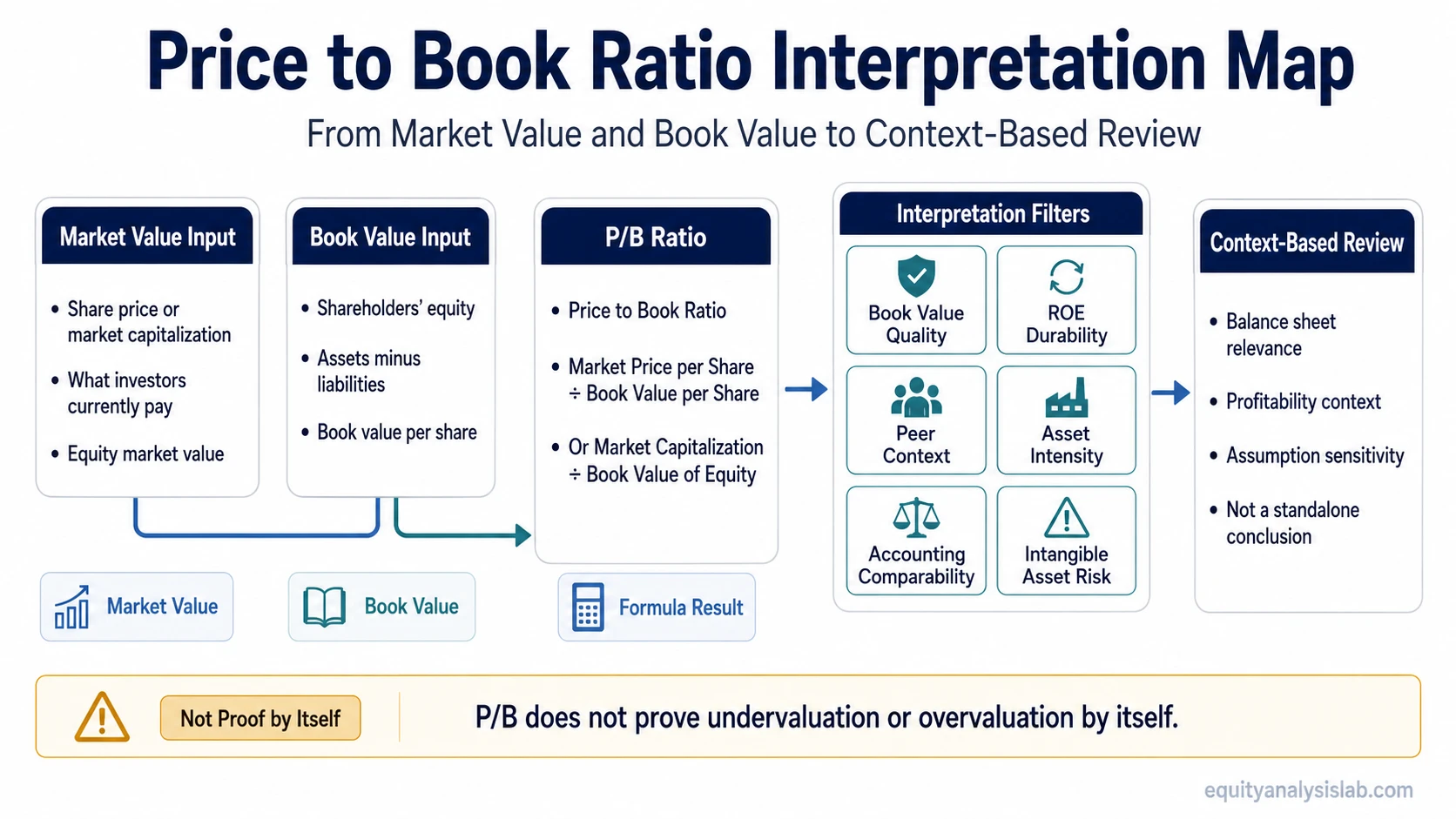

Price to book ratio compares a company’s market price with its book value of equity, showing how much investors are paying for each dollar of accounting net assets. The number becomes useful only after book value quality, peer context, profitability, and asset intensity are reviewed.

