Diversification is a portfolio construction process that spreads exposure across different holdings, asset classes, sectors, geographies, or risk drivers so one position or shared risk source does not dominate the portfolio.

In investing, the test is not only how many holdings a portfolio owns, but whether those holdings actually respond to different risks. A portfolio can look diversified on the surface while still depending heavily on the same sector, factor, currency, business model, or top-weighted position.

What Diversification Means in Investing

Diversification means spreading portfolio exposure so the outcome does not rely too heavily on one company, one industry, one asset class, one geography, or one dominant economic driver.

For an investor, diversification is a way to reduce dependence on a single source of risk. It does not make a portfolio risk-free. It changes where the risk comes from, how concentrated that risk is, and how much one adverse event can affect the whole portfolio.

The concept applies at several levels. A portfolio may diversify across asset classes, across individual securities, across sectors, across countries, across business models, and across sources of return. The useful question is not whether the portfolio has many line items. The useful question is whether the portfolio is exposed to different drivers in a way that fits the investor’s broader risk constraints.

How Diversification Changes Portfolio Exposure

Diversification changes a portfolio by spreading the sources of return and loss. Instead of one position, one sector, or one market condition carrying most of the portfolio outcome, the portfolio depends on a wider set of drivers.

At the broadest level, diversification may involve different asset classes. That boundary connects to asset allocation, which is the decision about how portfolio weight is divided across broad categories such as stocks, bonds, cash, or other assets.

Within stocks, diversification can mean owning companies with different earnings drivers, margins, capital needs, customer bases, geographies, balance-sheet sensitivity, or valuation behavior. Two companies can have different ticker symbols but still react to the same pressure if they depend on similar demand, financing conditions, commodity inputs, or investor sentiment.

Position weights matter as much as the list of holdings. A portfolio with many small positions and one very large position may still depend mainly on the large position. A portfolio can also drift toward a narrower exposure when earlier winners become a much larger share of total value.

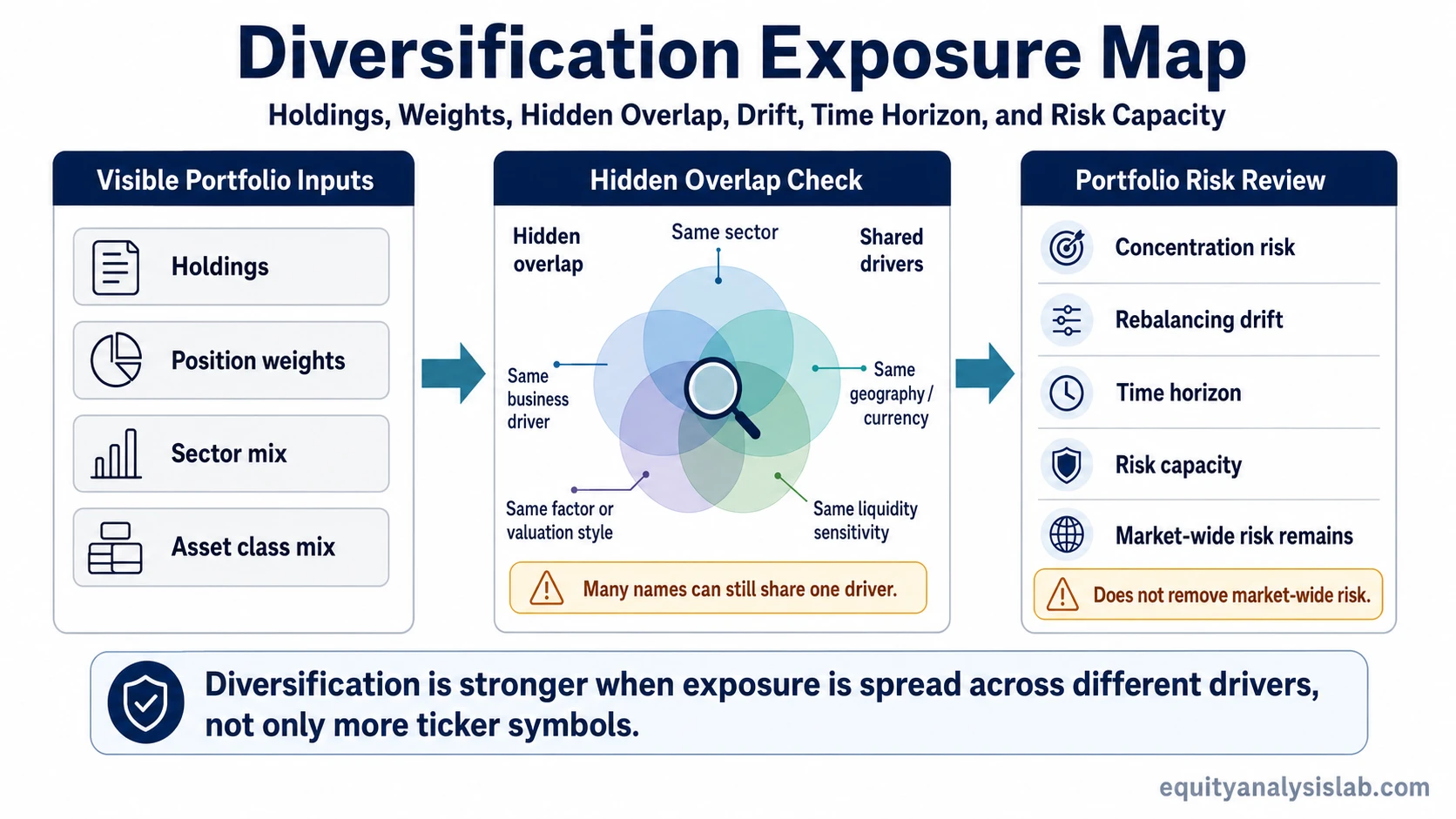

What to Check Before Calling a Portfolio Diversified

A diversified portfolio is easier to evaluate when the review starts with exposure, not with holding count alone. The table below separates visible breadth from the hidden drivers that can still concentrate risk.

