A concentrated portfolio is not defined only by how many holdings it contains. It is a portfolio where one large position, a small group of holdings, or a cluster of related exposures drives a meaningful share of portfolio behavior.

Concentration can be deliberate or accidental. It can reflect a focused research process, a legacy holding, a position that grew over time, or several holdings that depend on the same business driver. The key question is not whether concentration is automatically good or bad. The useful question is what actually controls the portfolio’s exposure.

Key Points

- A concentrated portfolio is driven by exposure, not just by the visible number of holdings.

- One large position can dominate results even when the portfolio contains many smaller positions.

- Several holdings can create hidden concentration if they depend on the same sector, factor, customer base, valuation driver, or economic cycle.

- Concentration can be intentional, accidental, or created by portfolio drift after a holding appreciates.

- Drawdown tolerance and review discipline matter because concentrated exposure can make portfolio behavior less forgiving.

What a Concentrated Portfolio Means

Definition: A concentrated portfolio is a portfolio where a limited set of positions or related exposures has an unusually large influence on total portfolio behavior. The concentration may come from one dominant holding, a small group of top-weighted holdings, or several holdings that share the same underlying risk driver.

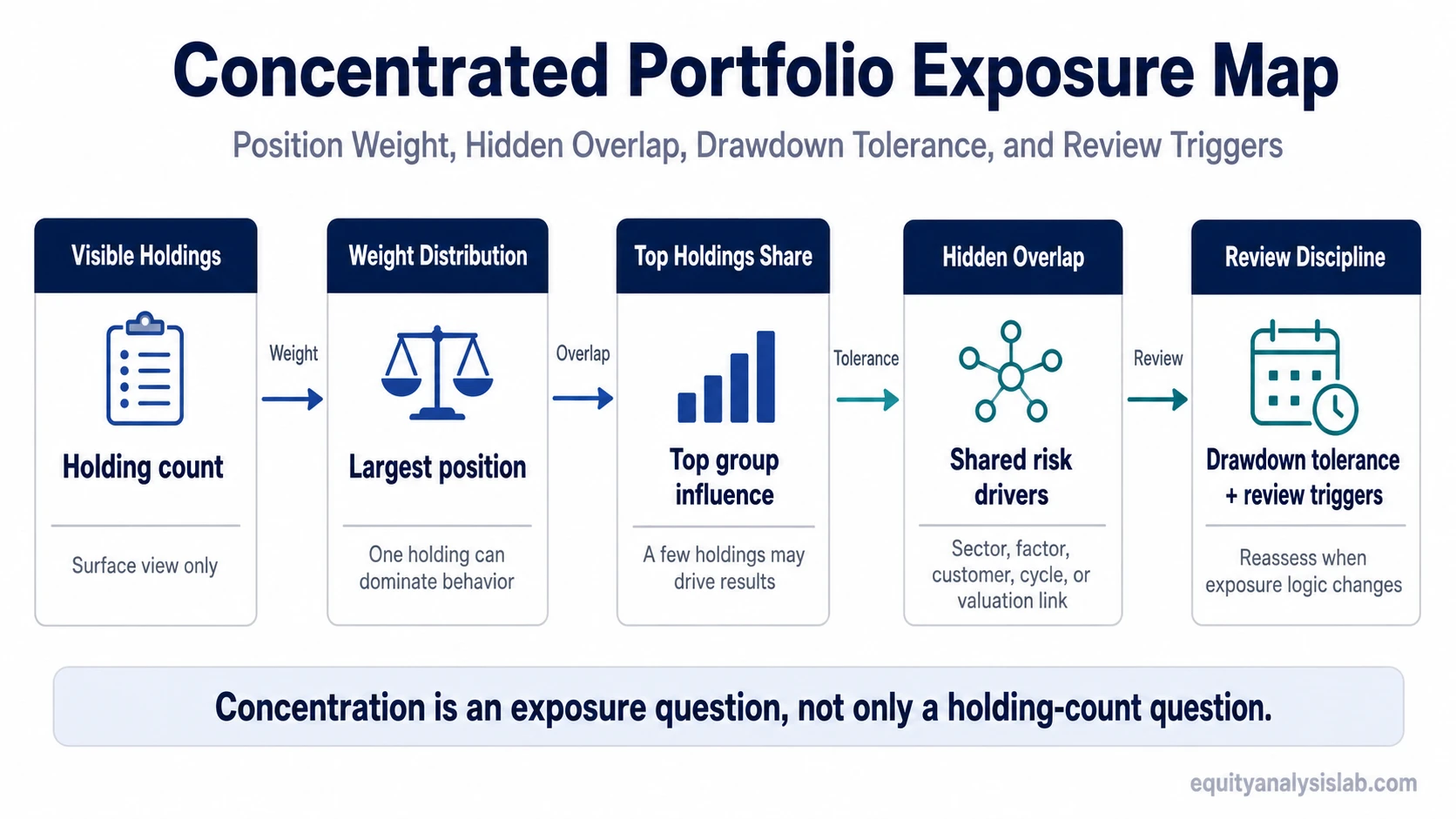

Holding count gives only the surface view. A portfolio with five holdings is visibly concentrated, but a portfolio with twenty holdings can also be concentrated if most of the value depends on similar companies, similar valuation assumptions, or the same economic condition.

The concept is about exposure. If the largest holdings would likely rise, fall, disappoint, or reprice for similar reasons, the portfolio may behave as one narrow cluster even when the holdings look separate by name.

