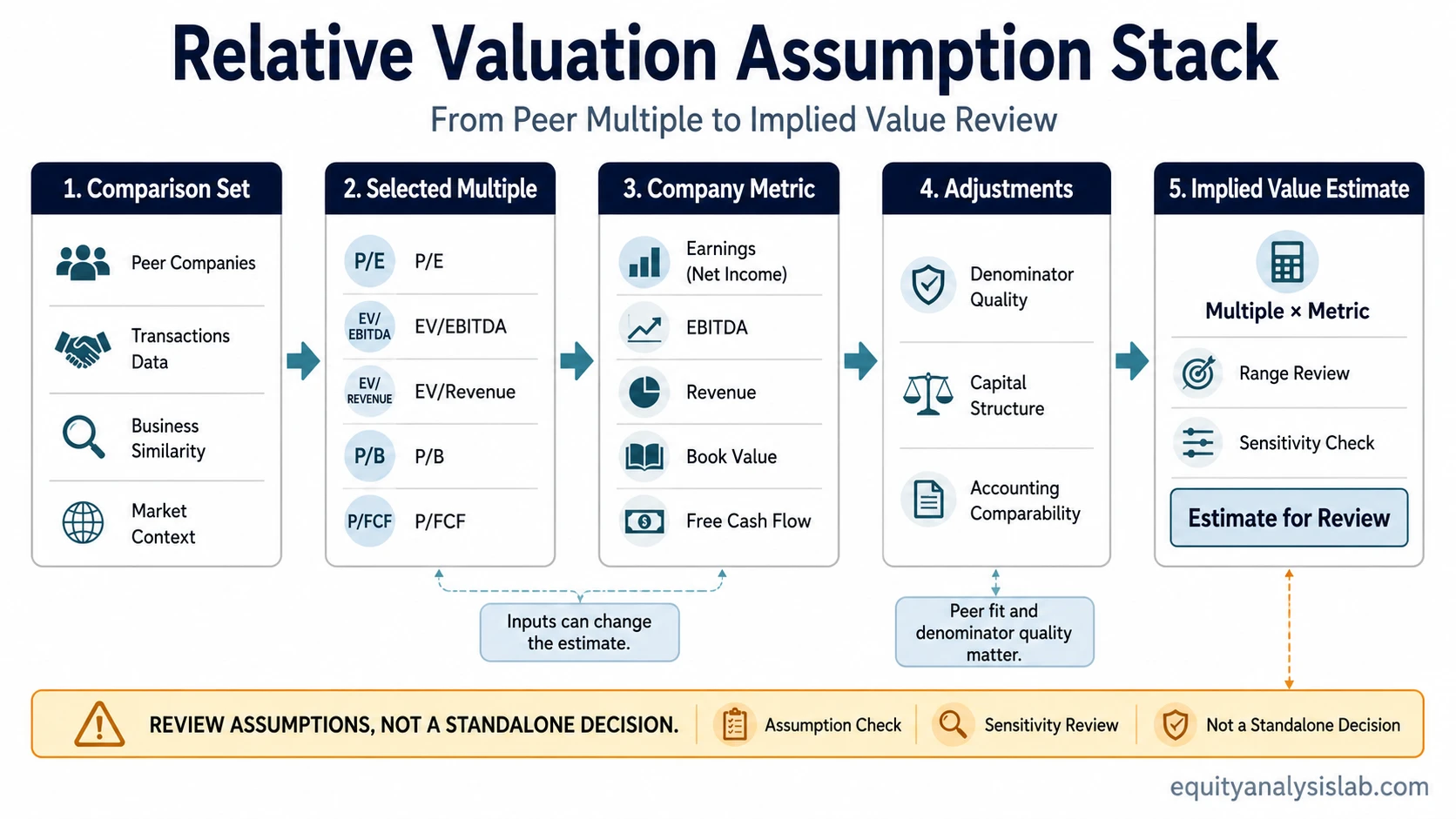

Relative valuation is a market-comparison valuation method that estimates value by applying peer or transaction multiples to a relevant company metric. The estimate depends on the comparison set, the selected multiple, denominator quality, capital structure, and assumptions about how similar the businesses really are.

