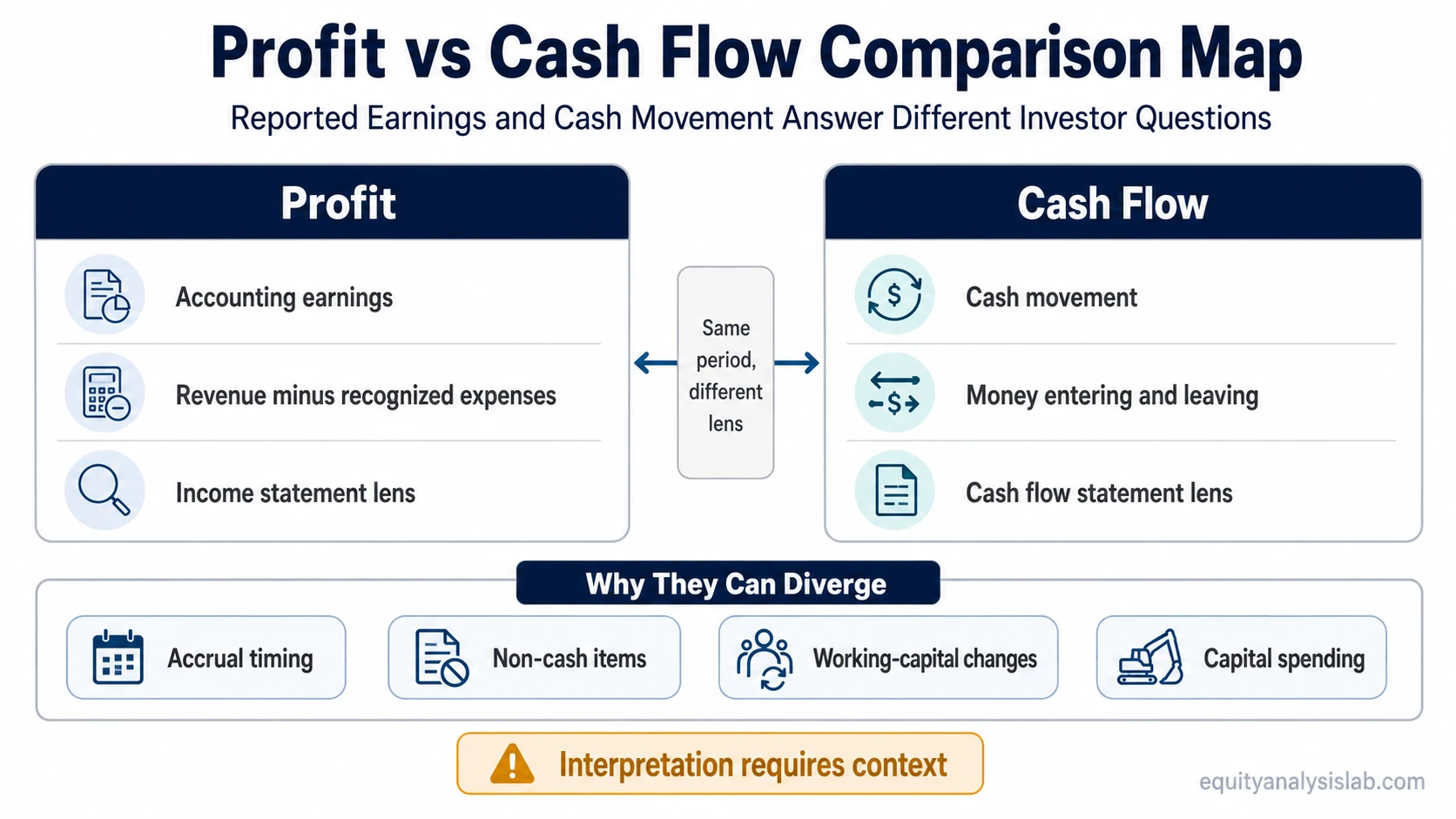

Profit vs cash flow separates accounting earnings from actual cash movement. Profit shows what remains after revenue and expenses are recognized under accounting rules, while cash flow shows how much cash entered or left the business during the same period.

A company can report a profit and still consume cash. It can also generate cash in a period without proving that its profitability is durable. The useful distinction is not which number is always better. The useful distinction is which question each number answers.

Key Points

- Profit reports accounting earnings after recognized expenses.

- Cash flow tracks cash entering and leaving the business.

- The two can diverge because of accrual accounting, non-cash items, working-capital timing, and capital spending.

What Profit Measures

Profit measures earnings after a company recognizes revenue and subtracts expenses for a reporting period. For public companies, the main evidence usually comes from the income statement, where revenue, cost of revenue, operating expenses, interest, taxes, and net income are presented.

Profit is useful because it shows whether the company’s accounting earnings exceed its recognized costs. It can also connect to profitability measures such as net margin, which compares net income with revenue. That does not mean profit alone proves business quality. The timing and quality of the earnings still matter.

Short definition: Profit is accounting earnings left after recognized expenses are deducted from recognized revenue.

What Cash Flow Measures

Cash flow measures actual cash movement. It shows whether money came into or left the business during the period, regardless of whether all related revenue and expenses were recognized in the same way on the income statement.

The primary evidence comes from the cash flow statement, which separates operating, investing, and financing cash flows. For investor analysis, operating cash flow is often the first cash-generation check because it connects the company’s core business activity to cash movement.

