Dividend reinvestment means using cash dividends to buy additional shares of the same stock or fund instead of taking the dividend as cash. It can increase share ownership over time, but it says little by itself about whether the dividend is safe, well covered, or attractive at the current valuation.

Definition: Dividend reinvestment is the process of taking a dividend payment and using it to purchase more shares, often automatically through a dividend reinvestment plan, or DRIP.

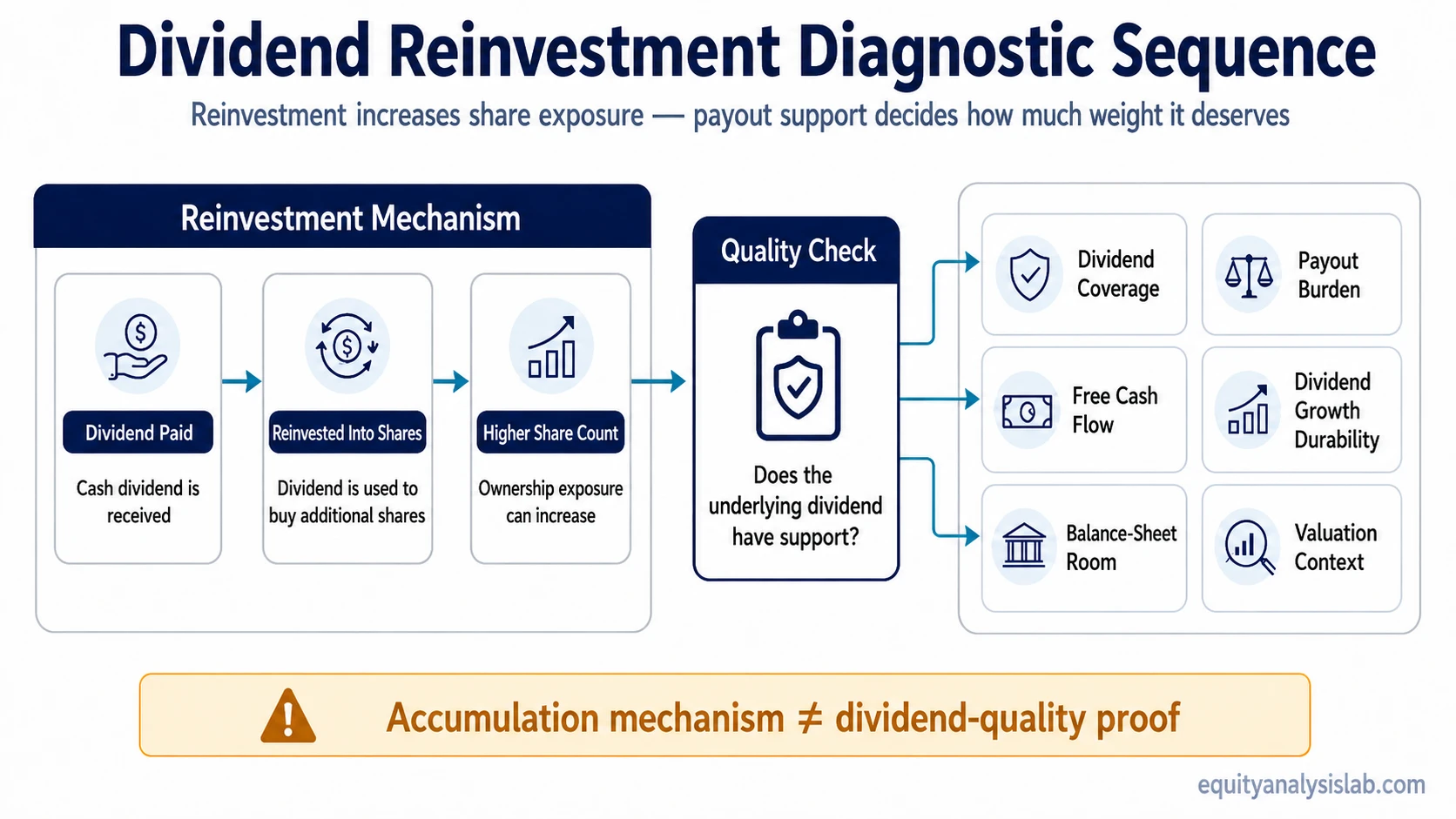

The mechanism is simple: a dividend is paid, the cash is used to buy more shares, and those additional shares may receive future dividends if the company or fund continues paying them. The investor’s ownership base grows, but the quality of that growth still depends on payout support, business durability, and the price at which the reinvestment occurs.

Key Points

- Dividend reinvestment turns cash dividends into additional shares instead of immediate cash income.

- A DRIP can automate the process and may allow fractional-share purchases, depending on the broker, plan, or account structure.

- Reinvestment can increase future dividend exposure if the dividend continues, but it does not make the payout more durable.

- The analytical value of reinvestment depends on dividend coverage, payout burden, free cash flow support, balance-sheet room, and valuation.

What Dividend Reinvestment Means

Dividend reinvestment replaces a cash-receipt decision with an accumulation decision. Instead of receiving the dividend as spendable cash, the investor uses the dividend to buy more shares of the same security or fund.

A dividend reinvestment plan, commonly called a DRIP, is one way this can happen automatically. Some plans and brokerage platforms allow the reinvested amount to buy fractional shares, so the full dividend can be put back into the position even when the dividend amount is smaller than the price of one full share.

The important distinction is that a DRIP is a mechanism, not a quality rating. It changes what happens to the dividend after payment. It does not explain whether the company can keep paying the dividend, whether the distribution is supported by cash flow, or whether the shares are attractively valued.

What Dividend Reinvestment Changes

Dividend reinvestment mainly changes the investor’s share count and exposure path. More shares can create a larger base for future dividend payments if the dividend continues and if those additional shares remain owned.

