of information feel larger than the rest. The trigger may be a visible loss, a sharp market rally, a dramatic headline, a missed opportunity, or a recent period of strong confidence. The risk is not the emotion itself. The risk is that the emotion lowers the amount of evidence required before action feels justified.

Loss discomfort can make an investor search for reasons to exit before reviewing whether the original business thesis changed. FOMO can make a rally feel urgent before valuation or risk is checked. Overconfidence can make supportive evidence feel obvious while contrary evidence is softened. Anchoring can keep attention fixed on a prior price rather than on current evidence.

The useful question is not “Do I feel calm?” The useful question is “Has the evidence changed enough to justify a decision?” That question keeps the review anchored in the investment process instead of the emotional trigger.

What Usually Gets Skipped

Emotional investing often appears as a skipped review step. The investor may still use rational language, but the sequence has changed: the action comes first, and the evidence is collected afterward to justify it.

| Review area | What emotion can skip | Why it matters |

|---|---|---|

| Business evidence | Whether revenue, margins, cash flow, balance sheet risk, or competitive position actually changed. | A price move alone does not prove that the underlying thesis is stronger or weaker. |

| Valuation | Whether the current price still makes sense relative to earnings quality, growth assumptions, and risk. | A good company can become less attractive if expectations rise faster than evidence. |

| Contrary evidence | Information that challenges the preferred action, such as weakening fundamentals or a better alternative interpretation. | Emotional pressure often accepts supportive evidence faster than contradictory evidence. |

| Risk | Whether the downside, concentration, liquidity, or thesis uncertainty is still acceptable. | Risk can feel smaller during excitement and larger during discomfort. |

| Portfolio fit | Whether the position still fits the investor’s time horizon, objectives, and overall exposure. | A decision can be emotionally satisfying while still weakening the portfolio process. |

The Checklist Guardrail

A checklist helps because it asks the investor to name the trigger before changing the decision. The point is not to make the checklist decide. The point is to make the investor review evidence before acting on pressure.

| Trigger | Evidence often skipped | Checklist failure | Action pressure | Review question |

|---|---|---|---|---|

| Sharp drawdown | Current thesis facts, valuation, and business quality. | Loss discomfort is treated as proof that the thesis failed. | Pressure to exit or reduce exposure before review. | What changed in the business evidence, valuation, risk, or portfolio fit? |

| Fast rally | Valuation discipline, downside risk, and alternative opportunities. | Price movement is treated as proof that immediate action is required. | Pressure to chase, add, or ignore position limits. | Does the evidence still support the expected-return logic after the price move? |

| Negative headline | Source quality, materiality, and whether the news changes long-term evidence. | The headline is treated as more important than the full evidence set. | Pressure to react before separating signal from noise. | Is this new information material to the thesis, or only emotionally salient? |

| Recent success | Contrary evidence, concentration risk, and limits of the original thesis. | Confidence replaces evidence review. | Pressure to increase size or lower standards. | Would this decision still pass the checklist without the recent positive outcome? |

| Anchoring to a prior price | Current fundamentals, updated assumptions, and opportunity cost. | The old price becomes the reference point instead of the current evidence. | Pressure to hold, add, or wait only because the prior price feels important. | Would the same decision make sense if the prior price were unknown? |

Common Mistakes That Make Emotional Investing Harder to Avoid

Treating discomfort as evidence: A loss can feel informative even when the underlying thesis has not been reviewed. Discomfort should trigger review, not replace it.

Chasing after a rally: A rising price can make urgency feel rational. The review still needs to ask whether valuation, risk, and expected-return logic changed.

Trying to time every reaction: Market movement can pressure the investor to constantly adjust. Frequent adjustment becomes a problem when it happens without a written reason.

Holding only because loss feels unacceptable: Avoiding a realized loss is not the same as confirming that the thesis remains intact.

Changing position size before reviewing evidence: Position-size pressure is a warning sign when it appears before the investor has checked the evidence that should govern the decision.

A Review Sequence Before Action

The review sequence should be short enough to use and specific enough to interrupt the emotional trigger. A long checklist that is ignored under pressure does not protect the process.

- Name the trigger. Write the reason the decision feels urgent: loss, rally, headline, missed opportunity, overconfidence, or anchoring.

- Separate price movement from thesis evidence. A price change may matter, but it should not be treated as the whole evidence set.

- Review the original thesis. Check whether the business evidence, valuation assumptions, risk factors, and expected-return logic still match the original case.

- Look for contrary evidence. Ask what would weaken the preferred action. This step is especially important when the decision feels obvious.

- Check portfolio fit. The checklist can also test whether the decision still fits the investor’s objectives, time horizon, risk capacity, and total exposure.

- Record the decision reason. The written reason should be clear enough that it can be reviewed later without relying on memory.

This kind of review is part of broader investment discipline. It does not make the investment outcome predictable. It makes the decision process easier to inspect.

How a Written Rule Can Help Without Becoming Mechanical

A written rule can prevent emotional pressure from becoming an immediate action. For example, an investor may require a thesis note update before changing a position after a large move. Another rule may require checking valuation, business evidence, and portfolio concentration before increasing exposure after a rally.

The rule should not be treated as a signal. It is a pause point. The decision still depends on evidence, uncertainty, and fit. A broader rules-based investing process can help when the rules define review conditions rather than automatic actions.

Illustrative Scenario

An investor owns a company after writing a thesis based on durable cash flow, manageable balance sheet risk, and a valuation that seemed reasonable under conservative assumptions. The stock then drops sharply after a negative market day. The portfolio loss feels immediate, and the investor feels pressure to act before reviewing the thesis.

A checklist changes the sequence. First, the investor names the trigger: the visible loss. Then the investor checks whether cash flow expectations, balance sheet risk, valuation assumptions, or portfolio concentration changed. If the evidence did not change, the discomfort is recorded as a trigger, not as a thesis update. If the evidence did change, the decision can be reviewed from the evidence rather than from the emotional reaction alone.

The scenario does not imply that holding, selling, or adding is correct. It shows the process difference between action first and review first.

When the Checklist Should Not Be Misused

A checklist is not proof that the original thesis is right. If business evidence, valuation, risk, or portfolio fit changes, the review needs enough flexibility to let the thesis change.

A checklist is not a personality test. The goal is not to label the investor as emotional or unemotional. The goal is to make the decision review visible.

A checklist is not a market timing tool. It does not predict the next price move. It helps separate current evidence from the pressure to act.

Where This Fits in the Investor Process

Avoiding emotional investing works best when the investor has a written thesis before the emotional moment arrives. Without a thesis, every price move can become the starting point for a new story. With a thesis, the review can ask whether the original evidence still holds.

The practical aim is evidence first, emotion second: the emotion can trigger review, but the recorded evidence should explain why the decision changed.

FAQ

Does avoiding emotional investing mean ignoring emotions?

No. It means recognizing the emotional trigger and then reviewing the evidence before changing the investment decision. Emotion can alert the investor to review, but it should not replace the review.

Can a checklist prevent bad investment outcomes?

No. A checklist can improve process discipline, but it cannot guarantee returns or prevent losses. Its role is to make the decision process more consistent and easier to review.

What is the first step when an investment decision feels urgent?

The first step is to name the trigger that is creating urgency. After that, the investor can check whether business evidence, valuation, risk, time horizon, or portfolio fit has changed.