Asset allocation is the way a portfolio is divided across asset classes and exposures, such as stocks, bonds, cash, funds, sectors, regions, or other investment categories. The allocation is expressed through weights, not just through the names of the investments held.

In portfolio construction, asset allocation is a structure decision. It helps define where portfolio risk and return exposure may come from, but it does not guarantee safety, prevent losses, forecast returns, or create a personalized investment mix.

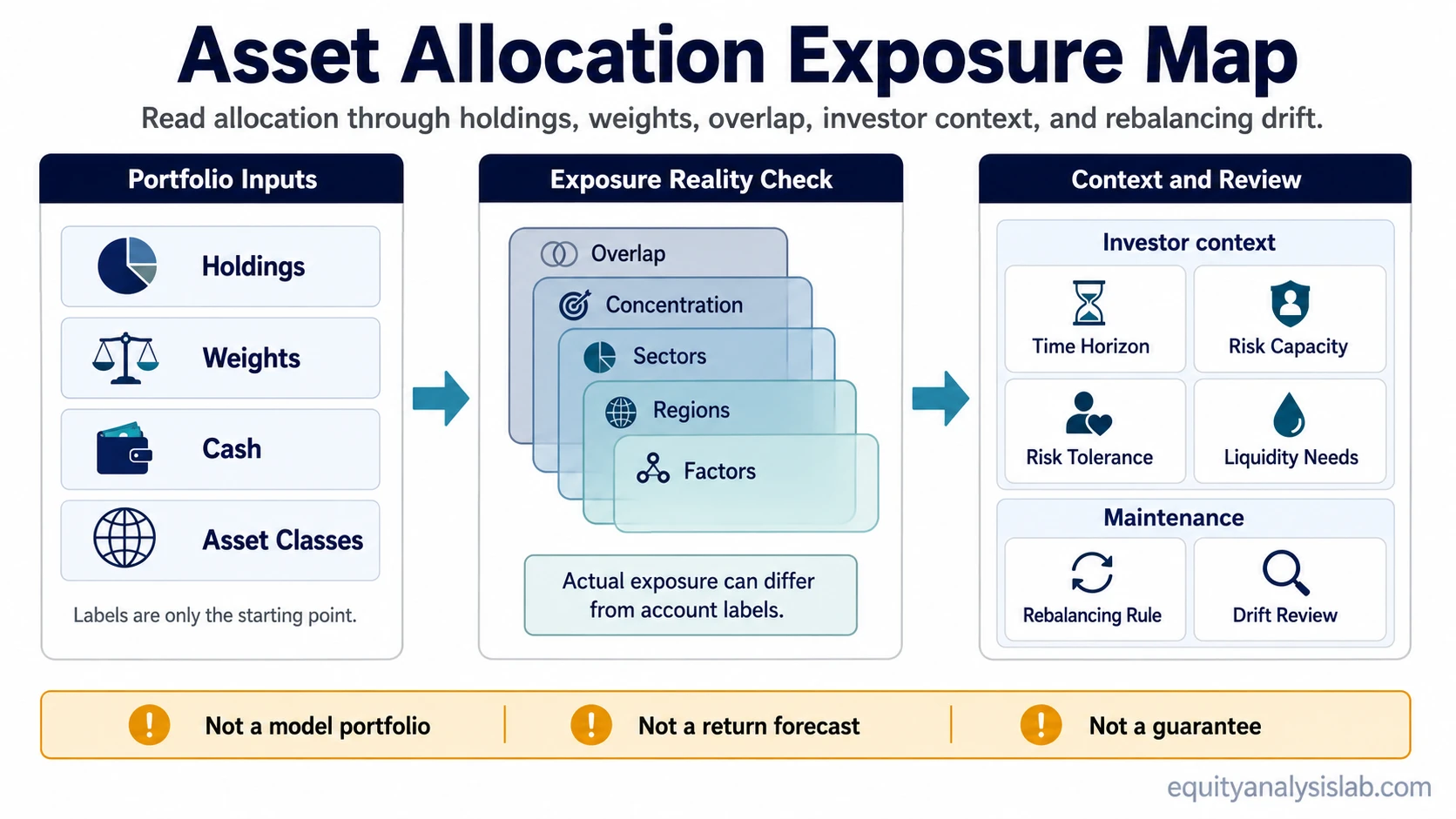

What Asset Allocation Means

Asset allocation is the combined result of what a portfolio owns, how much each part weighs, how exposures overlap, and how those exposures fit the investor’s time horizon, risk capacity, and rebalancing rule.

A simple label such as “stock fund,” “bond fund,” or “cash” can be useful, but the label is not enough. Two investments with different names can still share similar underlying securities, sectors, regions, or risk factors. Asset allocation should be read through actual holdings and weights.

Key Points About Asset Allocation

- Asset allocation describes the portfolio mix across asset classes and exposures.

- Weights matter because large positions drive more portfolio behavior than small positions.

- Holdings overlap can make a portfolio less varied than it appears from fund count alone.

- Time horizon, risk capacity, risk tolerance, liquidity needs, and investment objectives all affect allocation decisions.

- Rebalancing drift can change the allocation over time as market prices move.

How Asset Allocation Works in a Portfolio

Asset allocation starts with the broad mix of portfolio exposures. A portfolio may hold stocks, bonds, cash, funds, real assets, or other categories. Each category affects the portfolio differently because each one has its own risk, liquidity, income, volatility, and return characteristics.

The next layer is weighting. A holding that represents a large share of the portfolio can dominate the result, while a small holding may have limited effect even if it looks important on a list of positions.

Allocation also depends on what sits underneath each position. A portfolio can own several funds and still have repeated exposure to the same large companies, sectors, or factors. That repeated exposure can increase concentration even when the account appears broad at first glance.