Illustrative example: An investor owns 100 shares, receives a $100 dividend, and reinvests it at $25 per share. The reinvestment adds 4 shares, increasing the position to 104 shares. Future dividends may be paid on 104 shares, but the result still depends on whether the company maintains the dividend and whether the reinvestment price is reasonable.

This is the link between dividend reinvestment and compounding. The investor may accumulate more shares, and those shares may later generate more dividends. The compounding path weakens if the dividend is reduced, the business deteriorates, or the reinvested capital repeatedly buys shares at unattractive prices.

What Dividend Reinvestment Does Not Prove

Dividend reinvestment does not show whether a payout can be sustained. A company can offer reinvestment while its dividend is becoming harder to support. The reinvestment choice happens after the dividend is paid; it does not explain whether the dividend was funded by durable cash flow, temporary balance-sheet flexibility, or an unsustainable payout policy.

Reinvestment also does not confirm business quality. A higher share count in the same company increases exposure to the same underlying business. If the company’s earnings quality, competitive position, leverage profile, or capital allocation discipline weakens, reinvestment can concentrate exposure to a deteriorating asset.

Limitation: Reinvesting dividends can support accumulation, but it should not replace analysis of the dividend coverage ratio, free cash flow support, and the company’s ability to fund distributions without weakening the business.

Dividend Reinvestment vs Taking Dividends in Cash

The choice between reinvesting and taking dividends in cash changes capital allocation at the investor level. Reinvestment keeps the dividend tied to the same asset. Cash gives the investor flexibility to spend, hold, rebalance, or allocate elsewhere.

| Choice | What changes | What it does not prove |

|---|---|---|

| Reinvest dividends | Share count can increase in the same stock or fund. | The dividend is safe or well covered. |

| Take dividends in cash | Cash remains available for spending, holding, or redeployment. | The original investment is better or worse. |

| Use a DRIP | Reinvestment may happen automatically, sometimes with fractional shares. | The company has stronger fundamentals. |

| Manually reinvest | The investor can choose when and where to redeploy the dividend. | The reinvestment decision will improve total return. |

Neither approach is automatically superior. The choice is an allocation decision, not a universal rule. The better interpretation depends on the investor’s income needs, portfolio construction, tax situation, diversification, and view of the asset’s valuation and fundamentals.

