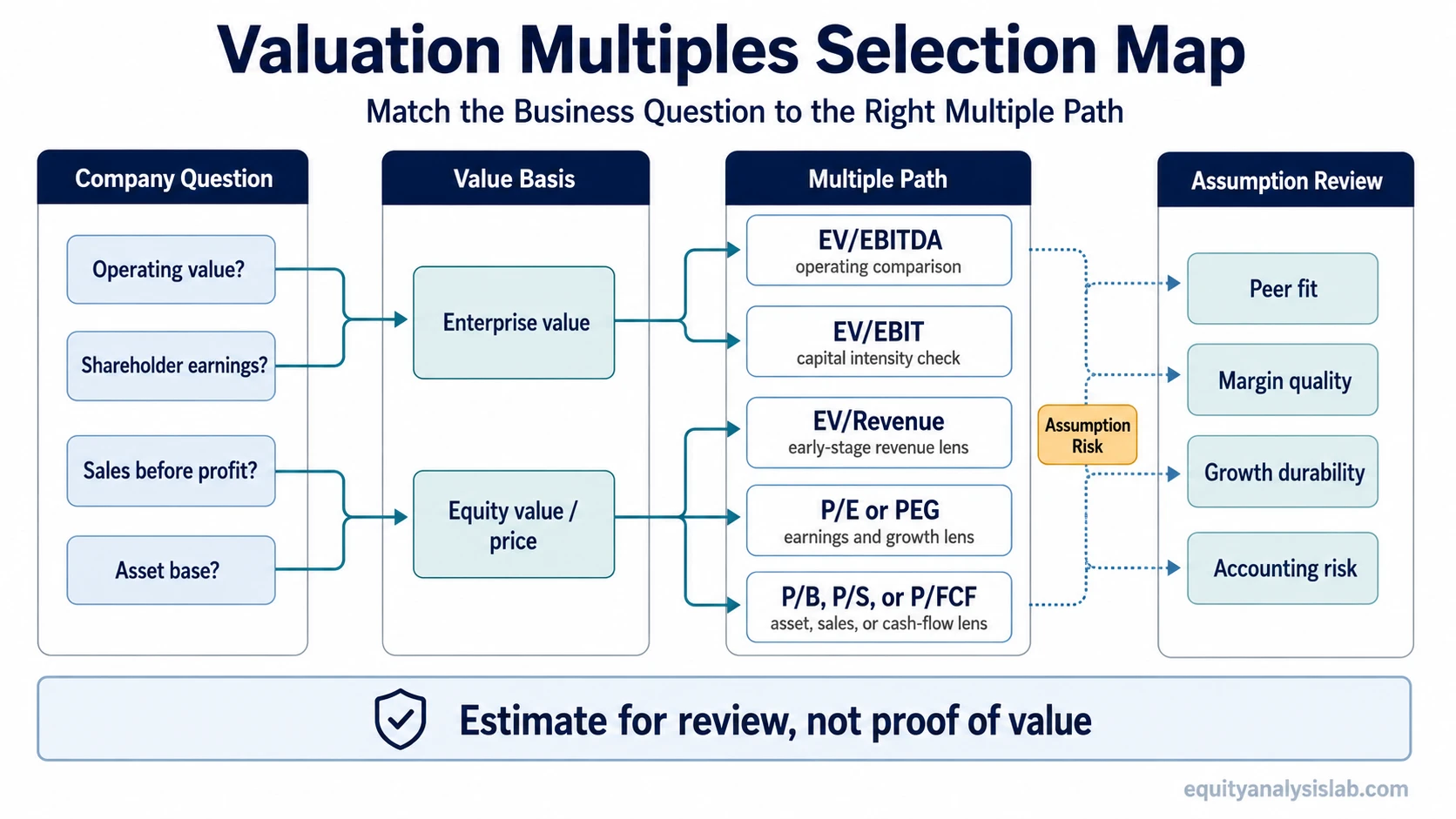

Valuation multiples compare company value with a business metric such as earnings, sales, cash flow, EBITDA, EBIT, or book value. The useful next step is choosing the multiple that matches the value measure, business model, capital structure, and assumption risk being reviewed.

A multiple is most useful when the numerator and denominator measure compatible things. Enterprise value belongs with operating metrics before financing effects, while equity value or share price belongs with metrics available to common shareholders. A clean comparison starts by matching the question to the metric rather than treating every multiple as interchangeable.

How Valuation Multiples Are Organized

Valuation multiples usually fall into practical groups. Enterprise value multiples pair operating value with operating measures. Equity multiples pair shareholder value with earnings, book value, cash flow, or sales. Growth-adjusted multiples add a growth lens, but they still depend on earnings quality and the assumptions behind the growth estimate.

| Multiple group | Typical question | What to check before using it |

|---|---|---|

| Enterprise value multiples | How does operating value compare before financing mix? | Debt, cash, leases, margins, and capital intensity. |

| Equity earnings multiples | How much are shareholders paying for earnings? | Net income quality, one-time items, dilution, and growth durability. |

| Revenue multiples | How is the market valuing sales when earnings are weak or not yet stable? | Gross margin, path to profitability, revenue quality, and peer maturity. |

| Book-value multiples | How does market value compare with accounting net assets? | Asset quality, write-down risk, financial-sector relevance, and intangible assets. |

| Cash-flow multiples | How does price compare with cash generation available after reinvestment? | Capital expenditure needs, working-capital swings, and cash conversion. |

Which Valuation Multiple Should You Start With?

