Sum of the parts valuation is a method for valuing a company by valuing its separate business segments first, then combining those segment values into one company-level estimate. It is most useful when one blended multiple, discount rate, or growth assumption would hide how different parts of the company actually earn money.

The output is not proof of fair value and it is not a price target. SOTP is an assumption-based valuation estimate that depends on how the analyst defines segments, chooses valuation methods, adjusts for corporate items, and converts enterprise value into equity value.

What is sum of the parts valuation?

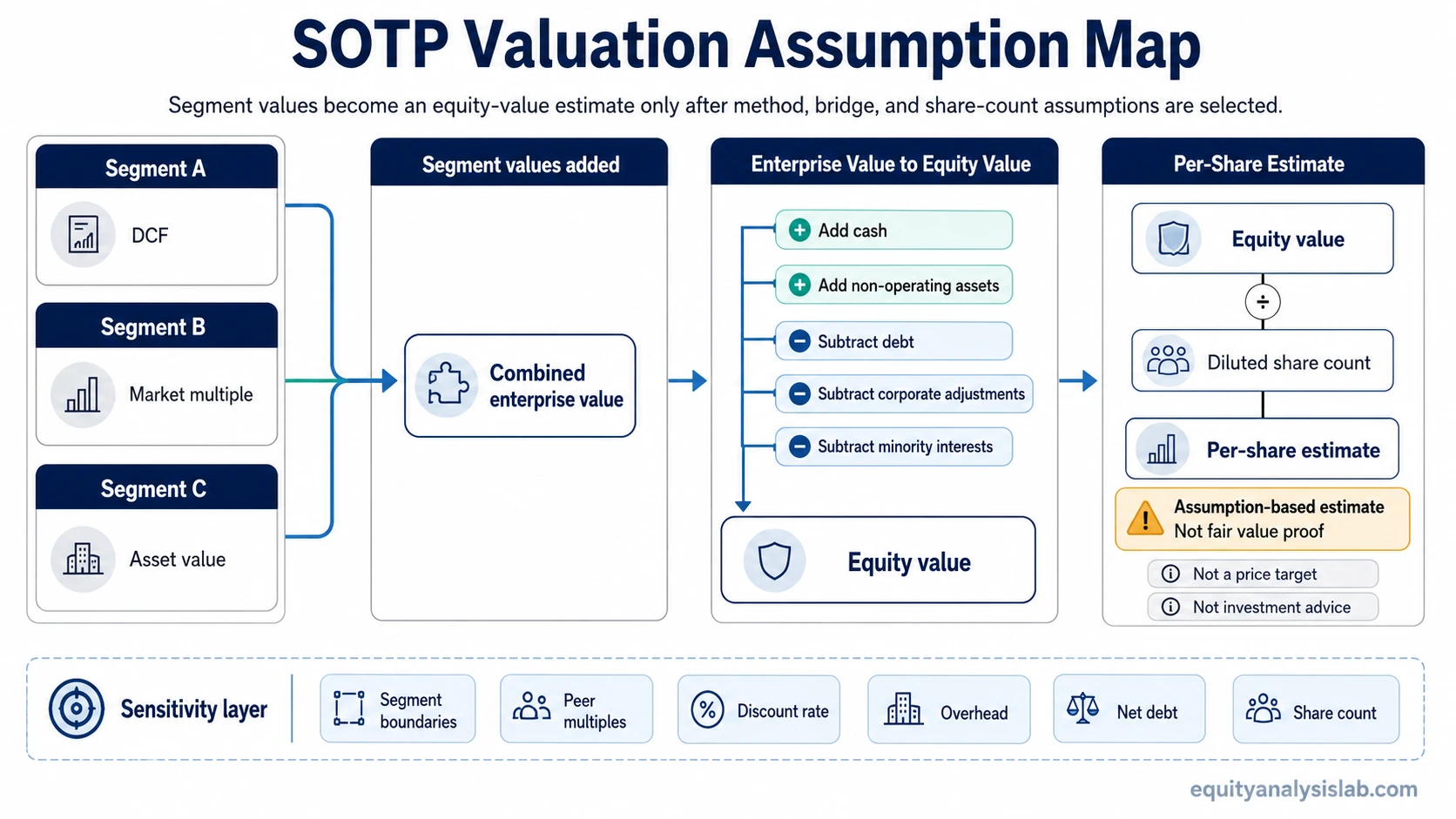

Sum of the parts valuation, often shortened to SOTP, separates a company into operating segments, values each segment using an appropriate method, adds the segment values together, and then adjusts for items such as corporate overhead, cash, debt, minority interests, and share count.