| What to check | What it shows | How it can mislead |

|---|---|---|

| Number of holdings | How many separate names appear in the portfolio | Many holdings can still share one dominant driver |

| Position weights | Whether top holdings dominate total exposure | A broad list can still be top-heavy |

| Sector exposure | How much risk comes from one industry group | Different stocks in the same sector may move together |

| Business-model overlap | Whether companies depend on similar revenue or margin drivers | Different company names can still face the same pressure |

| Geography and currency exposure | Which regions, economies, or currencies influence results | A company’s listing country may not match its real economic exposure |

| Factor exposure | Whether holdings lean toward the same style, valuation, size, or sensitivity | Unrelated businesses can still react similarly to interest rates, liquidity, or sentiment |

| Rebalancing drift | Whether portfolio weights have changed over time | Past winners can recreate concentration without a new purchase |

| Time horizon and risk capacity | Whether the exposure fits the investor’s ability to tolerate volatility and losses | Diversification can reduce single-driver dependence, but it cannot remove market-wide decline risk |

Holding count is only a starting point. The more precise question is whether the portfolio has enough independent exposure for its intended role, which is why a separate discussion of how many holdings are enough should not be treated as a universal rule.

False Diversification and Hidden Overlap

False diversification appears when a portfolio has many holdings but those holdings are tied to the same risk source. The portfolio looks broad by name count, but its behavior can still be narrow.

One common version is sector overlap. An investor may own several companies that appear separate, but if all of them depend on the same industry cycle, the same customer demand, or the same financing environment, the portfolio may still carry meaningful concentration risk.

Another version is factor overlap. A portfolio may contain companies from different sectors but still lean heavily toward the same valuation style, growth sensitivity, interest-rate exposure, or liquidity condition. In that case, the hidden common driver can matter more than the visible company labels.

For example, a portfolio may own many stocks across different tickers, but most of those companies may depend on the same consumer cycle, the same funding conditions, or the same high-growth valuation assumptions. If that shared driver weakens, the portfolio may behave less diversified than the holding list suggests.

False diversification can also happen through review limits. A very large number of small positions can become difficult to monitor if the investor cannot clearly track thesis quality, business deterioration, weight drift, and position role. More holdings do not automatically create clearer risk control.

Diversification vs Related Portfolio Concepts

Diversification is connected to several portfolio concepts, but it should not replace them. Each concept answers a different question about portfolio structure.

| Concept | Main question | How it differs from diversification |

|---|---|---|

| Diversification | Are risks spread across different drivers? | Focuses on whether portfolio exposure is broad or overly dependent on one source |

| Asset allocation | How is capital divided across broad asset categories? | Sets broad category weights, while diversification checks how concentrated the resulting exposure remains |

| Concentration | How dependent is the portfolio on one holding, sector, or driver? | Describes the opposite side of the same risk-spread question |

| Position sizing | How large is each holding relative to the portfolio? | Controls weight at the holding level, while diversification checks how those weights interact |

| Drawdown | How far can the portfolio fall from a previous high? | Measures decline behavior, while diversification influences what may drive that decline |

| Rebalancing | Should portfolio weights be reset after they drift? | Manages changes in exposure after prices move, rather than defining diversification by itself |

Limits of Diversification

Diversification can reduce dependence on one position or risk driver, but it cannot remove market-wide risk, guarantee returns, or prevent losses.

Some risks are specific to a company, sector, business model, or balance sheet. Diversification can reduce the impact of those risks when exposure is spread across different drivers. Other risks affect broad markets at the same time, including recessions, liquidity stress, inflation shocks, interest-rate repricing, or broad valuation compression.

During broad market declines, diversified portfolios can still fall. The size, speed, and source of a portfolio decline connect more directly to portfolio decline behavior than to diversification alone.

Diversification also does not fix weak analysis. A portfolio made of many poor theses is not stronger simply because the positions are spread out. Diversification helps organize exposure, but it does not replace valuation work, business-quality review, thesis monitoring, or risk-capacity judgment.

Related Portfolio Concepts

Diversification is easiest to use when it is separated from nearby portfolio decisions. Asset allocation sets the broad category mix. Concentration shows where one exposure may dominate. Drawdown describes how losses appear after portfolio value declines. Holding count helps frame review capacity, but it does not prove that exposure is genuinely spread.

| Related concept | Use when the question is about |

|---|---|

| Asset allocation | How capital is divided across broad asset categories |

| Portfolio concentration | Whether one holding, sector, or driver dominates the portfolio |

| Drawdown | How far portfolio value can fall from a prior high |

| How many stocks should you own | How holding count interacts with review capacity and exposure spread |

FAQ

What is diversification in investing?

Diversification in investing means spreading portfolio exposure across different holdings, asset classes, sectors, geographies, or risk drivers so one position or shared risk source does not dominate the portfolio.

Does diversification guarantee profit?

No. Diversification can reduce dependence on a single position or risk driver, but it cannot guarantee profit, prevent losses, or remove market-wide risk.

Can a portfolio have many holdings and still not be diversified?

Yes. A portfolio can own many holdings while still depending on the same sector, factor, geography, business model, or top-weighted position. Holding count alone does not prove that exposure is spread across different risks.

How is diversification different from asset allocation?

Asset allocation divides capital across broad asset categories, while diversification checks whether exposure is actually spread across different drivers inside and across those categories.