Short definition: Cash flow is the movement of cash into and out of a business during a reporting period.

Profit vs Cash Flow Comparison

The difference between profit and cash flow becomes clearer when each metric is tied to the question it answers, the statement where it appears, and the accounting mechanics that can affect it.

| Comparison point | Profit | Cash flow |

|---|---|---|

| Main question answered | Did recognized revenue exceed recognized expenses? | Did the business generate or consume cash? |

| Main statement source | Income statement | Cash flow statement |

| Accounting basis | Accrual accounting | Cash movement and statement adjustments |

| Common distortion | Revenue timing, expense recognition, non-cash charges, one-time items | Working-capital swings, capital spending, financing flows, timing effects |

| Investor-use caveat | Profit can look strong before cash is collected. | Cash can look strong for temporary reasons that do not prove durable profitability. |

Why Profit and Cash Flow Can Diverge

Profit and cash flow diverge because accounting earnings and cash movement follow different measurement rules. Accrual accounting can recognize revenue before cash is collected or expenses before cash is paid. That timing gap can make reported profit look different from cash generation in the same period.

Non-cash expenses also create a gap. Depreciation and amortization reduce accounting profit, but they do not require a new cash payment in the period they are recorded. Stock-based compensation, impairment charges, and certain accounting adjustments can also separate net income from cash movement.

Working capital adds another layer. If customers owe more money, inventory rises, or suppliers are paid faster, cash can fall even while profit remains positive. If receivables are collected or payables rise, operating cash flow can improve even when reported profit is not especially strong.

Capital spending can create an additional distinction. A company may generate operating cash but still have less cash available after maintaining factories, software infrastructure, equipment, or stores. That is why investors often move from raw cash generation to cash after capital spending when they analyze cash left after reinvestment.

Illustrative Same-Company Example

Illustrative scenario: A public company reports $100 million of revenue, $85 million of recognized expenses, and $15 million of profit for the quarter. On the surface, the company looks profitable because its income statement shows earnings after expenses.

The cash picture can still be weaker. Suppose a large portion of the revenue was sold on credit, inventory increased ahead of future demand, and customers had not yet paid by quarter-end. The company can report positive profit while operating cash flow is flat or negative because cash has not yet arrived.

The reverse can also happen. The company might collect old receivables, delay supplier payments, or reduce inventory, creating strong cash flow in one quarter. That does not automatically prove durable profitability if margins are shrinking or recurring earnings remain weak.

The useful read is the gap between the two numbers. Profit shows the earnings result, while cash flow tests whether those earnings are turning into cash during the same period.

Which Question Each Metric Answers

Neither profit nor cash flow is automatically more important in every situation. Profit answers whether the company produced accounting earnings during the period. Cash flow answers whether the business generated cash during the period.

Profit can matter more when the question is margin structure, expense control, tax impact, or earnings power. Cash flow can matter more when the question is liquidity, reinvestment capacity, debt pressure, or whether reported earnings are being converted into cash.

For investor analysis, the stronger reading usually comes from comparing both. A profitable company with weak cash conversion may require closer review. A cash-flow-positive company with poor recurring profitability may also require caution. The numbers are complementary, not interchangeable.

Common Confusion Trap

Profitability is not the same as liquidity. A company can be profitable on the income statement and still face cash pressure if collections lag, inventory absorbs cash, or capital spending is high.

Cash generation is not the same as durable profitability. A temporary cash inflow from working-capital release, asset sales, financing activity, or delayed payments can improve cash flow without proving that the operating model is earning attractive recurring profits.

Neither metric alone proves financial strength, business quality, investment attractiveness, or future returns. The interpretation depends on the reporting period, statement location, recurring versus temporary drivers, and cross-statement confirmation.

How Investors Can Read the Difference

A useful starting sequence is to compare the income statement with the cash flow statement over the same period. If net income rises while operating cash flow weakens, the next checks are usually receivables, inventory, payables, non-cash charges, and one-time items.

If operating cash flow is strong while profit is weak, the next checks are also important. Cash may be supported by working-capital release, delayed payments, lower inventory, restructuring effects, or non-recurring inflows. Strong cash flow is more meaningful when it is repeatable and connected to the core business.

The safest interpretation treats profit and cash flow as a pair. Profit gives an earnings view. Cash flow gives a cash movement view. The gap between them often carries the most useful information.

Related Concepts

Income-statement profit and cash-flow evidence work best when read together. The income statement shows recognized earnings, while the cash flow statement tests cash movement behind those earnings.

Margin analysis helps explain how much profit remains from revenue. Free cash flow analysis goes one step further by asking how much cash remains after capital spending and reinvestment needs.

FAQ

Can a company be profitable but cash-flow negative?

Yes. A company can report profit while cash flow is negative if revenue is recognized before cash is collected, inventory absorbs cash, capital spending is high, or working-capital timing moves against the business.

Can a company be cash-flow positive but not profitable?

Yes. Cash flow can be positive even when profit is weak or negative, especially if the company collects old receivables, reduces inventory, delays payments, sells assets, or receives financing inflows.

Is cash flow the same as profit and loss?

No. Profit and loss is an income-statement view of revenue and expenses. Cash flow is a cash-movement view that tracks money entering and leaving the business during the period.

Why do investors compare profit and cash flow?

Investors compare them because the gap can reveal timing effects, non-cash accounting items, working-capital pressure, or weak cash conversion behind reported earnings.