The method is not a shortcut to a final investment decision. It helps frame whether a company looks expensive, cheap, or broadly in line with similar assets after differences in growth, profitability, leverage, accounting quality, and business risk are considered.

What Relative Valuation Means

Relative valuation estimates a company’s value by comparing it with similar companies or transactions using standardized valuation multiples. Common multiples include price-to-earnings, enterprise value to EBITDA, enterprise value to revenue, price-to-book, and price-to-free-cash-flow.

The method is relative because the estimate is anchored to market prices paid for comparable assets. That makes it different from an intrinsic cash-flow model, where the analyst estimates value from projected cash flows and a discount rate. Relative valuation asks what the market is paying for similar earnings, revenue, assets, or cash flow, then applies that comparison to the company being reviewed.

How Relative Valuation Works

The simplified mechanism is:

| Step | Question | Why it matters |

|---|---|---|

| Choose the comparison set | Which peers or transactions are genuinely comparable? | The estimate is only as useful as the peer group behind it. |

| Select the multiple | Should the comparison use earnings, EBITDA, revenue, book value, or free cash flow? | Different multiples emphasize different parts of the business model. |

| Check the denominator | Is the metric normalized, recurring, and comparable across companies? | A distorted denominator can make a multiple look more meaningful than it is. |

| Apply the multiple | What value is implied by the selected multiple and company metric? | The output gives an implied value estimate, not a standalone conclusion. |

The basic calculation is: selected multiple × relevant company metric = implied value estimate. For example, an EV/EBITDA comparison applies an enterprise-value multiple to EBITDA, while a price-to-earnings comparison applies an equity-value multiple to earnings.

A detailed peer-based implementation belongs to comparable company analysis. Relative valuation is the broader method family; comps are one common way to apply it, not a separate meaning of the same estimate.

Inputs and Assumptions Behind Relative Valuation

Relative valuation can look simple because the visible output is often a single multiple or range. A peer average can still be misleading if the companies differ materially in growth, margin structure, capital intensity, leverage, accounting treatment, cyclicality, or business quality.

| Input | What to check | Risk if ignored |

|---|---|---|

| Peer group | Business model, geography, scale, margin profile, growth, cyclicality, and customer mix | The company may be compared with businesses that deserve different multiples. |

| Selected multiple | Whether the metric matches the company’s economics and capital structure | The multiple may emphasize the wrong part of the business. |

| Denominator quality | Normalized earnings, recurring EBITDA, revenue quality, book value relevance, or free cash flow durability | A low multiple may come from inflated or non-recurring metrics. |

| Capital structure | Debt, cash, lease obligations, preferred securities, and minority interests where relevant | Equity-value and enterprise-value comparisons may be mixed incorrectly. |

| Accounting comparability | Revenue recognition, depreciation policy, stock-based compensation, one-time items, and adjustments | Reported metrics may not be comparable across companies. |

| Market pricing context | Sector cycle, interest-rate environment, risk appetite, and market-wide multiple levels | The peer group may be expensive or cheap as a group. |

Relative Valuation Multiples

Different multiples answer different comparison questions. Price-to-earnings compares equity value with accounting earnings. EV/EBITDA compares enterprise value with operating earnings before depreciation and amortization. EV/Revenue is sometimes used when earnings are weak or temporarily distorted, but it says less about profitability. Price-to-book can matter for asset-heavy or financial businesses, while price-to-free-cash-flow focuses on cash generation available after capital spending.

No multiple is universally better. The right multiple depends on what drives value in the business and whether the underlying metric is comparable. A software company, a bank, a retailer, and a commodity producer may require different comparison lenses because their economics, balance sheets, and accounting profiles are different.