When Dividend Reinvestment Can Mislead

Dividend reinvestment can create false comfort when the focus stays on growing share count while the dividend itself becomes less secure. A high dividend yield may look attractive for reinvestment, but weak coverage can make the payout more vulnerable.

Common mistake: Treating reinvested dividends as evidence of quality confuses an investor action with a company condition. The investor may be accumulating more shares, while the company may still be facing payout pressure, weaker cash generation, or rising balance-sheet risk.

The interpretation also weakens when dividend growth is not supported by free cash flow. A rising dividend can appear attractive, but the durability of that increase depends on whether the company can fund it without starving reinvestment needs, increasing leverage, or relying on temporary conditions.

Valuation matters as well. Reinvestment automatically directs capital into the same asset. If the shares are priced aggressively relative to business quality and cash flow durability, reinvestment can increase exposure at a less attractive expected return.

How to Analyze Dividend Reinvestment in Context

Dividend reinvestment deserves more analytical weight when the underlying dividend is supported by cash flow, the payout burden is manageable, and dividend growth is consistent with the company’s economics. It deserves less weight when the dividend is high mainly because the share price has fallen, coverage is weak, or reinvestment needs inside the business are being underfunded.

| Check | Why it matters |

|---|---|

| Dividend coverage ratio | Tests whether the dividend is supported by earnings or cash flow. |

| Dividend payout ratio | Shows how much room remains after distributions. |

| Free cash flow support | Separates funded dividends from accounting-only comfort. |

| Dividend growth durability | Tests whether increases are backed by business economics. |

| Balance-sheet room | Shows whether leverage or liquidity limits the payout. |

| Valuation context | Tests whether reinvestment is adding exposure at a reasonable price. |

A stronger analysis checks whether the company’s dividend payout ratio leaves enough room for reinvestment, debt service, cyclical pressure, and future business needs. A payout that consumes too much of earnings or cash flow can make reinvestment look better on the investor side than the company’s economics justify.

Dividend growth also needs context. A durable dividend growth rate is more meaningful when it is backed by cash generation, balance-sheet flexibility, and a business model that can support distributions through different operating conditions.

Tax and Account Considerations

Reinvested dividends may still be taxable in taxable accounts, even when the cash is automatically used to buy more shares. The reinvestment changes how the dividend is used, not necessarily whether the dividend is treated as taxable income.

Tax treatment depends on account type, jurisdiction, dividend classification, and individual circumstances. The investing analysis should separate the dividend’s business quality from the investor’s after-tax outcome.

A Practical Interpretation

Dividend reinvestment is best understood as an accumulation mechanism, not a dividend-quality metric. It can increase ownership and future dividend exposure, but only after the underlying dividend has been tested.

The decision deserves more weight when cash flow, payout burden, balance-sheet room, reinvestment needs, and valuation all support the dividend. It deserves less weight when reinvestment simply adds exposure to a fragile payout, deteriorating fundamentals, or an overextended valuation.

FAQ

Is dividend reinvestment the same as compounding?

Dividend reinvestment can contribute to compounding because dividends buy more shares, and those shares may receive future dividends. It is not guaranteed compounding because future results still depend on dividend durability, share price, valuation, and business performance.

Are reinvested dividends still taxable?

In taxable accounts, reinvested dividends may still be taxable even though the cash is used to buy more shares. Tax treatment depends on account type, jurisdiction, and dividend classification.

Does dividend reinvestment make a dividend stock safer?

No. Dividend reinvestment changes what happens to the dividend after payment. It does not show that the company can sustain the dividend or that the payout is well covered.

What is a DRIP?

A DRIP automatically uses dividend payments to buy additional shares. It is a reinvestment mechanism, not evidence that the dividend is safer or better covered.