Valuation methods are structured ways to estimate what a company, security, or business interest may be worth. The useful starting point is not choosing the most complex model. It is matching the method to the kind of business being analyzed, the quality of the available inputs, and the question the valuation needs to answer.

For a company with visible cash flows, an income-based method may be the first approach to review. For a company with a strong peer set, a market-based method can help compare valuation against similar businesses. For a dividend-focused company, dividend capacity may matter more than headline earnings. For a multi-segment business, the right path may require separating the parts before combining the estimate.

Key Points

- Valuation methods group into cash-flow, market-based, dividend-based, asset-based, and segment-based approaches.

- The method should match the company’s economics, not only the analyst’s preferred model.

- Different methods can produce different valuation ranges because they rely on different assumptions.

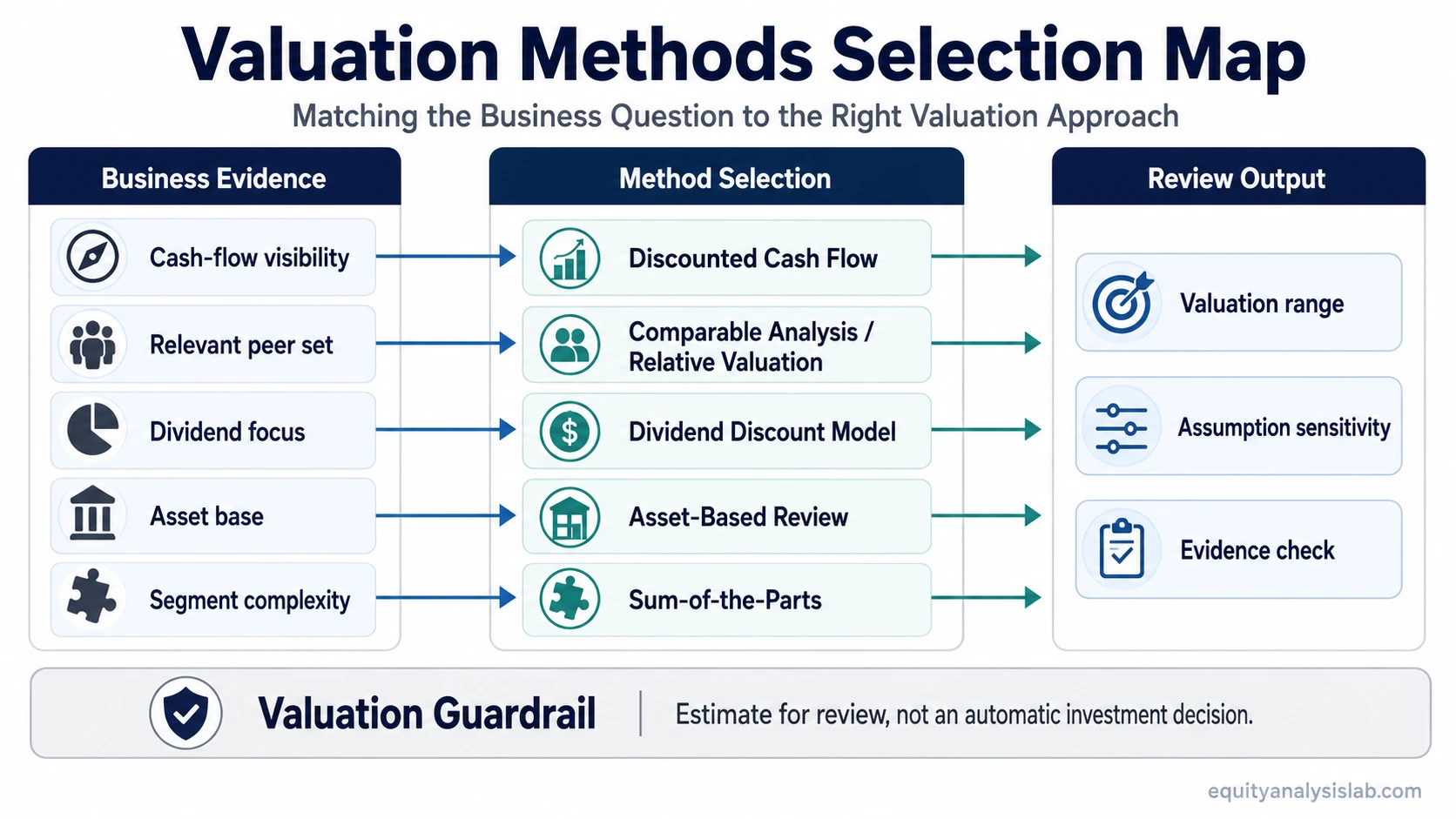

- A valuation output is an estimate for review, not an automatic investment decision.

How to Choose Between Valuation Methods

The method-selection process starts with the evidence available for the business. Cash-flow visibility, peer comparability, dividend policy, asset base, and segment structure each point toward a different valuation approach.

| Starting question | Method to review | Why it fits |

|---|---|---|

| Can the company’s future cash flows be estimated with reasonable structure? | discounted cash flow | Cash-flow valuation connects estimated future cash flows to present value assumptions. |

| Does the company have a relevant peer group? | comparable company analysis | Peer analysis compares market pricing against businesses with similar economics or risk profiles. |

| Is the main question whether the current multiple looks reasonable? | relative valuation | Multiples help frame the company against earnings, sales, cash flow, book value, or other reference measures. |

| Is the company valued mainly for recurring dividend capacity? | dividend-based valuation | Dividend-focused methods connect value to expected shareholder distributions. |

| Does one consolidated company contain several different businesses? | sum-of-the-parts valuation | Segment-based valuation can separate divisions that deserve different assumptions or peer groups. |

Main Valuation Method Families

