Discounted cash flow is a valuation method that estimates what expected future cash flows may be worth today after discounting them for time, risk, and required return.

A DCF model does not prove the true value of a company. It turns assumptions about cash flow, growth, discount rate, and terminal value into a present-value estimate that can be reviewed against business quality, cash-flow durability, balance-sheet risk, and market price.

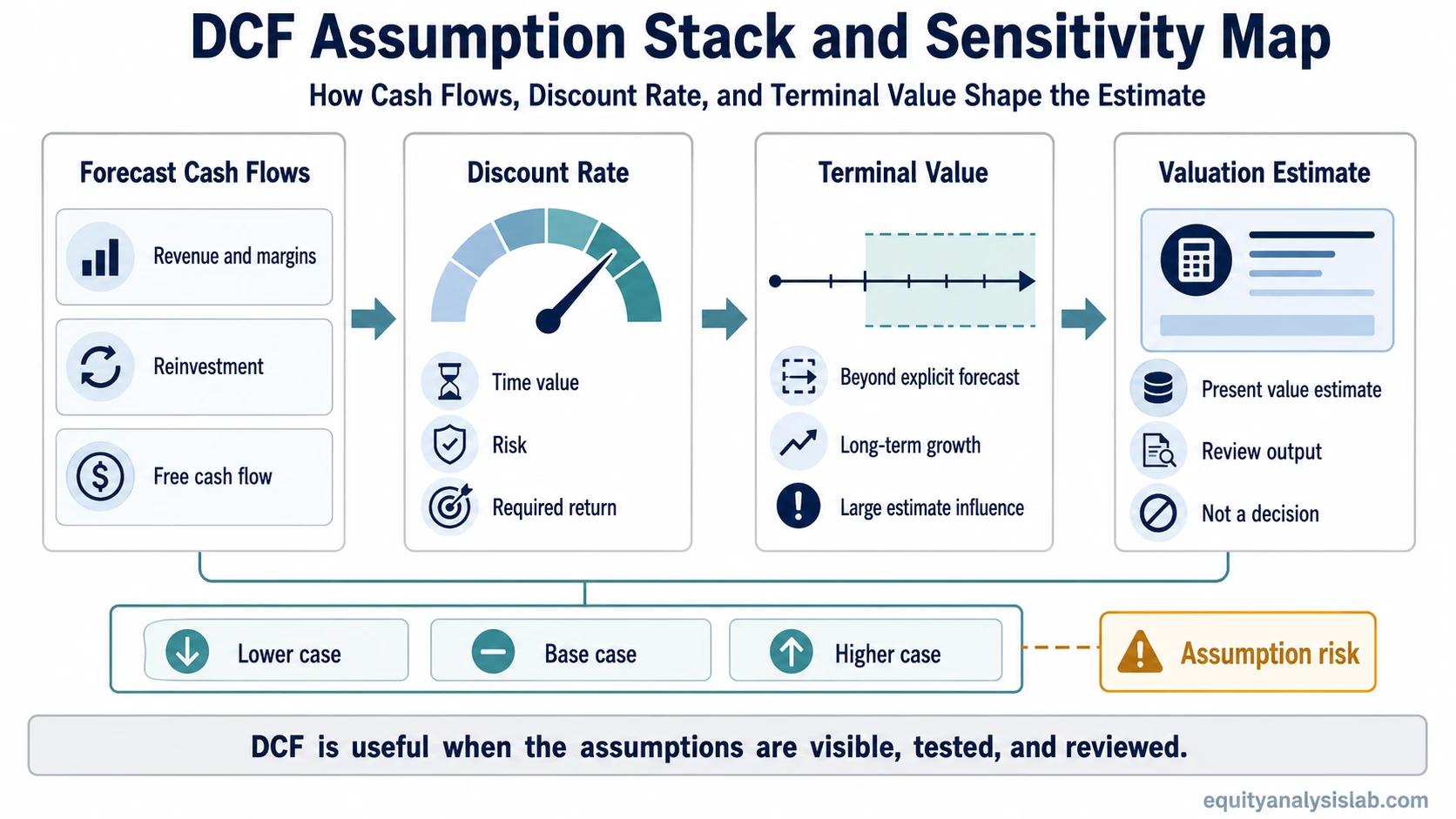

Definition: Discounted cash flow, often shortened to DCF, estimates present value by forecasting future cash flows and discounting them back to today. The method is most useful when future cash generation can be estimated with enough discipline to test the assumptions behind the valuation.