Assumption Sensitivity in Relative Valuation

Small changes in the assumptions can move the implied value estimate materially. That sensitivity is why the method should be read as a range or review framework rather than a single precise answer.

| Assumption change | Effect on estimate | Interpretation risk |

|---|---|---|

| Peer multiple moves from 8x to 6x | Implied enterprise value falls even if the company metric is unchanged. | The original estimate may have depended on an aggressive peer set or market cycle. |

| EBITDA is adjusted downward for non-recurring items | The implied value falls because the denominator is lower. | Reported profitability may have overstated recurring economics. |

| A high-growth peer is removed | The peer median may decline. | The company may not deserve the same multiple as faster-growing peers. |

| Net debt is higher than expected | Equity value may be lower after enterprise value adjustments. | A headline multiple can hide balance-sheet risk. |

Simple Relative Valuation Example

A hypothetical company has $100 million of EBITDA. If an analyst applies an 8x EV/EBITDA multiple, the implied enterprise value is $800 million before net debt, cash, and other enterprise-value adjustments. If a more comparable peer set supports 6x instead of 8x, the implied enterprise value falls to $600 million even though EBITDA did not change.

The diagnostic point is not that one number is automatically correct. The peer set, multiple, denominator, and net debt adjustments can change the output before any investment conclusion is considered.

Relative Valuation vs Intrinsic Valuation

Relative valuation is market-based. It compares a company with similar public companies or transactions and asks what the market is paying for comparable earnings, revenue, assets, or cash flow. Intrinsic valuation estimates value from the company’s own projected cash flows, required return, and long-term assumptions.

The discounted cash flow method is one common intrinsic valuation approach. Its mechanics are different because the estimate depends on projected cash flows, discount rate, and terminal value rather than a peer multiple.

The discounted cash flow formula is a separate calculation structure and should not be treated as the same method as peer-based multiple comparison.

Both approaches can be useful because they test different assumptions. Relative valuation asks whether market pricing for similar assets supports the estimate. Intrinsic valuation asks whether the company’s own cash-flow profile supports the estimate.

Where Relative Valuation Can Mislead

A company trading at a discount to peers is not automatically undervalued. The discount can reflect weaker growth, lower margins, higher leverage, weaker earnings quality, customer concentration, poor capital allocation, accounting differences, or higher business risk. A premium multiple is not automatic proof of quality either.

Relative valuation can also mislead when the whole peer group is mispriced. If a sector is priced aggressively, a company can look reasonable relative to peers while still being expensive under more conservative assumptions. If a sector is depressed, a company can look cheap without having a clear catalyst or durable advantage.

The strongest use of relative valuation is comparative and diagnostic. It can highlight where assumptions need review, but it does not prove fair value, predict returns, or replace business-quality analysis.

How Investors Can Use the Estimate

Relative valuation is most useful when it is treated as one input in a broader valuation process. A useful review asks whether the peer group is credible, whether the chosen multiple fits the business, whether the denominator is durable, and whether the implied value remains reasonable under different assumptions.

The output should be read as an estimate for review, not as a buy or sell signal. A low multiple can raise a question. It does not answer the question by itself.

Related Valuation Methods

Relative valuation often sits beside other valuation methods rather than replacing them. Peer multiples can be compared with a DCF result, transaction multiples, or an asset-based method to test whether the valuation conclusion depends too heavily on one assumption set.

For diversified companies, conglomerates, or businesses with materially different segments, valuing separate business segments may be more useful than applying one blended multiple to the entire company.

FAQ

What is relative valuation?

Relative valuation estimates value by comparing a company with similar companies or transactions using standardized multiples such as price-to-earnings, EV/EBITDA, EV/Revenue, price-to-book, or price-to-free-cash-flow.

How is relative valuation calculated?

The simplified calculation is selected multiple multiplied by the relevant company metric. For example, an EV/EBITDA method applies an enterprise-value multiple to EBITDA, while a price-to-earnings method applies an equity-value multiple to earnings.

What makes a peer group comparable?

A peer group is more comparable when the companies have similar business models, growth rates, margins, capital intensity, accounting profiles, leverage, geography, and risk characteristics. A weak peer group can distort the valuation estimate.

Is a company undervalued if it trades below peer multiples?

Not automatically. A lower multiple can reflect mispricing, but it can also reflect weaker growth, lower margins, higher leverage, poorer earnings quality, accounting differences, or higher business risk.