A low P/B ratio can reflect a valuation discount, but it can also reflect weak returns, impaired assets, poor growth expectations, or accounting values that no longer represent economic value. A high P/B ratio can reflect stronger profitability, durable intangible value, or optimistic expectations, but it does not prove that the stock is overpriced by itself.

Key Points

- Price to book ratio compares market value with book value of equity.

- The basic formula is market price per share divided by book value per share.

- P/B is usually more useful for asset-heavy, financial, and balance-sheet-driven businesses than for asset-light companies dominated by intangible assets.

- A good P/B ratio depends on peer comparability, return on equity, growth expectations, balance sheet quality, and accounting treatment.

- The ratio should not be used as standalone proof that a company is cheap or expensive.

What Is the Price to Book Ratio?

The price to book ratio, also called the P/B ratio or price to book value ratio, measures a company’s market value relative to its book value of equity. Book value of equity is the accounting value of shareholders’ equity, generally calculated as total assets minus total liabilities.

In valuation work, P/B asks a narrow question: how much is the market paying for the company’s net assets on the balance sheet? That makes the ratio most relevant when those recorded assets are economically meaningful and comparable across similar companies.

Definition: Price to book ratio is a valuation multiple that compares market price or market capitalization with book value of equity.

Price to Book Ratio Formula

The most common per-share formula is:

Price to Book Ratio = Market Price per Share ÷ Book Value per Share

The same idea can also be calculated at the company level:

Price to Book Ratio = Market Capitalization ÷ Book Value of Equity

| Input | Meaning | Why it matters |

|---|---|---|

| Market price per share | The current market value assigned to one share | Represents what investors are paying in the market |

| Book value per share | Shareholders’ equity divided by shares outstanding | Represents accounting net assets per share |

| Market capitalization | Share price multiplied by shares outstanding | Represents total equity market value |

| Book value of equity | Total assets minus total liabilities | Represents accounting equity available to shareholders |

The formula is simple, but the denominator can be difficult to interpret. Book value may be affected by write-offs, acquisitions, accumulated losses, buybacks, accounting treatment, or assets that do not reflect current economic value.

What the Price to Book Ratio Shows

P/B shows the market value placed on a company’s accounting equity. A ratio of 1.0x means the market value is equal to book value. A ratio above 1.0x means the market values the company above accounting equity. A ratio below 1.0x means the market values the company below accounting equity.

That comparison can be useful, but it is not a full valuation by itself. The market may pay more than book value for a company with strong returns on equity, durable profitability, valuable intangible assets, or high expected growth. It may pay less than book value when assets are impaired, returns are weak, liabilities are risky, or future economics look poor.

How to Interpret a Low or High Price to Book Ratio

A low, near-book, or high P/B ratio needs context before it can be interpreted. The same number can mean different things across banks, insurers, manufacturers, software companies, retailers, and asset-heavy industrial businesses.

| P/B range | Possible interpretation | What to check before judging it |

|---|---|---|

| Below 1.0x | The market values the company below accounting book value | Asset quality, impairment risk, ROE, balance sheet risk, and business decline |

| Around 1.0x | The market value is close to book value | Peer multiples, profitability, capital intensity, and whether book equity is meaningful |

| Above 1.0x | The market values the company above accounting book value | ROE durability, growth expectations, intangible value, and margin structure |

A low P/B ratio can be attractive only if the assets are reliable and the business can earn acceptable returns on them. A high P/B ratio can be reasonable only if the company’s economics justify paying more than recorded equity.

Simple Price to Book Ratio Example

A hypothetical company has $500 million in assets and $300 million in liabilities. Its book value of equity is $200 million. If it has 20 million shares outstanding, book value per share is $10. If the stock trades at $15, the price to book ratio is 1.5x.

The 1.5x result means the market is paying $1.50 for each $1.00 of accounting equity. That number does not tell whether the stock is attractive by itself. The interpretation depends on the company’s asset quality, return on equity, peer group, balance sheet structure, and business model.

