Portfolio rebalancing is not just a fixed calendar habit, an equal-weighting rule, or an automatic instruction to sell what has risen and buy what has lagged. It is the process of checking whether portfolio weights still match the intended exposure structure, then deciding whether any adjustment is justified after costs, taxes, liquidity, cash needs, and risk boundaries are considered.

A rebalance review starts with weights, not with share count. The important question is whether the portfolio still behaves like the portfolio that was originally intended. Large price moves, cash additions, withdrawals, dividends, fund overlap, or concentrated positions can change that behavior even when the list of holdings looks unchanged.

Key Points

- Portfolio rebalancing is based on portfolio weights and exposure, not the number of holdings.

- Weights can drift because prices move, cash enters or leaves the portfolio, income is reinvested, or the intended allocation changes.

- A target-versus-current comparison identifies drift, but it does not automatically justify action.

- Hidden overlap, concentration, transaction costs, taxes, liquidity, cash needs, and risk capacity can change the interpretation.

- No single schedule, percentage band, or rebalancing method applies to every portfolio.

What Portfolio Rebalancing Means

Portfolio rebalancing means comparing portfolio weights with the intended allocation, role, or exposure plan, then deciding whether the difference is meaningful enough to review or adjust. The adjustment can involve adding, trimming, redirecting cash flows, or doing nothing if the drift is not material within the investor’s rules and constraints.

The first comparison is usually between target weight and current weight. That comparison is only a starting point. The same weight can mean different things depending on the portfolio base, account type, holding overlap, liquidity, taxes, time horizon, and risk capacity.

How Portfolio Weights Drift

Portfolio weights drift when different parts of the portfolio change at different speeds. If one sleeve rises faster than the rest, its percentage of the portfolio increases. If one position falls, receives no new cash, or is diluted by new contributions elsewhere, its percentage falls. The holdings may be the same, but the exposure mix is different.

The denominator matters. A position can be 8% of the whole portfolio, 15% of one account, 25% of an equity sleeve, or 40% of a smaller strategy bucket. Each reading answers a different question. Rebalancing only becomes meaningful after the portfolio base has been defined.

The intended mix usually comes from asset allocation, but rebalancing is the maintenance layer. Allocation defines the intended structure; rebalancing checks whether the portfolio still resembles that structure after market movement, cash flows, and portfolio changes.

Portfolio Rebalancing Example

A simple example can show the mechanics without turning the result into a recommendation. The numbers below describe drift only. They do not imply that any specific adjustment should be made.

| Exposure / sleeve | Intended weight | Current weight | What changed | Interpretation note |

|---|---|---|---|---|

| Equity sleeve | 60% | 68% | Equities rose faster than the rest of the portfolio | Equity influence is higher than intended |

| Bond sleeve | 30% | 24% | The bond sleeve became a smaller share of the portfolio | The intended stabilizing role may be smaller than planned |

| Cash sleeve | 10% | 8% | Cash became smaller after other assets moved | Liquidity should be checked against near-term needs |

The table identifies drift, not a required trade. A portfolio could be reviewed because the equity sleeve is above its intended weight, but the action decision still depends on costs, taxes, liquidity, account rules, cash needs, and whether the original structure still fits the investor’s situation.

What To Check Before Interpreting A Rebalancing Result

A useful rebalancing review separates the measurement from the decision. The measurement asks what changed. The decision asks whether the change matters enough to justify action.

| Input | Question to ask | Why it changes the reading |

|---|---|---|

| Portfolio base / denominator | Is the review based on the whole portfolio, one account, one sleeve, or one strategy bucket? | The same holding can look small or large depending on the base used. |

| Target role | What role was the holding or sleeve supposed to play? | A growth sleeve, cash reserve, income sleeve, and defensive sleeve are not interpreted the same way. |

| Current weight | How far has the current weight moved from the intended weight? | Weight drift shows whether the portfolio’s influence has changed. |

| Overlap | Do funds, ETFs, sectors, styles, or individual holdings repeat the same exposure? | Multiple holdings can still point to the same underlying risk. |

| Concentration | Has one holding, sector, factor, or theme become more influential than intended? | Drift can create concentrated exposure even when the portfolio still contains many holdings. |

| Time horizon | Is the intended horizon still the same? | A portfolio built for long-term compounding is reviewed differently from a portfolio with near-term cash needs. |

| Liquidity and cash needs | Could cash needs or market liquidity affect whether an adjustment is sensible? | A clean weight calculation may still be impractical if liquidity is limited or cash is needed soon. |

| Cost and tax friction | Would action create meaningful costs, taxable events, or avoidable turnover? | Rebalancing can solve one exposure issue while creating another cost or tax issue. |

| Review rule | Is the review based on a calendar, a drift band, a cash-flow event, or a portfolio change? | The review trigger should not be confused with an automatic action trigger. |