How to Identify Portfolio Concentration

Concentration is easier to judge when the observable inputs are separated. A single number rarely explains the full picture. Holding count, position weight, top-holdings share, overlap, time horizon, and review rules each answer a different question.

| Observable | What it tells the investor | Common misread |

|---|---|---|

| Number of holdings | Shows the visible breadth of the portfolio. | Assuming more holdings automatically means the portfolio is diversified. |

| Largest position weight | Shows how much one holding can influence total portfolio behavior. | Ignoring a position that grew large after strong price appreciation. |

| Top-five or top-ten weight | Shows whether a small group controls most of the portfolio. | Looking only at the total number of holdings instead of the weight distribution. |

| Sector or industry overlap | Shows whether the portfolio depends heavily on one part of the market. | Treating different tickers as separate risks when they share the same cycle. |

| Business-driver overlap | Shows whether revenue, margins, demand, or valuation depend on similar forces. | Missing hidden overlap across companies that appear unrelated at first glance. |

| Factor or valuation overlap | Shows whether holdings may reprice together when rates, growth expectations, or risk appetite change. | Assuming different businesses cannot fall together because their products differ. |

| Time horizon | Shows whether the investor can wait through volatility and thesis development. | Holding concentrated exposure with a time horizon too short for the original thesis. |

| Liquidity needs | Shows whether cash may be needed before the thesis has time to develop. | Confusing conviction with flexibility when future cash needs are uncertain. |

| Review rule | Shows what would trigger reassessment before emotion or price movement dominates the decision. | Reviewing only after a large decline instead of after the exposure logic changes. |

Concentration, Diversification, and Asset Allocation

Concentration is related to asset allocation, but the two ideas are not the same. Asset allocation describes how capital is spread across broad categories such as stocks, bonds, cash, sectors, regions, or other asset groups. Concentration describes how much portfolio behavior is controlled by a narrow set of holdings or exposures.

Concentration is also different from diversification. Diversification asks whether risks are spread across different drivers. Concentration asks whether a narrow set of drivers still controls the outcome.

A portfolio can be diversified across many names but concentrated in one broad exposure. It can also be concentrated in a few holdings that have very different business drivers. The difference matters because the risk is not always visible from the holding list alone.

Hidden Overlap and False Diversification

Hidden concentration appears when separate holdings are more connected than they look. Two companies may operate in different industries but still depend on the same interest-rate environment, the same end customer, the same commodity input, the same valuation multiple, or the same funding condition.

That overlap can make a portfolio behave as though it has fewer independent exposures than the holding count suggests. The investor may think the portfolio is spread across many ideas, while the actual exposure is tied to one dominant assumption.

Limitation: Hidden overlap is not always obvious from sector labels. A portfolio can contain different sectors and still be concentrated if the holdings share the same growth expectations, financing sensitivity, geographic exposure, or valuation risk.

Why Drawdown Tolerance Matters

Concentration can make a portfolio decline from a prior peak more difficult to tolerate because fewer exposures may be available to offset weakness in the dominant position or cluster. The issue is not only the size of the decline. It is whether the investor can keep evaluating the thesis clearly while the largest exposure is under pressure.

Drawdown tolerance is not a promise that a concentrated portfolio will recover. It is a practical constraint. If the investor cannot tolerate the likely range of volatility, the position may force emotional decisions before the original thesis can be evaluated properly.

That is why review rules matter. A concentrated portfolio needs a clear reason to reassess exposure when the business case, valuation logic, risk driver, or portfolio role changes. Without that rule, the investor may react only after price movement has already become painful.

When Concentration Is Intentional or Accidental

Intentional concentration usually comes from a focused investment process. The investor may choose to hold fewer companies because each position has been researched deeply, or because the investor wants the portfolio to reflect only the highest-conviction ideas. That does not make the portfolio automatically safer or better. It only means the concentration is deliberate.

Accidental concentration can happen when a position grows faster than the rest of the portfolio, when several holdings become exposed to the same driver, or when old portfolio choices are never reviewed. In that case, the investor may be taking concentrated risk without having made an explicit decision to do so.

The distinction matters because intentional concentration can be monitored through thesis quality, exposure weight, and review discipline. Accidental concentration first requires detection. The investor has to see the exposure before it can be managed or reassessed.

Holding Count Is Only One Part of the Question

The question is not only the number of stocks in a portfolio. A holding count can help describe surface structure, but it does not show how much each position weighs, how related the holdings are, or whether several positions depend on the same driver.

A concentrated portfolio can be understood more clearly by asking three questions. Which holdings drive the largest share of results? Which holdings would likely move together for similar reasons? What would cause the investor to review or reduce the exposure?

Those questions keep the focus on exposure rather than labels. The portfolio may still be concentrated, but the investor has a clearer view of where that concentration actually comes from.

Related Concepts

Concentration sits inside a broader portfolio-construction process. It connects to diversification, asset allocation, position sizing, drawdown tolerance, and rebalancing because each concept helps describe a different part of portfolio exposure.

For a focused portfolio, the most useful review is usually not a single rule. It is a combined view of position weight, overlap, risk tolerance, liquidity needs, and the reason each holding still belongs in the portfolio.

FAQ

What is a concentrated portfolio?

A concentrated portfolio is a portfolio where a small number of positions or related exposures has an unusually large influence on total portfolio behavior. The concentration can come from one dominant holding, several top-weighted holdings, or hidden overlap across related risk drivers.

Is a concentrated portfolio the same as owning only a few stocks?

No. A small number of holdings is one form of concentration, but a portfolio with many holdings can also be concentrated if those holdings depend on the same sector, factor, business driver, or valuation environment.

Is portfolio concentration always bad?

No. Concentration can be deliberate or accidental. The risk depends on whether the exposure is understood, whether the largest drivers are visible, and whether the investor has a clear review rule when conditions change.

How can hidden concentration appear?

Hidden concentration can appear when different holdings share the same economic driver, customer base, geography, sector, business model, or valuation factor. The portfolio may look diversified by name while still reacting like one narrow exposure cluster.