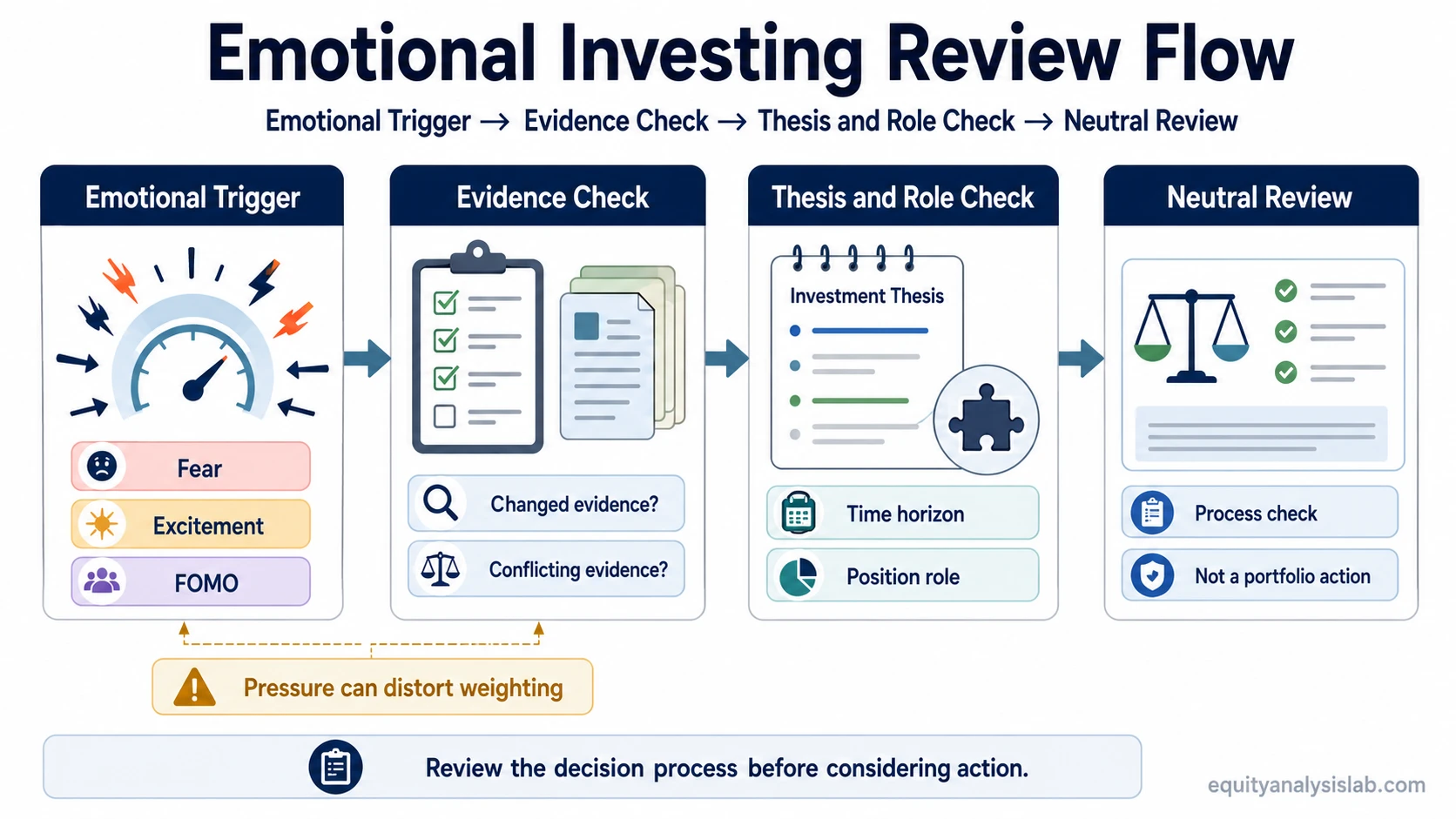

Emotional investing is a decision-review problem that appears when fear, excitement, FOMO, loss discomfort, or confidence pressure changes how an investor weighs evidence before making or revising an investment decision.

The issue is not that investors feel emotion. The risk appears when emotion starts to override the investment thesis, time horizon, position role, valuation context, risk limits, or checklist discipline that should frame the decision.

