Capital returns describe how a company sends value back to shareholders, most often through dividends, share repurchases, or a combination of both. The useful question is not simply whether a company returns capital, but which metric best explains the shareholder-return policy being tested.

In company analysis, capital returns sit inside a wider capital allocation decision. Management can reinvest in the business, reduce debt, acquire assets, pay dividends, repurchase shares, or hold cash. Dividends and buybacks are the most visible shareholder-return channels, but they need different metrics because they affect investors in different ways.

In this context, capital returns means shareholder-return analysis, not return-of-capital tax treatment, closed-end fund distribution rules, or the book titled Capital Returns.

Key Points

- Capital returns usually refer to dividends, buybacks, or both.

- The right metric depends on whether the analysis is testing income, payout burden, dividend safety, growth, repurchase intensity, or combined shareholder yield.

- Capital returns can be misleading without funding quality, reinvestment needs, valuation context, dilution, and industry structure.

How to Use Capital Returns in Company Analysis

Capital returns are best read as a decision map. A dividend tells investors that cash is being distributed directly. A buyback tells investors that the company is using cash to reduce shares or offset dilution. A combined shareholder-return view asks whether those actions are meaningful relative to the company’s value, cash generation, and reinvestment needs.

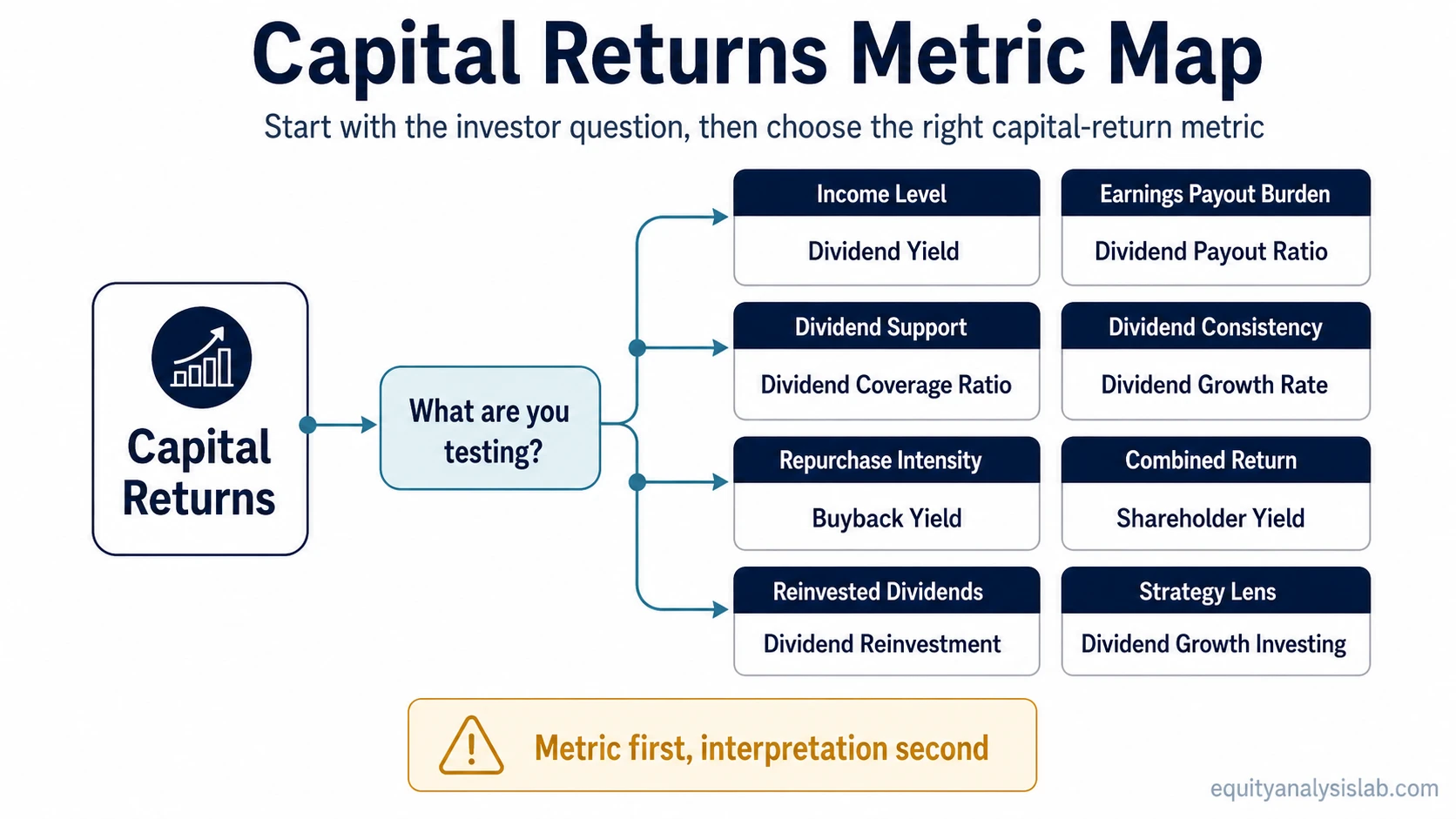

The starting point is the investor question. Income analysis points toward dividend yield. Sustainability analysis points toward payout ratio or dividend coverage. Repurchase-intensity analysis points toward buyback yield. Combined capital-return analysis points toward shareholder yield.