The method is designed for companies where the parts may deserve different valuation treatment. A software segment, a manufacturing segment, a financial-services segment, and a real-estate asset may not be well represented by a single company-wide multiple.

Key Points

- SOTP values separate business segments before building a company-level valuation estimate.

- Different segments can use different valuation methods, such as multiples, discounted cash flow, or asset-based estimates.

- The bridge from segment enterprise value to equity value must account for cash, debt, corporate costs, minority interests, and share count.

- The result can move materially when segment boundaries, peer groups, margins, growth, discount rates, or overhead assumptions change.

- SOTP is a valuation framework, not a guarantee that the market will recognize a specific value.

When SOTP valuation is useful

SOTP is useful when a company contains unlike businesses that should not be valued as if they had the same economics. A diversified company may have one segment with recurring revenue, another with cyclical earnings, and another with asset-heavy balance-sheet value. Combining them into one blended metric can make the valuation look cleaner than the business really is.

The method can also help when management reports enough segment detail for revenue, margins, assets, or cash flow to be analyzed separately. Without segment-level disclosure, the SOTP model may look precise while relying on weak allocation assumptions.

| Situation | SOTP fit | Reason |

|---|---|---|

| Company has clearly different business segments | Strong | Each segment may need its own multiple, margin profile, or cash-flow model. |

| Company reports useful segment data | Strong | The analyst can connect assumptions to disclosed operating information. |

| Company has one main operating business | Weak | A single valuation method may already capture the core economics. |

| Segment disclosures are vague or inconsistent | Risky | The model may depend more on analyst allocation choices than on observable data. |

How sum of the parts valuation works

The basic process is to identify the major parts of the company, assign a valuation method to each part, estimate the value of each part, add the values, and then bridge from combined enterprise value to equity value.

- Step 1: Define the operating segments or assets that should be valued separately.

- Step 2: Select the relevant metric for each segment, such as revenue, EBITDA, EBIT, free cash flow, invested capital, or asset value.

- Step 3: Choose a valuation method for each segment. A mature cash-generating segment may fit discounted cash flow, while a segment with strong market comparables may fit comparable company analysis or another form of relative valuation.

- Step 4: Add the estimated enterprise values of the separate segments.

- Step 5: Adjust for corporate-level items and convert the result into equity value per share.

A simple formula can be written as:

SOTP equity value = segment value A + segment value B + segment value C + non-operating assets + cash − debt − corporate adjustments − minority interests

If the final output is shown per share, the equity value is divided by the relevant share count. That share count choice matters, especially when diluted shares, options, convertibles, or other dilutive securities could change ownership claims.

When a segment value is built from present value mechanics, the DCF formula is one way to connect expected cash flows, terminal value, and discount rate to the segment estimate.

The assumptions that move SOTP value

SOTP often looks mechanical, but the model is driven by assumptions. The biggest changes usually come from segment boundaries, valuation method choice, peer selection, margin normalization, growth estimates, discount rates, terminal value assumptions, corporate overhead, and the equity bridge.

| Assumption | What the analyst chooses | How it can move value |

|---|---|---|

| Segment definition | Which businesses are separated or grouped together | A high-quality segment can be diluted if it is grouped with a lower-quality segment. |

| Segment metric | Revenue, EBITDA, EBIT, free cash flow, asset value, or another base | The same segment may look expensive or cheap depending on the metric used. |

| Method choice | Market multiple, DCF, asset value, or another approach | Different methods can produce different ranges even when the same segment is being valued. |

| Peer selection | Which comparable companies or transactions set the multiple range | A stronger or weaker peer set can shift the implied valuation range. |

| Growth and margin assumptions | Future revenue, profitability, reinvestment, and cash conversion | Small changes can compound when they affect terminal or normalized value. |

| Discount rate | Required return used for cash-flow-based segment estimates | A higher discount rate reduces present value, especially for long-duration cash flows. |

| Corporate overhead | Costs that sit above segment reporting | Ignoring overhead can overstate the value available to shareholders. |

| Balance-sheet bridge | Cash, debt, minority interests, pensions, leases, and non-operating assets | The bridge can materially change the difference between enterprise value and equity value. |

| Share count | Basic, diluted, or adjusted shares | Per-share value can fall when dilution is included. |