In fundamental investing, emotional investing can make a decision feel urgent before the underlying facts have changed. A falling price can make a sound thesis feel broken, a rising price can make weak evidence feel convincing, and social pressure can make another investor’s conviction feel like independent research.

Key Points About Emotional Investing

- Emotional investing is a decision-review problem, not the mere presence of emotion.

- The risk appears when urgency, fear, excitement, or FOMO changes evidence weighting.

- A neutral review compares the decision with thesis, time horizon, position role, valuation context, and checklist discipline.

- The emotional investing label does not prove the investor is wrong or that a portfolio action is required.

What Is Emotional Investing?

Emotional investing means allowing emotional pressure to influence an investment decision before the evidence has been reviewed neutrally. It can affect buying, selling, holding, averaging down, refusing to review a loss, or adding to a position after a sharp gain.

The concept belongs to investor psychology and decision discipline. It describes how judgment can shift when the investor reacts to market movement, regret, excitement, social comparison, or discomfort instead of checking whether the original evidence still supports the decision.

Definition: Emotional investing is an investment decision pattern where emotion changes evidence weighting, thesis review, time-horizon discipline, or position-role judgment before the investor completes a neutral review.

This makes emotional investing different from ordinary concern or conviction. Concern can be useful when it leads to evidence review. Conviction can be useful when it is grounded in research. The problem starts when the feeling becomes the decision filter.

How Emotional Investing Distorts Investor Decisions

Emotional investing often changes the sequence of review. Instead of starting with the thesis, business evidence, valuation context, time horizon, and portfolio role, the investor starts with the feeling and then searches for evidence that supports it.

That sequence can create selective attention. Negative information may look decisive after volatility. Positive information may look stronger after recent gains. A familiar position may receive more patience than a new idea with similar evidence. A popular idea may feel safer because many other investors are discussing it.

The distortion is usually observable in the decision process. The investor may stop asking whether the facts changed and instead ask how to relieve pressure, avoid regret, preserve pride, or keep up with other investors.

Observable Signs of Emotional Investing

Emotional investing is easier to review when it is treated as observable behavior rather than a personality label. The question is not “Am I emotional?” The better question is “What changed in the evidence review after the emotion appeared?”

| Observable sign | What it can indicate | Neutral review check |

|---|---|---|

| The decision becomes urgent after price movement | Recent volatility may be controlling the review sequence | Check whether the thesis changed or only the emotional pressure changed |

| Evidence is accepted only when it supports the desired action | The investor may be using evidence to defend a feeling | List confirming and conflicting evidence before deciding |

| The position role is forgotten | A small satellite idea may be treated like a core holding, or the reverse | Recheck allocation role, concentration, and downside tolerance |

| The time horizon suddenly changes | Short-term pressure may be replacing the original holding period | Compare the decision with the time horizon used when the thesis was formed |

| Other investors’ confidence becomes the main input | Social proof may be replacing independent analysis | Ask whether the decision still stands without outside enthusiasm or fear |

How to Separate the Trigger from the Decision

A useful emotional investing review separates the trigger from the decision. The trigger explains why pressure appeared. The evidence check determines whether the investment case actually changed.

| Trigger | Decision distortion | Evidence check | Review question |

|---|---|---|---|

| Fear after volatility | Recent downside receives too much weight | Recheck thesis quality, risk capacity, and time horizon | Has the evidence changed, or only the emotional pressure? |

| Excitement after gains | Recent strength is treated as stronger proof than it is | Recheck valuation, position role, and concentration | Is the decision supported beyond recent price movement? |

| FOMO from other investors | Outside conviction replaces independent research | Recheck the investor’s own evidence record | Would the decision still make sense without social pressure? |

| Loss discomfort | The investor avoids review or exits too quickly | Recheck the original plan and downside scenario | Is the action reducing risk or avoiding discomfort? |

Common Emotional Investing Mistakes

One common mistake is treating a strong feeling as new information. A feeling may identify pressure, but it does not by itself update revenue quality, margins, cash flow, valuation, competitive position, or portfolio role.

Another mistake is changing the decision standard after the outcome becomes uncomfortable. An investor may demand perfect evidence from a losing position while accepting thin evidence for a winning position, even when both require the same level of review.