Cash is part of the allocation too. It can reduce market exposure, provide flexibility, or reflect liquidity needs, but it also changes the portfolio’s expected behavior. The role of cash depends on the investor’s objectives, time horizon, and need for access to capital.

Asset Allocation Inputs

The main inputs behind asset allocation are not limited to risk preference. A useful allocation view connects the portfolio’s structure to the investor’s financial situation, time horizon, and ability to tolerate uncertainty without turning the mix into a model recommendation.

Risk capacity and risk tolerance are related, but they are not the same. Risk tolerance describes emotional comfort with volatility or losses. Risk capacity describes the financial ability to absorb losses, illiquidity, or a delayed recovery without disrupting the investor’s actual needs.

Time horizon changes the interpretation. Capital needed soon usually has less room to absorb volatility than capital that can remain invested for many years. Liquidity needs, income needs, tax constraints, and existing holdings can also change the way an allocation should be understood.

Observable Inputs That Shape Asset Allocation

| Allocation input | What it shows | Why it matters |

|---|---|---|

| Holdings | What the portfolio actually owns | Allocation depends on real exposure, not only account labels. |

| Weights | How much each holding or asset class contributes | Small and large positions do not affect the portfolio equally. |

| Concentration | Whether exposure is clustered in a few holdings, sectors, or factors | Clustered exposure can dominate portfolio risk even when the asset-class mix looks balanced. |

| Overlap | Whether funds or holdings share the same underlying exposures | Multiple funds can still repeat exposure to the same securities, sectors, or risk factors. |

| Time horizon | How long the investor expects capital to remain invested | A longer or shorter horizon can change how much volatility the portfolio can absorb. |

| Risk capacity | The financial ability to withstand losses or illiquidity | Capacity can differ from emotional risk tolerance. |

| Risk tolerance | The emotional comfort level with volatility and uncertainty | A portfolio can feel acceptable in calm markets but become difficult to hold during stress. |

| Rebalancing rule | How drift is corrected over time | Without a rule, the allocation can change as markets move. |

Asset Allocation vs Diversification vs Rebalancing

Asset allocation, diversification, and rebalancing are connected, but they solve different portfolio questions.

| Concept | Main question | Portfolio role |

|---|---|---|

| Asset allocation | How is the portfolio divided across exposures? | Sets the broad structure of the portfolio mix. |

| Diversification | How spread out is the risk inside or across that mix? | Reduces dependence on a narrow set of holdings, sectors, or drivers. |

| Rebalancing | How is the mix brought back after it drifts? | Maintains the intended structure when market moves change weights. |

A portfolio can have an allocation without being well diversified. It can also drift away from its intended allocation if no rebalancing rule exists.

Common Asset Allocation Mistakes

- Treating fund count as exposure spread: Owning many funds does not automatically mean the portfolio has many different underlying exposures.

- Ignoring overlap: Several funds can hold similar companies, sectors, regions, or factors.

- Confusing risk tolerance with risk capacity: Comfort with volatility is not the same as the financial ability to withstand losses or illiquidity.

- Using age as the only input: Age can be a rough simplification, but it cannot replace time horizon, objectives, liquidity needs, existing holdings, and risk capacity.

- Counting positions without checking weights: The number of holdings matters less than how much exposure each holding creates.

Example: When a Portfolio Looks More Diversified Than It Is

A portfolio may hold several broad funds and appear diversified because the account has many line items. A closer holdings review may show that the largest positions inside those funds repeat exposure to the same group of large companies or the same sector.

In that situation, the stated allocation and the actual exposure are not identical. The portfolio may look balanced by fund count, while its real behavior is still shaped by a smaller set of repeated exposures. The useful check is to read allocation through holdings and weights, not only through investment labels.

Strategic and Tactical Asset Allocation

Strategic asset allocation usually refers to a longer-term target mix. Tactical asset allocation usually refers to shorter-term changes around that mix. The distinction can be useful, but it should not turn asset allocation into a market-timing claim.

For a basic portfolio-construction view, the more important question is whether the portfolio’s current exposures match the investor’s objectives, constraints, time horizon, and risk capacity. Tactical changes can add complexity if they are not tied to a clear process.

Limits of Asset Allocation

Asset allocation can shape portfolio exposure, but it cannot remove uncertainty. A portfolio can still lose value, suffer volatility, or experience drawdown risk even when the allocation looks reasonable.

Allocation also does not replace company analysis, fund analysis, valuation work, liquidity review, or risk review. A weak investment does not become strong simply because it fits a category. A category label is only a starting point for understanding exposure.

Age-based rules and model portfolios can be useful as simple references, but they are too broad to resolve every investor’s situation. Time horizon, liquidity needs, income needs, existing assets, risk capacity, tax constraints, and behavior under stress can all change the interpretation.

Related Portfolio Concepts

Concentration helps identify whether risk is clustered in a few holdings, sectors, or factors. Diversification focuses on how widely risk is spread across or inside the allocation. Drawdown shows how much a portfolio can decline from a prior peak. The number of holdings can help frame portfolio breadth, but only after weights and overlap are understood.

Asset Allocation FAQ

Is asset allocation the same as diversification?

No. Asset allocation describes how a portfolio is divided across asset classes and exposures. Diversification describes how risk is spread within or across those exposures.

Does asset allocation guarantee lower risk?

No. Asset allocation can shape risk exposure, but it cannot eliminate losses, guarantee returns, or prevent drawdowns.

Is asset allocation only based on age?

No. Age can be one rough input, but asset allocation also depends on time horizon, risk capacity, objectives, liquidity needs, existing exposure, and rebalancing rules.