Enterprise value to equity value bridge

Adding segment values usually produces an enterprise-value-style estimate before final shareholder adjustments. That combined value still needs to be bridged to common equity value.

| Bridge item | Typical treatment | Why it matters |

|---|---|---|

| Cash and cash equivalents | Often added if not already embedded in segment values | Cash can increase equity value available to shareholders. |

| Debt | Usually subtracted from enterprise value | Debt claims sit ahead of common equity claims. |

| Corporate overhead | Capitalized, deducted, or otherwise reflected | Central costs may not belong to one segment but still reduce company-level value. |

| Minority interests | Adjusted based on ownership and consolidation treatment | The company may not own 100 percent of every value stream. |

| Non-operating assets | Added separately when not captured in segment valuation | Assets outside the operating segments can still belong in equity value. |

| Diluted share count | Used when calculating value per share if dilution is relevant | The same equity value can produce a lower per-share estimate when more shares are included. |

Simple SOTP valuation example

Assume a company has two operating segments and one non-operating asset. Segment A is valued at 500 million, Segment B is valued at 350 million, and the non-operating asset is valued at 50 million. The company also has 120 million of debt, 20 million of cash, and 100 million diluted shares.

| Item | Value | Treatment |

|---|---|---|

| Segment A | 500 million | Add |

| Segment B | 350 million | Add |

| Non-operating asset | 50 million | Add |

| Cash | 20 million | Add |

| Debt | 120 million | Subtract |

The implied equity value is 800 million: 500 million + 350 million + 50 million + 20 million − 120 million. Dividing 800 million by 100 million diluted shares gives an implied value of 8.00 per share.

The same structure would produce a different result if the subscription segment received a lower multiple, if debt were higher, or if diluted share count increased.

The example is simplified. Real SOTP work may need separate tax treatment, pensions, leases, minority interests, segment-level capital needs, and different valuation methods for each part.

Why SOTP can mislead investors

SOTP can mislead when the segment values look precise but the inputs are weak. A model can add many separate parts while still depending on aggressive peer multiples, optimistic margins, incomplete debt adjustments, or segment boundaries that do not match economic reality.

| Common mistake | Why it matters | Better check |

|---|---|---|

| Using one blended multiple for unlike segments | The model may hide different growth, margin, and risk profiles. | Match the method and peer set to each segment. |

| Ignoring corporate overhead | Segment values may overstate what belongs to shareholders. | Identify costs that remain at the company level. |

| Forgetting the equity bridge | Enterprise value is not the same as common equity value. | Adjust for cash, debt, minority interests, and other claims. |

| Using weak segment data | Allocation estimates may drive the result more than disclosed economics. | Separate reported data from analyst allocation assumptions. |

| Treating SOTP as a price target | The market may not recognize the same assumptions or timing. | Read the output as an assumption-based valuation range. |

SOTP valuation limitations

SOTP works best when segment economics are genuinely different and the available disclosures support separate analysis. It becomes weaker when the company reports limited segment data, when peer sets are stretched, or when most of the implied value comes from assumptions that are hard to test.

The strongest SOTP conclusion is not the one with the highest value. It is the one where the segment logic, method choice, balance-sheet bridge, and per-share calculation remain understandable under conservative, base, and optimistic cases.

SOTP valuation checklist

| Question | Risk if ignored | What a stronger analysis shows |

|---|---|---|

| Are the segments economically different? | Separate valuation may add complexity without improving understanding. | Clear segment differences support separate valuation. |

| Is the segment data reliable? | Weak disclosure forces more allocation assumptions. | Reported segment revenue, profit, assets, or cash flow improve model discipline. |

| Are peer groups matched to segment economics? | Wrong peers can create a misleading valuation range. | Peers with similar growth, margins, cyclicality, and capital intensity improve comparability. |

| Is the equity bridge complete? | Enterprise value is not the same as common equity value. | Cash, debt, minority interests, liabilities, and dilution are treated explicitly. |

| Does the conclusion depend on one aggressive input? | Sensitivity reveals whether the estimate is robust or fragile. | The range remains reasonable across conservative and optimistic cases. |

FAQ

Is SOTP the same as DCF?

No. SOTP is a framework for combining separate segment values. A DCF model can be used to value one or more of those segments, but SOTP can also use multiples, asset values, or other methods.

Does SOTP prove fair value?

No. SOTP produces an assumption-based valuation estimate. The result depends on segment definitions, method choice, peer groups, forecast inputs, corporate adjustments, and share count.