A third mistake is using recent price movement as a substitute for thesis review. Price movement can create a reason to recheck the case, but it does not automatically prove that the business quality, valuation setup, or risk profile has changed.

Common mistake: The investor tries to remove discomfort before separating the emotional trigger from the investment evidence. That can turn a review process into a pressure-release decision.

Emotional Investing vs Investment Discipline

Emotional investing is one behavioral pressure inside the broader decision process. Investment discipline is the broader ability to follow a defined process across thesis review, position sizing, time horizon, risk limits, and portfolio rules.

| Concept | Main role | What it reviews |

|---|---|---|

| Emotional investing | Identifies when emotion may be distorting a decision | Trigger, evidence weighting, urgency, thesis pressure, and review quality |

| Investment discipline | Maintains process consistency across decisions | Rules, checklist use, allocation boundaries, holding period, and review routines |

The distinction matters because identifying emotion does not complete the investment process. It only signals that the decision should be checked against the same evidence standard that would apply without the emotional pressure.

How to Review an Emotional Investing Decision

A neutral review starts by slowing the decision down enough to separate the feeling from the evidence. The goal is not to suppress emotion. The goal is to prevent emotion from becoming the only filter used to interpret the facts.

Review sequence:

- Name the trigger: volatility, gain, loss, social pressure, regret, confidence, or uncertainty.

- Restate the original thesis in one or two sentences.

- List the evidence that has changed and the evidence that has not changed.

- Check whether the time horizon and position role are still the same.

- Compare the proposed action with checklist discipline before deciding.

Detailed prevention routines belong on How to Avoid Emotional Investing. The useful split is simple: emotional investing identifies the distortion, while prevention routines focus on guardrails that reduce the chance of repeating it.

A Short Emotional Investing Example

An investor owns a company after building a thesis around earnings durability, balance-sheet strength, and a multi-year time horizon. The stock falls sharply after a broad market selloff, but the investor has not yet reviewed whether the company’s fundamentals changed.

If the investor sells only because the price drop feels intolerable, emotional pressure may be driving the decision. If the investor rechecks the thesis, valuation, risk limits, and time horizon before acting, the same concern can become a disciplined review rather than an emotional reaction.

The same logic applies after gains. A rising price may create excitement, but the decision to add still needs evidence beyond recent strength, especially if the position is already large or valuation has become less favorable.

Limits of the Emotional Investing Label

Calling a decision emotional does not prove that the decision is wrong. A fearful investor may still identify a real thesis break. An excited investor may still recognize improving evidence. The label only means the decision process needs to be checked for distortion.

Limitation: Emotional investing review cannot determine suitability, expected return, portfolio allocation, or the correct action by itself. It only helps separate emotional pressure from evidence, thesis, time horizon, and checklist discipline.

This boundary is important because investor psychology concepts can become misleading when they are treated as signals. Emotional investing is not a buy signal, sell signal, or proof that a position is valid or invalid.

Related Concepts

Emotional investing connects most directly to decision discipline because both concepts deal with process quality under pressure. It also connects to prevention routines, but prevention is a separate question from defining the distortion itself.

- Emotional investing: identifies how emotion can distort evidence weighting, thesis review, and decision timing.

- Prevention routines: focus on guardrails that reduce repeated emotional decision drift.

- Investment discipline: covers broader process adherence across thesis review, allocation boundaries, holding period, and portfolio rules.

FAQ

What is emotional investing?

Emotional investing is a decision pattern where fear, excitement, FOMO, loss discomfort, or confidence pressure changes how an investor weighs evidence before completing a neutral review.

Is emotional investing always irrational?

No. Emotion can point to a real concern or a real opportunity. The risk appears when the emotion replaces evidence review instead of prompting it.

How does emotional investing affect investor decisions?

It can change evidence weighting, shorten the investor’s time horizon, distort position-role judgment, or make recent price movement feel more important than the original thesis.

What is an example of emotional investing?

An investor may sell after volatility without checking whether the thesis changed, or add after gains because the position feels exciting rather than because the evidence improved.

Does identifying emotional investing tell an investor what to do?

No. It only signals that the decision should be reviewed against thesis, evidence, time horizon, position role, and checklist discipline before any action is considered.