Price to Book Ratio Assumption Stack

P/B becomes more useful when the analyst reviews why market value differs from book value. The ratio is not only a formula result; it is a starting point for testing the assumptions behind the market’s valuation of equity.

| Interpretation variable | Why it changes P/B meaning |

|---|---|

| Book value quality | Weak, overstated, or impaired assets can make a low P/B ratio misleading. |

| ROE and profitability | A higher P/B ratio can be more explainable when returns on equity are strong and durable. |

| Growth expectations | Market value may exceed book value when investors expect future economics to matter more than recorded assets. |

| Required return | Higher perceived risk can lower the multiple investors are willing to pay for the same book equity. |

| Asset intensity | P/B is usually more relevant when assets are central to the business model. |

| Accounting comparability | Different accounting treatments can distort comparisons across companies and sectors. |

| Negative book value | The ratio can become unusable or misleading when book equity is negative. |

When Price to Book Ratio Is Most Useful

P/B is most useful when book value is a meaningful proxy for the economic capital used by the business. This often makes the ratio more relevant for asset-heavy companies, financial institutions, insurers, mature industrial businesses, and peer groups where balance sheet comparability is strong.

| More useful when | Weaker when |

|---|---|

| Assets are central to value creation | Intangible assets dominate the business model |

| Book equity is positive and economically meaningful | Book value is negative, distorted, or heavily impaired |

| Peer accounting is comparable | Accounting treatment differs materially across peers |

| ROE can be compared across similar businesses | Profitability is unstable or not tied to the asset base |

| Earnings are temporarily depressed but assets remain relevant | Buybacks, acquisitions, or write-offs distort shareholders’ equity |

For asset-light companies, book value may understate the economic value of brands, software, customer relationships, networks, or intellectual property. In those cases, P/B can still provide balance sheet context, but it is rarely enough to support a valuation view alone.

Limitations of Price to Book Ratio

Book value is accounting-based. The denominator reflects accounting equity, not necessarily current market value, replacement value, liquidation value, or intrinsic value.

Intangible-heavy businesses can look expensive. Companies with valuable brands, software, patents, or network effects may trade at high P/B ratios because much of their economic value is not fully captured on the balance sheet.

Low P/B can signal distress. A company trading below book value may be facing asset impairments, weak profitability, high leverage, declining economics, or poor reinvestment prospects.

Peer context is necessary. P/B ratios are more useful when companies have similar accounting rules, capital intensity, profitability profiles, and business models.

Price to Book Ratio vs Other Valuation Multiples

P/B focuses on the balance sheet, while other valuation multiples focus on different parts of the business. A price-to-earnings multiple compares market value with earnings, so it is usually more relevant when profitability is stable and meaningful.

The PEG ratio adjusts an earnings multiple by expected growth, which makes growth assumptions more visible. A revenue-based multiple can be more useful when earnings are negative or temporarily distorted, but it still needs margin and business quality context.

The useful multiple depends on the analytical question. P/B is strongest when the balance sheet matters to valuation. It is weaker when the company’s value comes mainly from future earnings power, cash flow conversion, or intangible assets that accounting equity does not capture well.

Common Mistakes When Using Price to Book Ratio

Mistake 1: Treating low P/B as automatic undervaluation. A low ratio can reflect poor asset quality, weak returns, or a business model that deserves a discount.

Mistake 2: Comparing unrelated companies. A bank, a software company, and a manufacturer can have very different relationships between book value and economic value.

Mistake 3: Ignoring return on equity. A company trading above book may still have a reasonable valuation context if it earns durable returns on equity, while a company near book value may be less attractive if it cannot earn adequate returns.

FAQ

What is the price to book ratio?

The price to book ratio is a valuation multiple that compares a company’s market price or market capitalization with its book value of equity.

What is the price to book ratio formula?

The common formula is market price per share divided by book value per share. It can also be calculated as market capitalization divided by book value of equity.

Is a low price to book ratio good?

A low P/B ratio is not automatically good. It can suggest a valuation discount, but it can also reflect weak profitability, impaired assets, or balance sheet risk.

Is a high price to book ratio bad?

A high P/B ratio is not automatically bad. It can reflect strong ROE, valuable intangible assets, higher expected growth, or optimistic market assumptions.

When is price to book ratio most useful?

P/B is usually most useful for asset-heavy, financial, or balance-sheet-driven businesses where accounting book value is economically meaningful and comparable across peers.