Valuation is the process of estimating what a business or security may be worth under a set of assumptions. For investors, it connects price with business value, cash flow, growth, risk, and market comparison.

A valuation estimate is not proof of upside, safety, or future return. The result depends on the question being asked, the method used, the quality of the business evidence, and how sensitive the range is to inputs such as cash flow, growth, discount rate, terminal value, balance sheet context, and market multiples.

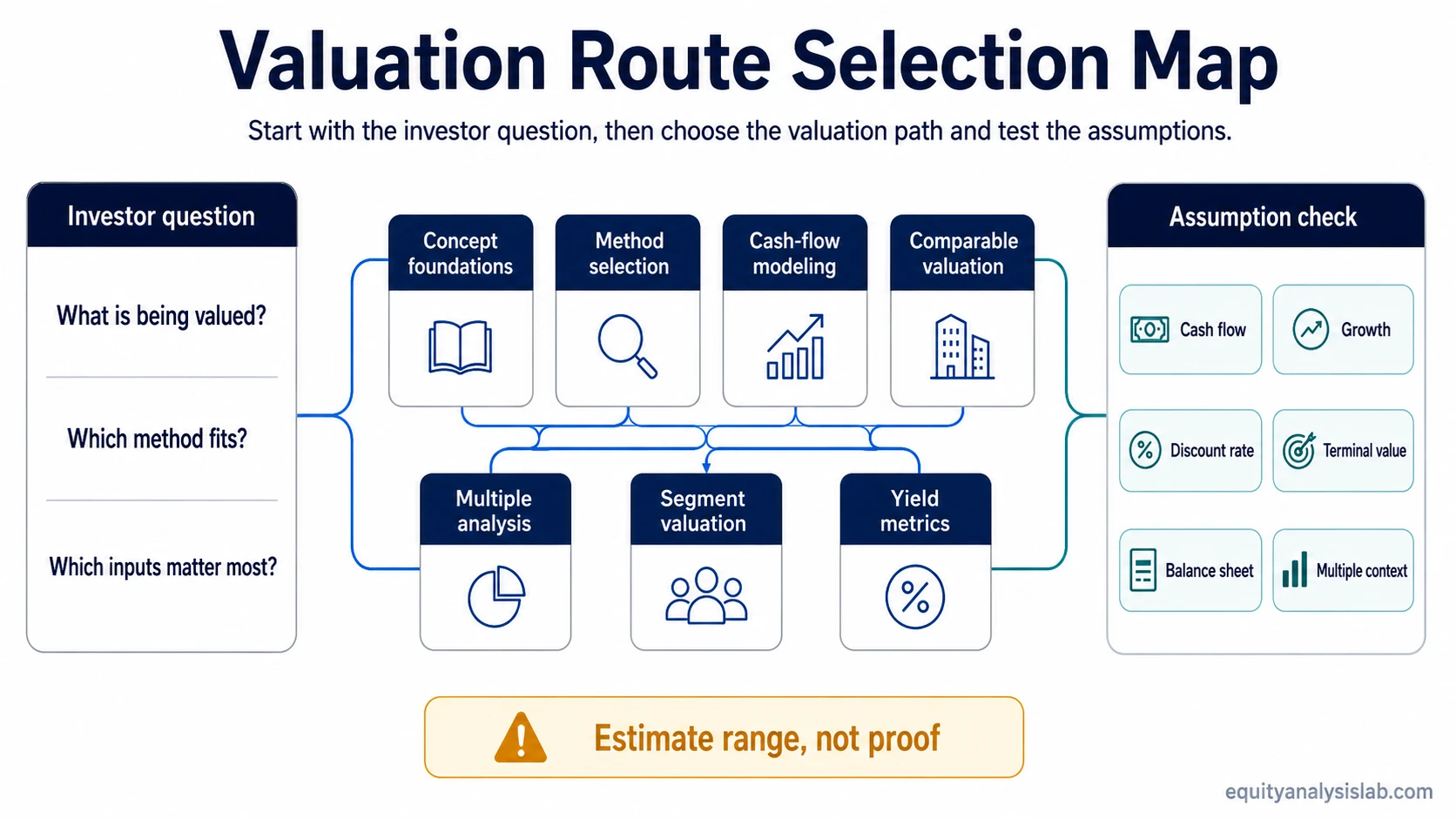

Definition: valuation organizes an investor’s estimate of business value. It can use concept work, method selection, market comparison, yield-based metrics, or sensitivity testing, depending on the research problem.

What valuation organizes for investors

Valuation gives structure to a basic investment question: is the current price reasonable compared with a disciplined estimate of business value? That estimate may come from cash-flow modeling, market multiples, earnings yield, asset value, or a combination of approaches.

