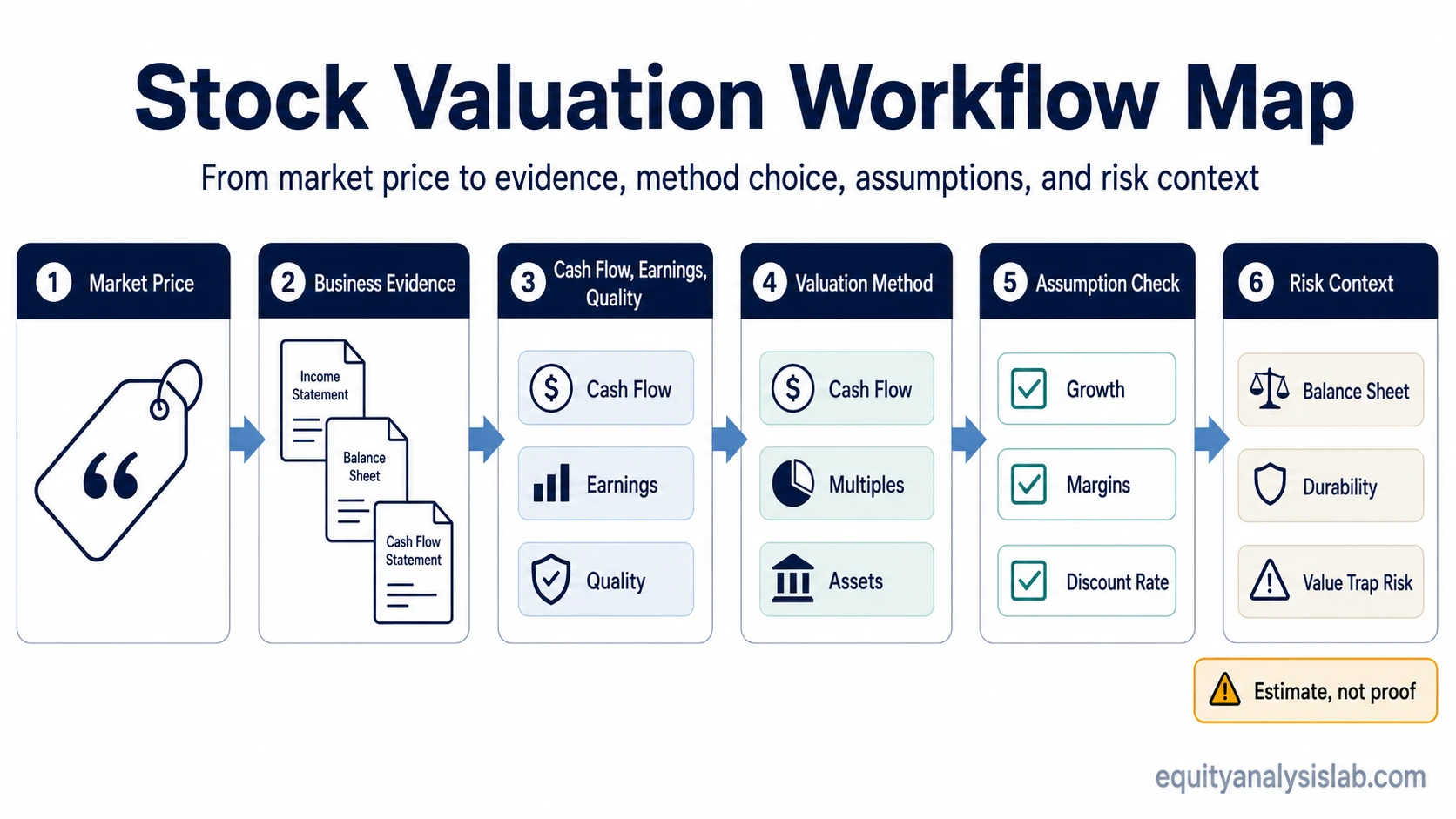

To value a stock, compare its market price with an estimate of the underlying business value using financial statements, cash flow, earnings, growth, business quality, risk, and valuation methods.

That estimate is not a certainty. A valuation is a structured judgment about what the business may be worth under reasonable assumptions, while the market price is the observable amount investors are currently paying.

For beginners, the useful starting point is not choosing one perfect formula. It is learning which evidence belongs to which valuation question, then avoiding the mistake of treating a cheap-looking number as a complete investment conclusion.

Key Points

- Price is what the market quotes; value is an estimate built from evidence and assumptions.

- No single ratio can value a stock by itself.

- The right valuation method depends on the question being asked.

- Cash flow, earnings quality, growth, balance-sheet risk, and business durability can change the meaning of a valuation number.

- A low price or low multiple can still be a value trap if the business is deteriorating.

What It Means to Value a Stock

Valuing a stock means estimating what a share of a business may be worth and comparing that estimate with the current market price. The estimate can come from cash flows, earnings, assets, peer comparisons, or a combination of methods.

The market price is visible every trading day. The business value is not directly visible. It has to be inferred from the company’s economics: how much cash the business can produce, how durable those cash flows appear, how much capital the business needs, how risky the balance sheet is, and how much uncertainty sits in the assumptions.

A beginner mistake is to treat valuation as a single calculation. A stronger approach separates three jobs: gather business evidence, choose a valuation method, then test whether the result still makes sense after risk and quality are considered.

Price, Value, and Intrinsic Value

Price and value are related, but they are not the same thing. Price is the amount available in the market. Value is an estimate of what the business is worth based on evidence such as cash generation, reinvestment needs, growth, risk, and competitive position.

Intrinsic value is one way to describe that estimate. It usually refers to the value of the business based on its expected future economics rather than the latest quoted price alone.