Analysis note: A company can return capital and still make a poor capital allocation decision if the distribution is funded weakly, crowds out better reinvestment, offsets heavy dilution, or occurs at an unattractive valuation.

Choose the Right Capital Return Metric

The same company can look attractive on one capital-return measure and weaker on another, especially when dividends, buybacks, dilution, earnings quality, and cash flow do not point in the same direction.

| Investor question | Metric or concept | Why it fits |

|---|---|---|

| How much capital is returned through buybacks? | buyback yield | Measures repurchase intensity relative to company value. |

| How much income does the stock pay? | dividend yield | Connects dividend payments to share price. |

| Is the dividend too large relative to earnings? | dividend payout ratio | Shows how much profit is being paid out as dividends. |

| Is the dividend covered by earnings or cash flow? | dividend coverage ratio | Tests whether the dividend is supported by the company’s financial base. |

| Is the dividend stream growing? | dividend growth rate | Shows the direction and consistency of dividend increases. |

| What is the combined return through dividends and buybacks? | shareholder yield | Combines multiple shareholder-return channels in one view. |

| What happens when dividends are reinvested? | dividend reinvestment | Explains how received dividends can be used to buy more shares. |

| How do investors use dividend growth as a strategy? | dividend growth investing | Moves from a dividend metric to a broader investing approach. |

Dividends vs Buybacks in Capital Allocation

Dividends and buybacks are both ways to return capital, but they do not communicate the same thing. A dividend is a direct cash payment to shareholders. A buyback uses company cash to repurchase shares, which can reduce share count and influence per-share metrics when the repurchase is large enough and not offset by new share issuance.

Dividends are usually easier to see because the payment is explicit. Buybacks require more interpretation because the result depends on repurchase price, dilution, share count changes, balance-sheet impact, and whether the company had better uses for the cash.

Dividend question: How much cash is being paid to shareholders, and can the company support that payment?

Buyback question: How much stock is being repurchased, and does the repurchase improve per-share economics after dilution, valuation, and cash needs are considered?

Metric Selection Logic

Capital-return analysis becomes cleaner when each metric is used for one job. Dividend yield measures income relative to price, not dividend safety. Payout ratio measures the burden on earnings, not total shareholder return. Dividend coverage focuses on support for the dividend, not the attractiveness of the stock. Buyback yield measures repurchase intensity, not whether the repurchase price was sensible.

Shareholder yield is broader because it combines dividends and buybacks. That makes it useful for comparing total shareholder-return policy, but it still needs context. A high combined yield may come from a shrinking business, unusually high cash generation, a one-time balance-sheet decision, or repurchases that mainly offset dilution.

| What is being tested | Metric family | Interpretation caution |

|---|---|---|

| Income level | Dividend yield | A high yield can reflect a falling share price, not only a generous dividend. |

| Payout burden | Dividend payout ratio | Earnings can be volatile or non-cash, so payout quality needs context. |

| Dividend support | Dividend coverage | Coverage can weaken if cash flow, debt service, or reinvestment needs change. |

| Dividend growth | Dividend growth rate | Past growth does not guarantee future increases. |

| Repurchase intensity | Buyback yield | Buybacks should be checked against dilution and valuation. |

| Combined shareholder return | Shareholder yield | Combined yield still needs funding, reinvestment, and balance-sheet context. |

Short Example: The Question Changes the Metric

An investor looking at a cash-generative company may ask three different questions. If the question is “how much cash income does the stock provide?”, dividend yield is the starting point. If the question is “can the company afford the dividend?”, dividend coverage or payout ratio is more relevant. If the question is “how much total capital is being returned through dividends and repurchases?”, shareholder yield is the better starting point.

The same capital-return policy can therefore lead to different analysis depending on the investor question. The metric should narrow the question first; interpretation comes after the number is checked against business quality, funding quality, and valuation context.

When Capital Returns Can Mislead

Funding quality: Capital returns are stronger when they are supported by recurring cash generation. They are weaker when they rely heavily on borrowing, asset sales, or temporary cash sources.

Reinvestment needs: A company that underinvests in operations, research, maintenance, or growth may report attractive capital returns while weakening future competitiveness.

Valuation context: Buybacks can be less useful when shares are repurchased at unattractive prices. A high buyback amount does not automatically mean value was created.

Dilution: Repurchases can look large in isolation but have limited impact if they mainly offset stock-based compensation or other new share issuance.

Industry structure: Capital intensity, regulation, cyclicality, and balance-sheet needs can change how much capital a company can safely return.

Measurement base: Numerator, denominator, time period, peer set, and average versus ending balance-sheet values can all change the reading of a capital-return metric.

What to Check Next

Start with the narrowest question. Use dividend yield for income level, payout ratio for earnings burden, dividend coverage for sustainability, dividend growth rate for dividend consistency, buyback yield for repurchase intensity, and shareholder yield for combined shareholder-return policy.

After the correct metric is selected, the next step is interpretation. A number by itself rarely settles the analysis. Capital returns are more useful when they are checked against cash flow, balance-sheet strength, reinvestment needs, dilution, valuation, and the company’s long-term capital allocation record.