Cash flow yield compares a company’s cash-flow measure with a value measure, such as market value or enterprise value, so the result only makes sense when the cash-flow base and denominator match.

As a valuation lens, cash flow yield translates cash generation into a percentage of value. A higher percentage can make a company look less expensive, but the ratio can also reflect temporary cash flow, leverage, cyclicality, or underinvestment. The useful question is whether the selected cash-flow measure is sustainable and whether the value base represents the same economic claim.

Key Points

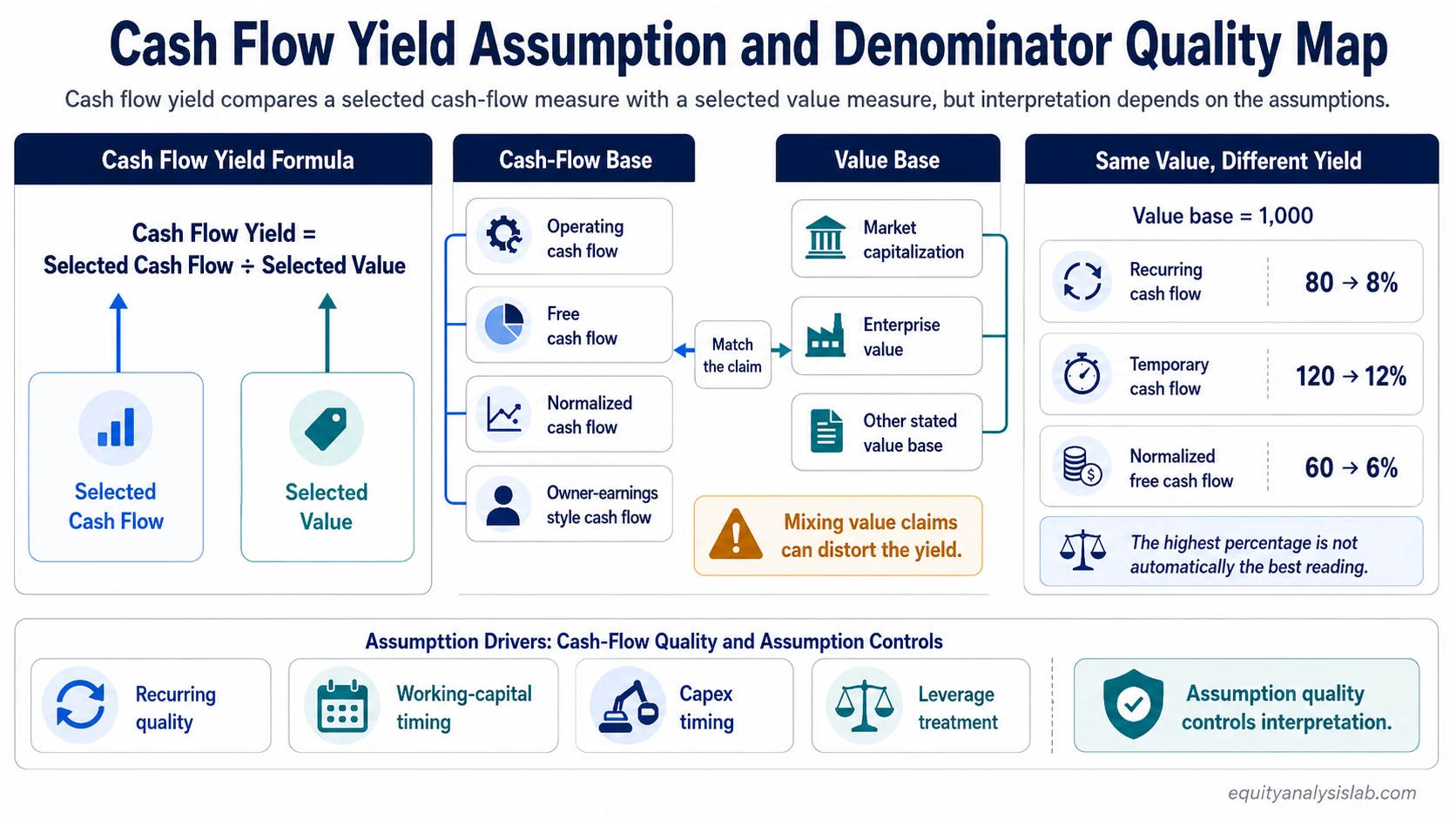

- Cash flow yield is a yield-based valuation ratio: selected cash flow divided by selected value.

- The numerator matters because operating cash flow, free cash flow, normalized cash flow, and owner-earnings-style cash flow can produce different readings.

- The denominator must match the cash-flow claim. Equity value and enterprise value are not interchangeable.

- A high yield can reflect real cash generation, cyclicality, leverage risk, temporary working-capital inflow, or underinvestment.

What Cash Flow Yield Means

Cash flow yield measures how much cash flow a company produces relative to a chosen value base. The ratio is usually expressed as a percentage, which makes it easier to compare cash generation with the price or value assigned to the business.

If a business is valued at 1,000 and produces 80 of the selected cash-flow measure, the cash flow yield is 8%. The harder part is deciding whether that 80 is recurring, temporary, levered, unlevered, maintenance-adjusted, or distorted by timing.

Cash flow yield is broader than free cash flow yield. Free cash flow yield normally focuses on free cash flow after capital expenditures. Cash flow yield can refer to several cash-flow bases, so the analyst has to state the base before interpreting the percentage.