Most company valuation work starts by sorting the problem into a few method families. The labels differ across finance, accounting, appraisal, and investment education, but the investor’s practical question is usually the same: which evidence is strong enough to support the estimate?

Company and security valuation for investor analysis usually differs from startup pricing, real-estate appraisal, and legal or accounting fair-value work. Those areas may use related language, but they rely on different evidence requirements, standards, and decision contexts.

| Method family | Common use | Main input risk |

|---|---|---|

| Income approach | Businesses where future cash flow, reinvestment, and discount-rate assumptions can be modeled. | Small changes in growth, margin, discount rate, or terminal assumptions can move the estimate materially. |

| Market approach | Businesses with observable peer companies, transactions, or public-market valuation multiples. | The peer set may not match the company’s growth, margins, leverage, accounting quality, or risk profile. |

| Asset-based approach | Asset-heavy or balance-sheet-centered situations where asset values matter more than normalized earnings power. | Book value, replacement value, and liquidation value can differ from economic value. |

| Dividend approach | Companies where dividends are stable, intentional, and central to the investor’s valuation question. | Dividend history may not reflect future distribution capacity or capital-allocation priorities. |

| Segment-based approach | Conglomerates or multi-business companies where one blended multiple would hide important differences. | Segment disclosures may be incomplete, and each part may require a different peer set or assumption base. |

Asset-based valuation affects method selection when balance-sheet value, liquidation value, replacement value, or asset backing matters more than normalized earnings power. It should be treated as a distinct method family because the evidence base differs from cash-flow, market, dividend, or segment-based valuation.

Cash-Flow Valuation Methods

Cash-flow valuation is most useful when the analyst can build a reasoned estimate of future operating performance, reinvestment needs, and long-term economics. The method does not become stronger because the model is detailed. It becomes stronger when the assumptions are tied to business quality, cash conversion, capital intensity, and risk.

A cash-flow approach can fit companies with durable revenue, understandable margins, and enough financial history to support explicit assumptions. It becomes weaker when the business is too early-stage, the cycle is unstable, or the terminal value dominates the estimate without enough support from the operating forecast.

