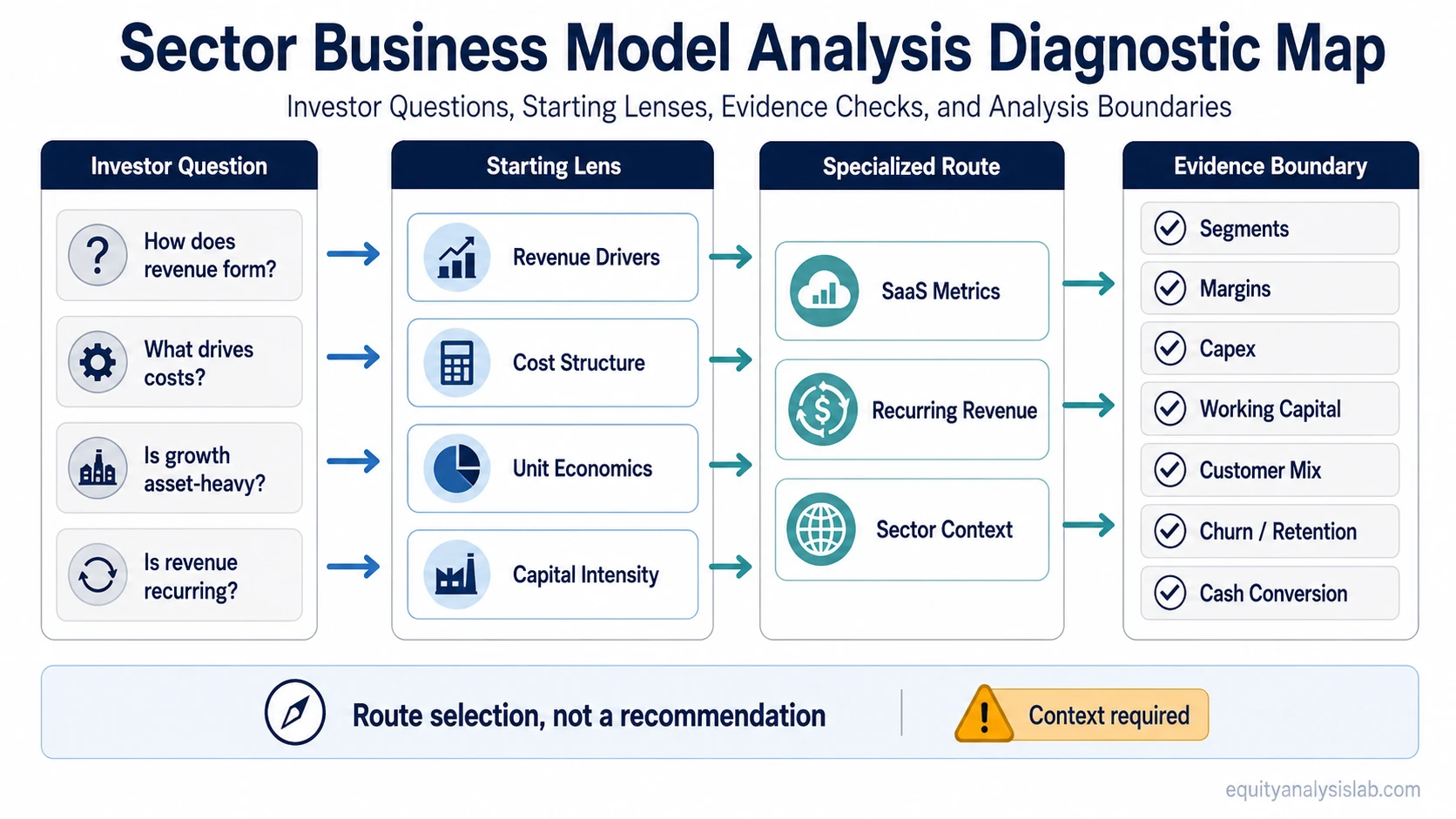

Sector business model analysis helps investors choose the right business-model lens before going deeper into company or sector research. The useful starting point depends on the question: revenue drivers, cost structure, unit economics, customer concentration, capital intensity, recurring revenue, or sector economics.

Key Points

- Start with the business-model question before choosing the metric.

- Use sector context before judging margins, capital needs, or cash conversion.

- SaaS and recurring-revenue models need their own measurement route.

- No business model is automatically superior without evidence from filings, financial statements, and operating data.

How to Choose the Right Business Model Lens

The first step is not to label a company as “good” or “bad.” The first step is to decide which part of the business model explains how the company earns revenue, absorbs costs, converts activity into cash, and depends on customers, assets, or recurring contracts.

| Investor question | Best starting route | Evidence to check | Why it matters |

|---|---|---|---|

| How does the company create revenue? | Business Model Features | Revenue segments, volume drivers, pricing, contract type, customer mix | The revenue model shapes how growth appears and how fragile that growth may be. |

| Does the company need heavy assets to grow? | Capital intensity and asset structure | Property, equipment, depreciation, capex, lease obligations, working capital | Capital needs affect reinvestment burden, margin durability, and free cash flow conversion. |

| Are margins driven by scale, pricing, or cost control? | Cost structure and unit economics | Gross margin, operating margin, contribution margin, customer acquisition cost, fulfillment cost | Margins can look similar across companies while being produced by very different business economics. |

| Is recurring revenue central to the model? | SaaS Metrics | ARR, MRR, churn, retention, expansion revenue, CAC, LTV | Recurring revenue needs retention and customer-quality checks, not only headline growth. |

| Does industry structure change the interpretation? | Sector Analysis | Sector cyclicality, regulation, input costs, demand sensitivity, balance-sheet norms | The same metric can mean different things in software, industrials, financials, utilities, or commodity-linked businesses. |

Useful observable evidence usually comes from segment revenue, gross and operating margin structure, capex, working capital, customer concentration, churn or retention data where relevant, and sector-specific disclosure. The route matters because each evidence type answers a different business-model question.