The starting point depends on the business question. A mature profitable company, an asset-heavy financial business, a high-growth software company, and a cyclical industrial company may all require different multiples before the comparison becomes meaningful.

| Analytical question | Useful starting point | Why it matters | Assumption risk to check | Related comparison path |

|---|---|---|---|---|

| Do you need operating value before capital structure effects? | EV/EBITDA | Focuses on enterprise value relative to EBITDA before interest and tax effects. | Capital expenditure needs, lease treatment, and margin quality. | Compare with P/E when financing mix changes the view. |

| Do depreciation and amortization matter for the business model? | EV/EBIT | Includes depreciation and amortization, which can matter for asset-heavy companies. | Accounting policies, reinvestment needs, and operating margin comparability. | Use after checking whether EBITDA hides capital intensity. |

| Is the company still early-stage or temporarily unprofitable? | EV-to-revenue | Uses revenue when operating profit is not yet stable enough for earnings-based comparison. | Gross margin, revenue retention, profitability path, and peer maturity. | Compare with sales-based equity multiples only after capital structure is considered. |

| Are you comparing shareholder value to current earnings? | price-to-earnings multiple | Connects share price with earnings available to common shareholders. | One-time gains, cyclicality, share count changes, and earnings durability. | Use forward versus trailing earnings when earnings are changing quickly. |

| Do you need a growth-adjusted earnings lens? | PEG ratio | Relates a P/E multiple to expected growth instead of viewing the earnings multiple alone. | Growth forecast quality, margin expansion assumptions, and earnings base effects. | Compare with P/E when growth expectations drive the valuation gap. |

| Is book value central to the business model? | price-to-book ratio | Compares market value with accounting equity, often more relevant for asset-heavy or financial companies. | Asset quality, intangible assets, write-down risk, and return on equity. | Use carefully outside sectors where book value has clear analytical meaning. |

| Is cash generation more useful than accounting earnings? | price-to-free-cash-flow | Compares equity value with free cash flow after operating needs and reinvestment. | Capital expenditure cycle, working-capital timing, and recurring cash conversion. | Check whether free cash flow is temporarily inflated or depressed. |

| Are sales the only stable metric available? | price-to-sales ratio | Uses sales as the comparison base when earnings or free cash flow are not yet stable. | Gross margin, dilution, future profitability, and revenue quality. | Revenue multiples need more caution when margins differ sharply across peers. |

Enterprise Value Multiples vs Equity Multiples

Enterprise value multiples compare the value of the operating business with operating metrics before the financing mix is fully reflected. They are often useful when companies have different debt, cash, or lease structures.

Equity multiples start from the value available to common shareholders. They are more direct when the question is about share price, earnings per share, book value per share, or cash flow available to equity holders.

Practical boundary: enterprise value and equity value should not be mixed casually. EV-based numerators belong with operating denominators such as EBITDA, EBIT, or revenue. Price or market capitalization belongs with equity-level denominators such as earnings, book value, free cash flow, or sales per shareholder context.

A Light Example of Choosing the First Multiple

A company with stable earnings, modest leverage, and a long operating history may be easier to begin with through a P/E-style earnings lens. A company with heavy debt or a very different cash balance than peers may require an enterprise value lens first. A company with fast revenue growth but limited current profit may need a revenue multiple, followed by a margin and cash-flow review.

The example does not make one multiple automatically correct. It shows why the metric should follow the business question. The same company can look different under different multiples when growth, margins, debt, accounting choices, cyclicality, or market sentiment change the interpretation.

When Multiples Can Mislead

Valuation multiples can look precise while hiding weak assumptions. A low multiple is not proof that a stock is undervalued, and a high multiple is not proof that a stock is overvalued. The multiple only becomes useful after the peer set, accounting base, business quality, growth profile, margin structure, and capital structure are checked.

| Risk area | How it can distort the multiple | What to review |

|---|---|---|

| Peer mismatch | Companies may share a sector label but have different margins, growth, risks, or business models. | Comparable company quality, geography, segment mix, and growth stage. |

| Accounting differences | Reported earnings, EBITDA, book value, or free cash flow may not be measured consistently. | One-time items, lease treatment, depreciation policy, capitalized costs, and working capital. |

| Capital structure | Debt and cash can make equity multiples and enterprise value multiples tell different stories. | Net debt, cash balances, interest expense, refinancing risk, and dilution. |

| Cyclicality | Peak earnings can make a cyclical company look cheaper than it really is across a full cycle. | Normalized margins, cycle position, commodity sensitivity, and demand conditions. |

| Growth and sentiment | Multiple expansion or compression can reflect optimistic or pessimistic expectations that are not visible in the ratio alone. | Revenue durability, margin expansion, reinvestment needs, return on invested capital, and market sentiment. |

Related Valuation Multiple Comparisons

Some valuation questions are easier to resolve through direct comparisons between multiples. The difference between EV/EBITDA vs P/E ratio is especially useful when capital structure, depreciation, or tax effects change the interpretation.

The difference between forward P/E vs trailing P/E matters when the market is pricing future earnings differently from the most recently reported earnings base.

Common Questions About Valuation Multiples

What is a valuation multiple?

A valuation multiple is a ratio that compares company value or share price with a business metric such as earnings, sales, EBITDA, EBIT, free cash flow, or book value.

Are enterprise value multiples and equity multiples the same?

No. Enterprise value multiples compare operating value with operating metrics, while equity multiples compare shareholder value or share price with equity-level metrics such as earnings or book value.

Does a low valuation multiple mean a stock is cheap?

No. A low multiple can reflect risk, weak growth, cyclicality, leverage, accounting issues, or poor business quality. The multiple must be reviewed with assumptions and peer context.

Which valuation multiple should investors start with?

The starting point depends on the question. Enterprise value multiples help with operating-value comparisons, P/E helps with shareholder earnings comparisons, PEG adds a growth lens, and sales or book-value multiples fit narrower situations.