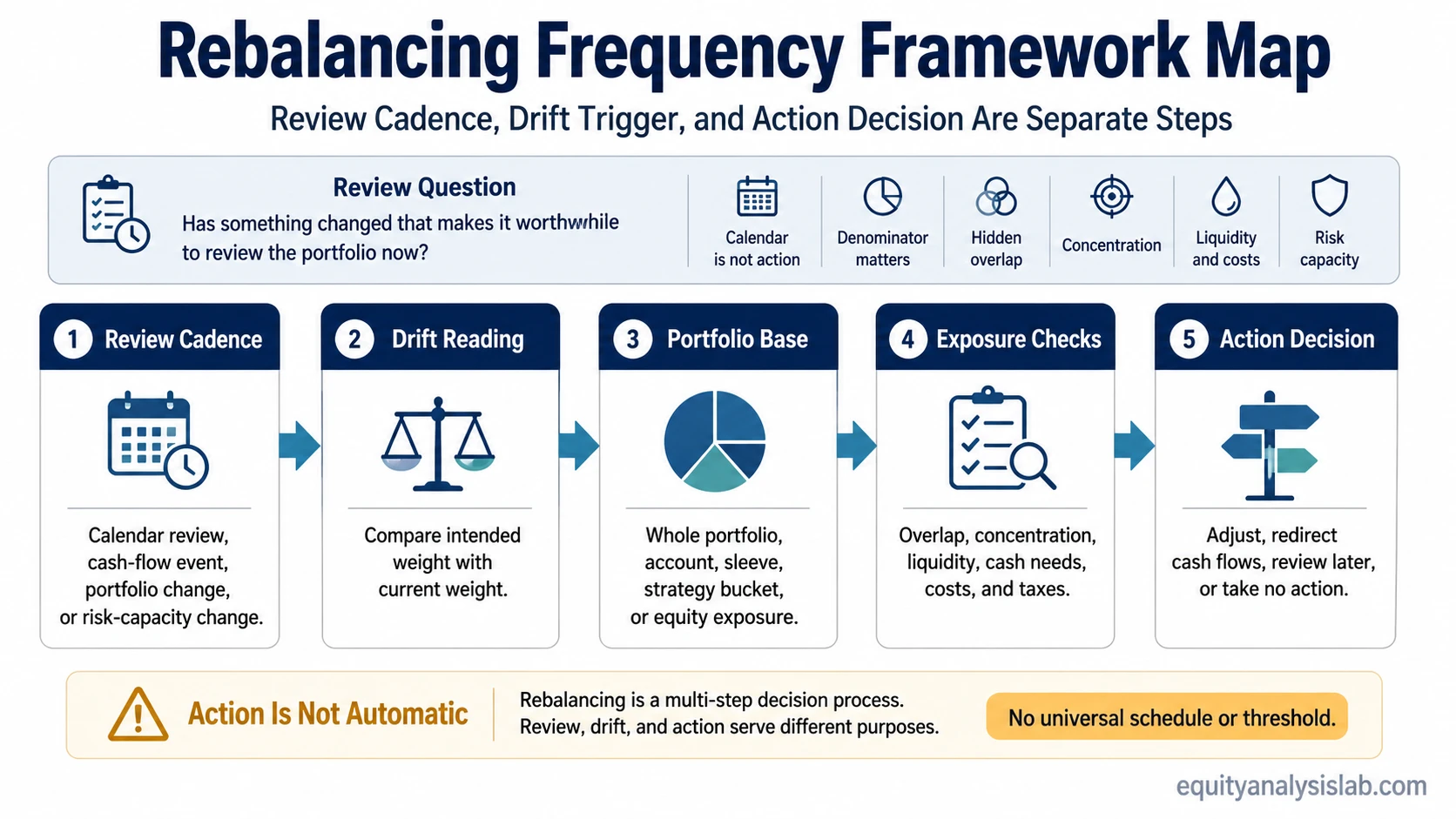

Review Cadence Versus Action Trigger

A review cadence is the moment when the portfolio is checked. An action trigger is the condition that makes an adjustment worth considering. Confusing the two can make rebalancing too mechanical.