The useful starting point is not a formula. It is the question behind the work. A business with stable cash flows may require a different valuation path than a cyclical company, a high-growth company, a segment-heavy company, or a stock that looks cheap because the market is pricing in risk.

Main valuation routes

| Investor question | Best valuation path | What it clarifies | Best next topic |

|---|---|---|---|

| I need the basic language first. | Concept foundations | Value, price, estimates, assumptions, enterprise value, equity value, and related terms. | valuation concepts |

| I need to choose a valuation approach. | Method selection | How different estimate-building methods fit different company and evidence types. | valuation methods |

| I need intrinsic-value style work. | Cash-flow modeling | How future cash flows, discount rates, and terminal inputs shape an estimate. | discounted cash flow |

| I need market-comparison context. | Comparable valuation | How the market prices similar companies, business models, margins, growth, and risk. | relative valuation |

| I need to compare valuation ratios. | Multiple analysis | How price, earnings, sales, book value, EBITDA, and free cash flow relate to market value. | valuation multiples |

| I need to value different business segments separately. | Segment-level valuation | How different business units can require different assumptions or comparison sets. | sum-of-the-parts valuation |

| I need earnings or cash-flow yield context. | Yield-based metrics | How earnings or cash flow compares with price in yield terms. | yield-based valuation metrics |

How the main valuation paths differ

Concept work comes first when the problem is language clarity. Terms such as intrinsic value help separate market price from an investor’s estimate. Price vs value clarifies the same distinction from the market-price side.

Method work becomes necessary when the question moves from meaning to estimate construction. Discounted cash flow, relative valuation, and segment-based valuation answer different questions, so they should not be treated as interchangeable tools.

Multiple work helps compare how the market prices similar companies, but a multiple is only useful when business quality, margin structure, growth durability, accounting quality, and balance sheet risk are understood.

Yield-based work translates earnings or cash flow into yield terms. For example, cash flow yield can help compare price with cash generation, but the interpretation still depends on durability, reinvestment needs, and capital allocation.

How assumptions change valuation conclusions

Valuation conclusions can change sharply when the inputs change. A small adjustment in growth, discount rate, terminal value, normalized margin, share count, or balance sheet risk can move an estimate enough to change the investment interpretation.

| Assumption area | Why it matters | Common mistake |

|---|---|---|

| Cash flow | Cash generation supports the estimate more directly than narrative alone. | Treating accounting earnings as durable without checking cash conversion. |

| Growth | Higher growth can justify a higher range only if durability and reinvestment economics support it. | Using optimistic growth without checking quality, competition, or capital needs. |

| Discount rate | The required return changes how future cash flows are translated into present value. | Using a precise-looking rate while ignoring business risk and uncertainty. |

| Terminal value | Long-term inputs can dominate a model, especially for growth companies. | Letting a distant input drive most of the conclusion. |

| Balance sheet context | Debt, cash, dilution risk, and financial flexibility can change what equity holders actually own. | Comparing companies by headline multiples while ignoring leverage or dilution. |

| Multiple context | A low or high multiple only has meaning relative to quality, growth, cyclicality, and risk. | Calling a low multiple a bargain before asking what risk the market may be pricing. |

A simple assumption-sensitivity example

A company can look inexpensive on a headline multiple and still deserve caution if cash flow is weak, share dilution is rising, or the valuation depends on growth lasting much longer than the evidence supports. The same business can look more defensible if cash generation is durable, reinvestment economics are strong, and the valuation does not require aggressive terminal assumptions.

The practical distinction is that valuation is not just price divided by one metric. It is the relationship between price, business quality, cash flow, growth, risk, and the inputs needed to connect them.

What valuation does not prove

Valuation does not prove that a stock is cheap, expensive, safe, or likely to produce a specific return. A valuation estimate is a disciplined range built from assumptions. The estimate becomes more useful when the investor can explain which inputs matter most and what evidence would weaken them.

Full formulas, model construction, and company-specific worked examples belong in dedicated method, metric, and case materials. The useful role here is to keep the valuation question clear before the investor moves into a more detailed estimate.

A margin of safety can help frame the gap between price and estimate, but it does not remove business risk, model risk, liquidity risk, or the possibility that the estimate itself is wrong.

Where to go next

| Sequence | Next action |

|---|---|

| 1. Define the terms | Start with value, price, enterprise value, equity value, assumptions, and estimate ranges. |

| 2. Choose the method | Match the valuation approach to the business type, available evidence, and research question. |

| 3. Test the inputs | Check how cash flow, growth, discount rate, terminal value, balance sheet context, and multiples affect the conclusion. |

| 4. Compare price with evidence | Use the estimate range as a discipline tool, not as proof of future return or safety. |