Key Points About Discounted Cash Flow

- DCF estimates present value from expected future cash flows.

- The main inputs are projected cash flow, growth, discount rate, terminal value, and the bridge from enterprise value to equity value.

- The output can change materially when discount-rate, growth, or terminal-value assumptions change.

- DCF is a valuation review tool, not an investment decision by itself.

What Is Discounted Cash Flow?

Discounted cash flow is based on the time value of money. A dollar expected several years from now is usually worth less than a dollar available today because the future dollar carries timing risk, business risk, financing risk, and opportunity cost.

In company valuation, a DCF model usually starts with expected future cash flows, discounts each forecast period back to present value, adds a terminal value for cash flows beyond the explicit forecast period, and then adjusts the result to estimate enterprise value or equity value.

The most useful output is the assumption trail behind the final number: which cash flows were used, how durable those cash flows appear, what discount rate was selected, and how much of the estimate depends on terminal value.

How Discounted Cash Flow Works

A DCF model follows a sequence. The analyst forecasts cash flows over an explicit period, selects the cash-flow type, applies a discount rate, estimates terminal value, discounts those amounts to present value, and then compares the estimate with market price and valuation context.

The forecast period is where business analysis enters the model. Revenue growth, margins, reinvestment needs, working capital, capital expenditures, taxes, and cash conversion can all change the cash-flow path. The discount rate then translates those future cash flows into today’s value by reflecting time and risk.

DCF can be used with different cash-flow bases. Free Cash Flow to the Firm is commonly used when valuing the operating business before financing structure.

A shareholder-level model may use free cash flow to equity after debt, interest, and financing effects are considered.

Key Inputs in a DCF Model

A DCF estimate is best read as an assumption stack. Each layer affects the next one, and a weak layer can make the final output look more precise than it really is.

| DCF input | What it represents | Why it matters |

|---|---|---|

| Forecast cash flow | Expected cash generated during the explicit forecast period | Small changes in growth, margins, reinvestment, or working capital can shift the valuation base. |

| Cash-flow type | Whether the model values the firm or the equity directly | The cash-flow definition must match the discount rate and valuation bridge. |

| Growth assumptions | Expected expansion or contraction in revenue, margins, and cash flow | Overly smooth growth can hide cyclicality, competitive pressure, or capital intensity. |

| Discount rate | The rate used to convert future cash flows into present value | A higher rate reduces the present value of future cash flows; a lower rate increases it. |

| Terminal value | The estimated value of cash flows beyond the explicit forecast period | Terminal value can dominate the estimate, especially when the explicit forecast period is short. |

| Net debt and other adjustments | The bridge from enterprise value to equity value | Debt, cash, minority interests, leases, and other claims can change what common shareholders may own. |

The DCF formula mechanics define how future cash flows are mathematically discounted into present value. In practical valuation work, the larger issue is how the assumptions interact: cash-flow durability, discount-rate selection, terminal-value dependence, and the bridge from enterprise value to equity value.

Discount Rate and Terminal Value

The discount rate is one of the most important judgment points in a DCF model. For a firm-level DCF, analysts often use a weighted average cost of capital because the model values cash flows available to all capital providers. For an equity-level DCF, the discount rate should reflect the required return on equity.

Terminal value estimates what the business may be worth after the explicit forecast period. That estimate can be based on a long-term growth assumption or an exit multiple. Both approaches require caution because small changes in long-term assumptions can move the valuation materially.

Limitation: A DCF output can look exact even when the most important inputs are judgment calls. The model should usually be read as a valuation range, not as a single precise answer.