Calendar rebalancing checks the portfolio on a set schedule. Threshold rebalancing checks whether weights have moved beyond a defined band. A hybrid approach combines both. These methods describe how drift is noticed; they do not prove that selling, buying, or reallocating is always justified.

New cash can also change the decision. A portfolio may be brought closer to intended weights by directing contributions, dividends, or withdrawals rather than selling existing holdings. That still belongs to rebalancing logic because weights are being managed, but it may create a different cost, tax, and liquidity profile.

What Portfolio Rebalancing Does Not Tell You

Rebalancing does not say that a portfolio should always return to an old target. It does not prove that a rising holding is overvalued, that a falling holding is attractive, or that any fixed threshold is suitable for every investor.

The review can show that exposure has changed. It cannot decide by itself whether the original allocation is still appropriate, whether taxes justify delaying action, whether liquidity is sufficient, or whether the investor’s objectives and risk capacity have changed.

Portfolio Rebalancing Strategies And Methods

The word “strategy” can make rebalancing sound like a performance technique, but the safer interpretation is method selection. A method describes how the review is organized; it does not promise a better result.

| Method | How it works | Main limitation |

|---|---|---|

| Calendar review | The portfolio is checked at a scheduled interval. | The schedule may miss large drift between review dates or trigger a review when drift is small. |

| Threshold review | The portfolio is checked against a defined drift band or tolerance range. | The threshold can be too sensitive or too wide if costs, taxes, liquidity, or risk capacity are ignored. |

| Cash-flow-based review | New contributions, dividends, or withdrawals are used to move weights closer to the intended structure. | Cash flows may be too small, irregular, or unavailable when the drift is large. |

| Hybrid review | A schedule is combined with drift checks or cash-flow events. | More inputs can improve awareness, but they can also make the rule more complex. |

These methods are review structures, not universal instructions. Their usefulness depends on the portfolio base, account type, friction, liquidity, investor objectives, and the reason the original weights existed.

How Often To Rebalance A Portfolio

How often to rebalance depends on whether “rebalance” means review or action. A portfolio can be reviewed regularly without being changed every time. The review frequency can be calendar-based, event-based, drift-based, or linked to cash flows.

A more useful question is whether the portfolio’s current exposures still match the intended structure. If they do, no action may be needed. If they do not, the next step is to check whether the difference is large enough to matter after costs, taxes, liquidity, cash needs, and risk capacity are considered.

Related Portfolio Concepts

Rebalancing belongs inside a broader portfolio construction process. It should not be read as a standalone rule detached from allocation, holding count, concentration, and diversification.

Asset allocation defines the intended structure. Holding count affects how many holdings are needed for the portfolio’s purpose. Rebalancing starts after the holdings and intended exposure structure already exist.

Concentrated exposure is especially important when one winner, one fund, or one theme begins driving too much of the portfolio’s behavior. Rebalancing can be one possible response, but the first step is recognizing the influence.

Exposure spread and overlap matter because a portfolio can hold many lines while still depending on the same underlying drivers. Weight drift and overlap should be read together, not as separate checklist items.

Portfolio Rebalancing FAQ

Is portfolio rebalancing the same as asset allocation?

No. Asset allocation defines the intended mix of assets, sleeves, or portfolio roles. Portfolio rebalancing checks whether current weights still match that intended mix after prices, cash flows, income, and portfolio changes have altered the actual exposure.

Does portfolio rebalancing always require selling investments?

No. A rebalance review can lead to selling, buying, redirecting new cash, reinvesting income differently, withdrawing from one sleeve, or taking no action. The review identifies drift; the action decision depends on the investor’s rules, constraints, costs, liquidity, and risk boundaries.

Is a fixed rebalancing schedule required?

No universal schedule applies to every portfolio. A schedule can be one review method, but drift bands, cash-flow events, portfolio changes, liquidity needs, and risk-capacity changes can also affect when a review is useful.