Cash Flow Yield Formula

The general formula is:

Cash flow yield = selected cash-flow measure / selected value measure

The selected cash-flow measure may be operating cash flow, free cash flow, normalized free cash flow, owner-earnings-style cash flow, or another defined cash-flow base. The selected value measure may be market capitalization, enterprise value, or another clearly stated value base.

The formula is useful only when the numerator and denominator describe the same economic claim. Equity cash flow should normally be compared with equity value. Cash flow available to all capital providers should normally be compared with enterprise value. Mixing claims can make the ratio look cleaner than the economics really are.

Why the Cash-Flow Base Matters

The cash-flow base controls much of the interpretation. Operating cash flow can include working-capital movements that may not repeat. Free cash flow includes capital expenditures, but capex may be temporarily high or low. Normalized cash flow tries to smooth unusual timing, but it introduces analyst judgment.

A strong cash flow yield from recurring operations is different from a strong cash flow yield caused by delayed supplier payments, reduced inventory, temporarily low capex, or a one-time tax benefit. The percentage may look similar, but the valuation question is different.

| Input | What It Controls | Common Distortion | Interpretation Question |

|---|---|---|---|

| Operating cash flow | Cash generated before capital expenditures | Working-capital timing can temporarily lift or reduce it | Is the cash flow recurring or mostly timing-driven? |

| Free cash flow | Cash after capital expenditures | Capex may be unusually high, unusually low, or deferred | Does the capex level reflect maintenance needs or a temporary cycle? |

| Normalized cash flow | A smoothed estimate of cash generation | Normalization can hide real deterioration if assumptions are too generous | Which adjustments were made, and are they defensible? |

| Market capitalization | Equity value only | Debt and cash can be ignored if the numerator belongs to the whole firm | Is the cash-flow measure available to equity holders only? |

| Enterprise value | Value of the whole operating business | Cash, debt, leases, or minority interests may change comparability | Does the denominator match a pre-debt or enterprise-level cash-flow base? |

How Assumptions Change the Yield

The same company value can produce several cash flow yield readings because each version uses a different cash-flow base.

| Value Base | Cash-Flow Assumption | Cash Flow Used | Cash Flow Yield | What the Reading May Miss |

|---|---|---|---|---|

| 1,000 | Recurring operating cash flow | 80 | 8.0% | Still needs capex and leverage context |

| 1,000 | Temporarily boosted cash flow | 120 | 12.0% | Working-capital release may not repeat |

| 1,000 | Normalized free cash flow | 60 | 6.0% | Normalization may depend on capex assumptions |

The useful reading is not simply the highest percentage. It is the reading that best matches sustainable cash generation, value denominator, capital intensity, leverage, and peer comparability.

Cash Flow Yield vs Free Cash Flow Yield and Earnings Yield

Cash flow yield, free cash flow yield, and earnings yield are related, but they answer different valuation questions. The distinction matters because cash flow and earnings can diverge when depreciation, capex, working capital, stock-based compensation, or one-time items affect reported results.

| Metric | Main Base | Best Used For | Main Caution |

|---|---|---|---|

| Cash flow yield | Selected cash-flow measure | Broad cash-generation comparison across a chosen value base | The cash-flow base must be defined before the ratio means much |

| Free cash flow yield | Free cash flow after capex | Testing valuation against cash left after reinvestment needs | Capex timing and maintenance versus growth capex can distort the reading |

| Earnings yield | Earnings, often EPS or net income | Comparing accounting earnings with price or market value | Earnings may not convert into cash, and accounting items can affect comparability |

Illustrative Example

Suppose a hypothetical company has a value base of 1,000. If the analyst uses recurring operating cash flow of 80, the cash flow yield is 8%. If the analyst uses temporarily boosted cash flow of 120, the yield rises to 12%. If the analyst uses normalized free cash flow of 60, the yield falls to 6%.

The company value did not change in this example. The interpretation changed because the cash-flow measure changed. That is why cash flow yield should be read together with the source of cash flow, the reinvestment requirement, the capital structure, and the reason any adjustment was made.

When Cash Flow Yield Can Mislead

A high cash flow yield can be useful, but it can also reflect falling market value, temporary cash-flow strength, cyclicality, leverage pressure, or underinvestment.

It can mislead when a company cuts necessary investment to make free cash flow look stronger, when working capital creates a temporary inflow, when a cyclical peak is treated as normal, or when enterprise-level cash flow is compared with an equity-only denominator.

A low cash flow yield can also have more than one meaning. It may reflect weak cash generation, but it may also reflect heavy reinvestment, growth investment, or a valuation base that already prices in stronger future cash flow. The ratio frames the question; it does not answer the whole valuation problem.

How to Use Cash Flow Yield in Valuation

Cash flow yield is most useful as a comparison tool after the analyst defines the cash-flow base, adjusts for obvious timing effects, and checks whether the denominator matches the claim being measured.

For peer comparisons, the ratio is stronger when companies have similar capital intensity, accounting policies, tax profiles, leverage, and reinvestment needs. Without those checks, the comparison can reward the company with the most favorable timing rather than the better cash-generation profile.

A practical valuation review usually asks four questions: what cash-flow base is being used, whether that base is recurring, whether the value denominator matches the claim, and what would change the interpretation if capex, working capital, leverage, or normalization assumptions changed.