Discounted Cash Flow Sensitivity

Sensitivity analysis shows how much the valuation changes when key assumptions move. This matters because a DCF estimate can be highly dependent on a small number of inputs, especially the discount rate, terminal growth rate, margin path, and terminal value method.

| Assumption change | Typical valuation effect | What to review |

|---|---|---|

| Higher discount rate | Lower present value | Whether the risk level, leverage, cyclicality, or uncertainty justifies the rate. |

| Lower discount rate | Higher present value | Whether the model is understating business, financing, or forecast risk. |

| Higher terminal growth | Higher terminal value | Whether long-term growth is realistic relative to industry maturity and reinvestment needs. |

| Lower terminal growth | Lower terminal value | Whether the business is more mature, cyclical, or capital intensive than the base case assumes. |

| Higher margins | Higher forecast cash flow | Whether margin expansion is supported by pricing power, scale, or cost structure. |

| Higher reinvestment needs | Lower free cash flow | Whether growth requires more capital than the model originally assumed. |

If a small change in one assumption creates a large change in the valuation, the estimate is fragile. If several reasonable scenarios point to a similar range, the model is more useful as a valuation cross-check.

Example of How DCF Assumptions Can Change the Estimate

Consider a company that appears stable under a base-case forecast. If the model assumes steady cash-flow growth, modest reinvestment, and a moderate discount rate, the valuation may look comfortably above the current market price.

That conclusion can change if the business needs more capital to grow, margins normalize, or the discount rate rises. The same company may look undervalued in one scenario and only fairly valued in another.

Illustrative example: A DCF model that depends heavily on terminal value should be reviewed with extra caution. If most of the estimated value comes from cash flows far beyond the forecast period, the result depends more on long-term assumptions than on near-term business evidence.

DCF and Intrinsic Value

DCF is often used to estimate intrinsic value, but the two terms are not identical. Intrinsic value is the estimated economic worth of an asset. DCF is one method that can be used to estimate that worth.

The distinction matters because a DCF result is only as reliable as the assumptions behind it. A polished model can still be weak if cash-flow forecasts are unrealistic, the discount rate is too low, terminal value is aggressive, or balance-sheet adjustments are incomplete.

When Discounted Cash Flow Is Useful

DCF is most useful when the business has reasonably visible cash flows, an understandable reinvestment profile, and assumptions that can be tested. It can work well for mature companies, stable cash-generating businesses, and companies where long-term economics can be estimated with some discipline.

DCF can also help separate business analysis from market pricing. Instead of only asking what peers trade for, the model asks what the business may be worth under a set of cash-flow assumptions.

When DCF Is Less Reliable

DCF becomes less reliable when future cash flows are highly uncertain, the business model is changing quickly, profitability is not yet visible, or terminal value explains most of the estimate. In those cases, the model may still be useful for scenario analysis, but the final number should not be treated as precise.

Common mistake: Treating the DCF output as “the value” instead of asking which assumptions caused the output. A better review starts with the cash-flow path, discount rate, terminal value, and sensitivity range.

Discounted Cash Flow vs Other Valuation Methods

DCF is one valuation method, not the entire valuation process. It is often used alongside market-based methods, accounting checks, and business-quality review.

Comparable Company Analysis looks at how similar companies are priced in the market.

A market-relative cross-check can show whether a DCF estimate is far away from peer valuation levels, but peer multiples can also reflect market mood, accounting differences, or business-quality gaps.

A dividend-focused valuation approach is narrower because it values expected dividends rather than broader free cash-flow generation.

DCF and NPV share the idea of discounting future cash flows, but they are often used in different contexts. DCF is commonly used to value companies or securities, while NPV is often used to evaluate a project, investment, or capital allocation decision.

How to Read a DCF Estimate

A DCF estimate should be read through three questions. Are the cash flows realistic? Is the discount rate appropriate for the risk? Does the terminal value explain too much of the result?

If the answer depends mainly on one optimistic assumption, the valuation range is fragile. If the estimate holds across several reasonable scenarios, the model gives a more useful view of valuation context, although it still does not make the investment decision by itself.

FAQ

Is DCF the same as intrinsic value?

No. DCF can be used to estimate intrinsic value, but the result depends on the assumptions used in the model. It is an estimate, not proof of exact value.

Why does the discount rate matter in DCF?

The discount rate converts future cash flows into present value. A higher discount rate usually lowers the estimate, while a lower discount rate usually raises it.

Why can terminal value make DCF fragile?

Terminal value often represents a large share of the total estimate. If the long-term growth or exit assumptions are too optimistic, the final valuation can look more precise than it is.

Can DCF tell whether a stock should be bought?

No. DCF can support valuation review, but it does not make a buy or sell decision by itself. Business quality, risk, portfolio context, market price, and assumption sensitivity still need review.