Two investors can reach different valuation estimates for the same company because they may use different growth assumptions, margin assumptions, discount rates, peer groups, or risk adjustments. That difference does not automatically make one estimate useless. It shows why valuation needs ranges, sensitivity checks, and humility.

Which Valuation Method Fits the Question?

A valuation method is useful only when it matches the question. Some questions are about cash generation, some are about estimated business value, and some are about how the market is pricing the company compared with similar businesses.

| Valuation question | Better starting point | What can distort the answer | Concept to review |

|---|---|---|---|

| Is the business producing real cash? | Check cash generated after operating needs and reinvestment. | Cash flow can be uneven across cycles, acquisition periods, and heavy investment phases. | free cash flow |

| What might the business be worth? | Estimate a business-value range rather than relying only on the quoted price. | Growth, margin, reinvestment, and discount-rate assumptions can change the estimate materially. | intrinsic value |

| What are future cash flows worth today? | Use a cash-flow model only when the assumptions can be stated and tested. | Small changes in long-term growth, margins, or discount rate can create a very different output. | discounted cash flow method |

| How does the company compare with peers? | Compare valuation multiples only against genuinely similar businesses. | Peer groups can mislead when growth, margins, capital needs, accounting quality, or risk differ. | relative valuation |

| How much are investors paying for earnings? | Use earnings multiples as a starting comparison, not a complete conclusion. | Earnings can be cyclical, adjusted, temporarily inflated, or weakly supported by cash flow. | how much investors are paying for earnings |

Why Ratios Can Mislead Beginners

Valuation ratios are useful shortcuts, but shortcuts can hide the reason a stock looks cheap or expensive. A low multiple may reflect undervaluation, but it may also reflect falling earnings quality, weak growth, debt pressure, cyclicality, competitive decline, or market concern about future results.

A high multiple is not automatically wrong either. A durable business with stronger growth, better margins, lower capital needs, and lower balance-sheet risk may trade at a higher valuation than a weaker business. The number alone does not explain whether the premium is justified.

Limitation: Ratios work best as comparison tools, not final answers. They should be checked against sector norms, business model differences, accounting quality, balance-sheet risk, growth durability, and cash-flow support.

How Cash Flow and Business Quality Affect Valuation

Cash flow matters because valuation is ultimately tied to the economic benefits a business can produce for owners over time. Earnings may be useful, but they can be affected by accounting choices, one-time items, cyclicality, and non-cash adjustments.

Business quality affects how much confidence an investor can place in a valuation estimate. A company with recurring demand, pricing power, disciplined capital allocation, and manageable debt may deserve a different valuation discussion from a company with unstable margins or heavy financing risk.

That does not mean quality guarantees a good outcome. It means that the same valuation multiple can mean different things depending on the durability of the business behind the number.

Common Beginner Mistakes When Valuing Stocks

Beginners often search for one number that settles the decision. Valuation rarely works that cleanly. The goal is to improve the quality of the estimate and understand what could make the estimate wrong.

- Treating low P/E as automatically cheap: a low multiple can reflect real risk, not only opportunity.

- Treating a DCF output as precise: the model can look exact even when the assumptions are uncertain.

- Ignoring cash flow: reported earnings are less useful if they are not supported by cash generation over time.

- Ignoring business quality: weak competitive position, fragile margins, or poor capital allocation can reduce valuation confidence.

- Confusing valuation with a decision: valuation is one part of the research process, not a complete buy or sell instruction.

A Simple Beginner Valuation Sequence

A clean starting sequence begins with evidence. First, identify earnings and cash conversion. Second, check balance-sheet pressure and reinvestment needs. Third, choose the valuation method that fits the available evidence. Fourth, test the assumptions against business quality, cyclicality, and margin durability. Fifth, treat valuation as research input, not a standalone decision.

A company can look inexpensive on earnings while free cash flow weakens, debt rises, or margins depend on unusually favorable conditions. In that case, the low multiple may reflect real business risk rather than a clear bargain. Another company can look expensive on a simple multiple, yet still deserve deeper analysis if cash conversion is durable, reinvestment opportunities are strong, and the assumptions can be tested rather than simply believed.

Valuation also does not replace portfolio context, risk tolerance, position size, or diversification. A stronger estimate can improve research quality, but it cannot remove uncertainty from the investment process.

Stock Valuation Concepts to Learn Next

After the basic price-versus-value distinction is clear, the next step is to separate the valuation problem into smaller concepts. Cash-flow evidence helps test the quality of the numbers. Intrinsic-value thinking frames the business-value estimate. DCF and relative valuation offer different method families. Earnings multiples show how the market is pricing profit, but they still need context.

Start with cash: check whether the business can produce cash after operating needs and reinvestment.

Then estimate value: compare the current price with a reasoned business-value range instead of relying on one quoted number.

Choose the method carefully: use cash-flow methods when assumptions can be made responsibly and peer comparisons when comparable businesses are genuinely similar.

Keep the mistake boundary visible: a valuation estimate can support research, but it does not replace risk analysis, business analysis, or portfolio judgment.

FAQ

Is a low P/E ratio enough to show that a stock is undervalued?

No. A low P/E ratio can point to a potentially cheap stock, but it can also reflect weak growth, cyclical earnings, accounting risk, debt pressure, or a deteriorating business.

Is DCF the best way to value every stock?

No. DCF can be useful when future cash-flow assumptions are reasonable, but it is sensitive to inputs. Some situations also require peer comparisons, asset-based context, or extra caution around uncertain cash flows.

What is the difference between price and value?

Price is the amount quoted in the market. Value is an estimate of what the business may be worth based on evidence and assumptions. The two can differ, but the difference alone does not prove an investment case.