Position sizing is the process of deciding how much capital or portfolio exposure belongs in a single position. In a portfolio, it controls how much one holding can affect results, risk, and behavior, but it does not prove that the investment idea is correct.

Position sizing definition: Position sizing means setting the size of a holding as a share of the portfolio, usually by considering portfolio value, position weight, downside tolerance, liquidity, overlap with other holdings, time horizon, and the rule for adjusting the position later.

Position sizing sits inside portfolio construction and risk management. It is different from stock selection. A strong idea can still be oversized, and a small position can still be a weak idea. The sizing decision answers a narrower question: how much exposure should this position be allowed to carry?

Key points about position sizing

- Position sizing controls exposure, not investment quality.

- A position can be too large even when the thesis sounds reasonable.

- Portfolio weight matters more than the number of holdings alone.

- Overlap can make several positions behave like one larger exposure.

- Position sizes drift after price moves, so a sizing rule usually connects to rebalancing.

What position sizing means in a portfolio

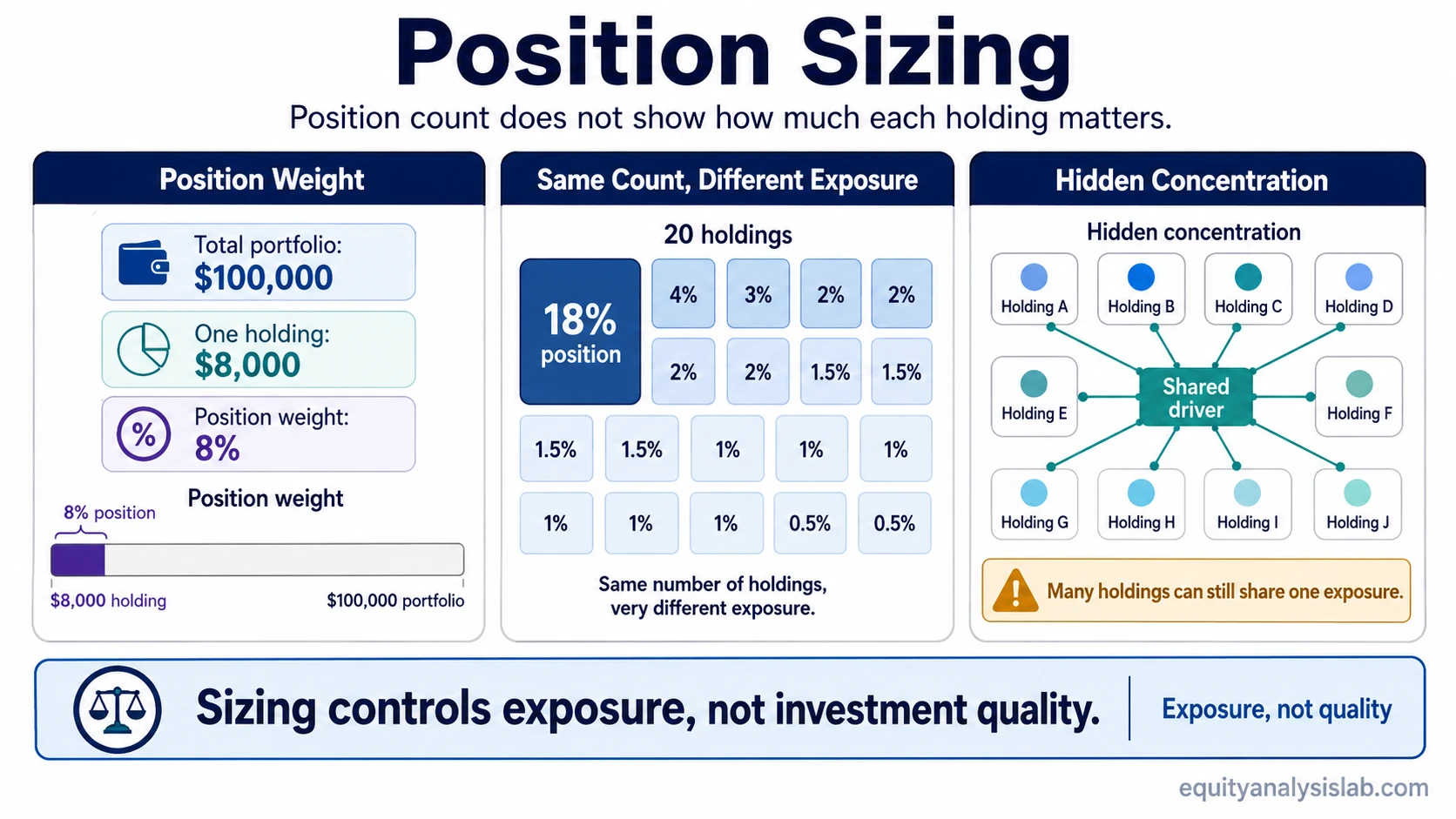

In portfolio terms, a position size is usually expressed as a percentage of total portfolio value. If a portfolio is worth $100,000 and one holding is worth $8,000, that holding is an 8% position. The simple weight formula is:

Position weight = position value ÷ total portfolio value

That percentage matters because it shows how much the portfolio depends on one holding. A 2% position and a 20% position can reflect the same investment idea, but they create very different portfolio impact if the price moves sharply, the thesis changes, or liquidity becomes limited.