Business Model Feature Routes

Business model features describe the structural traits that shape how a company operates. They help separate questions about asset needs, scale, pricing power, customer dependency, and operating leverage.

An asset-light business model may require less fixed investment than an asset-heavy model, but that does not automatically make it better. Investors still need to check customer concentration, pricing durability, reinvestment needs, and whether reported margins convert into cash.

Capital intensity is the opposite side of the same routing problem. A capital-intensive company may need recurring reinvestment to maintain capacity, comply with regulation, or support growth. That can make depreciation, maintenance capex, asset turnover, and free cash flow conversion more important than headline revenue growth.

Economies of scale, pricing power, and unit economics belong in the same review because they explain how growth flows through the income statement. A company can grow revenue while still failing to improve economics if customer acquisition costs, support costs, input costs, or fulfillment costs rise at the same time.

Customer concentration adds a different risk layer. When a small group of customers controls a large share of revenue, the business model may depend less on broad market demand and more on contract renewal, bargaining power, and customer-specific budget cycles.

SaaS and Recurring-Revenue Metric Routes

Subscription and recurring-revenue businesses need a separate measurement route because revenue recognition, customer retention, expansion revenue, and acquisition costs can change the interpretation of growth.

Annual recurring revenue is useful when a company has subscription contracts or repeatable revenue streams, but ARR alone does not prove quality. It needs to be read with churn, net retention, customer acquisition cost, contract duration, expansion revenue, and cash collection.

MRR can be useful for shorter measurement periods, while churn and retention show whether the customer base is stable. CAC and LTV help connect growth spending to customer economics, although those measures can become misleading if definitions are inconsistent or if payback periods stretch too far.

The recurring-revenue route is most useful when the investor is trying to separate durable contracted revenue from growth that depends on constant new customer acquisition. That distinction matters because a business can report strong growth while the underlying customer base is still unstable.

Sector Analysis Routes

Sector context changes how business model evidence should be read. A margin level that looks strong in one sector may be normal in another, and a high capital requirement may be structural rather than a sign of poor management.

For cyclical sectors, the first route is usually demand sensitivity. Revenue, margins, inventory, receivables, and working capital may all respond differently as the cycle changes. That makes peak-margin risk and cash conversion more important than a single-year profitability snapshot.

For defensive sectors and some regulated industries, the review often moves toward pricing rules, allowed returns where relevant, balance-sheet structure, and capital requirements. A stable revenue base can still carry reinvestment needs, regulatory limits, or financing risk.

For software and digital subscription businesses, sector analysis overlaps with recurring-revenue metrics. For industrial or asset-heavy businesses, it overlaps with capital intensity, asset turnover, and maintenance capex. For financial companies, it may require a different balance-sheet lens because revenue, leverage, and capital rules behave differently from operating companies.

Illustrative Route Example

A capital-intensive industrial company, a subscription software company, and a regulated financial company can all report revenue growth, but the starting analysis lens should not be the same.

For the industrial company, the review may begin with capital intensity, capacity, input costs, working capital, and cash conversion. For the software company, the review may begin with recurring revenue, retention, churn, customer acquisition cost, and expansion revenue. For the financial company, the review may begin with balance-sheet structure, regulatory capital, credit quality, and interest-rate sensitivity.

The useful takeaway is that each model changes the first evidence check before valuation or portfolio relevance can be judged.

What Sector Business Model Analysis Cannot Decide

Sector business model analysis does not predict returns, create a buy or sell decision, or prove that a company deserves a specific valuation. It only helps organize the evidence that should be checked before moving into deeper company analysis.

A recurring-revenue model is not automatically superior to a transactional model. An asset-light model is not automatically superior to an asset-heavy model. A high-margin company is not automatically higher quality if those margins depend on weak reinvestment, customer concentration, underreported costs, or temporary sector conditions.

The analysis also cannot replace primary evidence. Filings, segment disclosures, financial statements, management commentary, customer concentration notes, and sector-specific data still matter. The route map helps decide where to look first, not what conclusion to reach.

FAQ

What is sector business model analysis?

Sector business model analysis is the process of choosing the right business-model lens for a company or industry before deeper research. It looks at revenue drivers, cost structure, unit economics, capital intensity, customer concentration, recurring revenue, and sector context.

Is sector business model analysis the same as sector analysis?

No. Sector analysis studies industry structure, cyclicality, regulation, demand patterns, and competitive context. Sector business model analysis uses that context to decide which business-model traits and metrics matter most for a company inside the sector.

Why do SaaS companies need a separate metric route?

SaaS and recurring-revenue companies often depend on retention, churn, ARR, MRR, CAC, LTV, and expansion revenue. These measures can reveal whether growth is durable or whether the company must spend heavily to replace lost customers.

Can business model analysis identify the best stock to buy?

No. It can help investors organize company evidence, but it does not create a buy decision, predict performance, or prove valuation quality. Investment decisions require broader analysis, risk assessment, valuation work, and portfolio context.