When the main need is to understand the mechanics behind the model, the DCF formula is the better supporting topic. Formula detail should clarify the estimate, not make the result look more certain than it is.

Market-Based Valuation Methods

Market-based methods compare a company with other businesses or transactions. This approach can be useful when the peer group is real, the accounting base is comparable, and the market already prices similar business models with enough consistency to make the comparison meaningful.

The weak point is peer quality. A company can look cheap or expensive only because the comparison set is poorly chosen. Growth rate, margin structure, balance-sheet risk, customer concentration, cyclicality, and accounting differences can all distort the conclusion.

When the main challenge is building the peer group, how to choose comparable companies is the better next topic. Peer selection usually matters more than the surface multiple.

Dividend and Segment-Based Methods

Dividend-focused valuation fits companies where distributions are central to the investment case. It is less useful when dividends are irregular, management is changing capital-allocation priorities, or the payout does not reflect the company’s true earning power.

Segment-based valuation fits companies that combine businesses with different economics. One division may deserve a cash-flow lens, another may be compared with public peers, and another may require a more conservative asset or margin assumption. A single blended multiple can hide those differences.

Terminal value choices can also change the result. When a cash-flow model depends heavily on the final value estimate, the distinction between exit multiples and perpetuity growth assumptions should be reviewed through exit multiple vs perpetuity growth.

Where Valuation Methods Can Mislead

Valuation methods can make an estimate look precise even when the inputs are fragile. A model can be mathematically correct and still be economically weak if revenue durability, margin assumptions, reinvestment needs, terminal value, or peer selection are not realistic.

- False precision: A detailed spreadsheet does not prove that the estimate is reliable.

- Peer mismatch: Market multiples can mislead when the comparison companies have different economics.

- Terminal value dependence: A DCF can become mostly a terminal value estimate if the explicit forecast carries too little weight.

- Dividend overreach: A dividend model can fail when payout policy changes or distributions do not represent durable earning power.

- Segment simplification: A blended company multiple can hide high-quality and low-quality divisions inside the same business.

A Simple Method-Selection Scenario

A mature software company with recurring revenue, positive free cash flow, and a public peer group could support more than one valuation method. A cash-flow model may help test whether long-term margins and reinvestment assumptions justify the estimate. A market approach may show whether the current multiple is in line with similar companies. If the business also has separate infrastructure and services divisions, a segment-based view may prevent one average multiple from hiding different economics.

The useful comparison is not which method gives the highest value. The useful comparison is which method is best supported by the available evidence and which assumption would change the conclusion most.

Related Valuation Questions

Use the method that fits the specific valuation question. Cash-flow work belongs with DCF logic, peer-based work belongs with comparable analysis, multiples belong with relative valuation, dividend questions belong with dividend-based valuation, and mixed-business questions belong with segment-based valuation.

| Question | Relevant method |

|---|---|

| How do future cash flows translate into present value? | Discounted cash flow |

| Which companies should be compared? | Comparable company analysis |

| Which valuation multiple is being used and why? | Relative valuation |

| Do dividends represent the main valuation lens? | Dividend-based valuation |

| Should the company be separated into different business units? | Sum-of-the-parts valuation |

FAQ

What are the main valuation methods?

The main valuation methods include income-based methods, market-based methods, asset-based methods, dividend-based methods, and segment-based methods. Each method depends on a different evidence base, so the right choice depends on the company and the valuation question.

Which valuation method is best for a company?

No single valuation method is best for every company. Cash-flow methods fit companies with forecastable economics, market-based methods fit companies with useful peers, dividend methods fit distribution-focused businesses, and segment-based methods fit companies with distinct business units.

Can different valuation methods produce different values?

Yes. Different valuation methods can produce different estimates because they rely on different assumptions, peer groups, discount rates, growth expectations, asset values, or payout assumptions. The difference should be reviewed rather than treated as an automatic decision signal.