Position sizing also affects how the investor reacts. A position that is too large for the investor’s risk capacity can create pressure to sell at the wrong time, ignore new evidence, or treat normal volatility as a crisis. A position that is too small may have little effect even if the idea works.

Position sizing inputs

A useful position size is not based on one input alone. It usually comes from combining portfolio weight, downside tolerance, overlap, liquidity, time horizon, and the rule for when the position should be adjusted.

| Input | What it controls | Why it matters |

|---|---|---|

| Portfolio size | Base for exposure | Determines how large a weight is in total portfolio terms. |

| Position weight | Direct allocation | Shows how much one holding can affect the portfolio. |

| Risk capacity | Loss tolerance boundary | Prevents one position from exceeding the investor’s ability to absorb loss. |

| Overlap | Shared drivers | Reveals when separate holdings behave like one concentrated exposure. |

| Time horizon | Holding-period context | Affects how much volatility the investor may need to tolerate. |

| Liquidity | Exit and adjustment flexibility | Matters when a position cannot be reduced easily. |

| Rebalancing rule | Ongoing size discipline | Prevents winners or volatile holdings from quietly becoming too large. |

The table also shows why position sizing is not the same as diversification. Diversification asks how exposure is spread across different holdings and drivers. Position sizing asks how much each exposure is allowed to count.

Simple position sizing example

Imagine a portfolio with 20 holdings. On the surface, the stock count may look broad. But one position is 18% of the portfolio, and several other holdings depend on the same business driver. The portfolio has many line items, but the actual exposure may still be concentrated.

Position sizing asks whether the 18% weight fits the investor’s risk capacity, time horizon, liquidity needs, and rebalancing rule. It also asks whether the related holdings should be viewed separately or as part of one larger exposure.

This is why the question is not only how many stocks should you own. A portfolio with fewer holdings can be more balanced than a larger portfolio if the larger portfolio has repeated exposure to the same driver.

Basic position sizing formula

The basic portfolio-weight formula is simple: divide the position value by the total portfolio value. That gives the current weight of the position.

Example formula: $8,000 position value ÷ $100,000 portfolio value = 8% position weight.

The formula is only the starting point. The more important question is whether that weight is appropriate for the position’s downside profile, liquidity, overlap, and role in the portfolio. A stable core holding, a cyclical holding, and a speculative holding should not automatically receive the same size just because the formula can measure them the same way.

For a fuller workflow that turns portfolio value, target weight, and risk boundaries into a sizing process, use how to size a stock position.

Common mistakes and limitations

Position sizing does not make a weak investment high quality. A smaller position can limit portfolio impact, but it does not fix poor business quality, weak cash flow, fragile thesis logic, or unsupported assumptions.

A speculative holding should not be sized like a core holding when the downside profile is meaningfully different. If a position has severe downside risk, limited liquidity, or uncertain thesis durability, the size should reflect those constraints instead of relying on optimism.

An exit rule does not fully define risk if the position is too large for the portfolio to absorb. Even when an investor has a plan to reduce or exit a position, the size can still create emotional and financial pressure if the loss would be intolerable.

Many holdings can still create hidden concentration. Several positions may depend on the same sector, customer type, commodity, rate environment, funding condition, or valuation driver. In that case, the real exposure can be larger than any single position weight suggests.

Position size changes after price moves. A winner can become too large without any new purchase, and a volatile holding can change the portfolio’s risk profile over time. That is why sizing and rebalancing are connected.

How position sizing differs from nearby concepts

Position sizing is closely related to several portfolio concepts, but it does not replace them.

| Concept | Main question | Difference from position sizing |

|---|---|---|

| Position sizing | How much exposure should one position carry? | Sets the size of a holding relative to the portfolio. |

| Diversification | How spread out are the portfolio’s risks? | Focuses on distribution across holdings and drivers. |

| Rebalancing | When should position weights be adjusted? | Maintains or resets sizes after prices move. |

| Drawdown | How far has the portfolio fallen from a prior peak? | Measures an observed decline after it happens. |

| Stock count | How many holdings are in the portfolio? | Counts holdings, but does not show how much each one matters. |

The practical distinction is that position sizing is an allocation decision made before or during ownership. Drawdown is an observed outcome. Diversification is about spread. Rebalancing is the process that keeps position sizes from drifting too far away from the intended structure.

FAQ

What is position sizing?

Position sizing is the process of deciding how much capital or portfolio exposure to allocate to one position. It controls how much that position can affect the overall portfolio.

Is position sizing the same as diversification?

No. Position sizing sets how large each holding is. Diversification looks at how risk is spread across different holdings, sectors, drivers, or asset types.

Does position sizing reduce all investment risk?

No. Position sizing can limit the impact of one position, but it cannot remove business risk, valuation risk, liquidity risk, thesis risk, or market risk.

Why can a portfolio with many holdings still be concentrated?

A portfolio can hold many positions that depend on the same underlying driver. When several holdings behave similarly, the combined exposure can be more concentrated than the stock count suggests.