Financial statements are accounting reports that show a company’s financial position, operating performance, cash movement, and changes in equity. Investors use them together because each statement answers a different question: how the company performed, what it owns and owes, how cash moved, and whether reported results are supported by the rest of the statement set.

Financial statements are a connected set of company reports. The income statement shows performance over a period, the balance sheet shows financial position at a point in time, and the cash flow statement shows how cash moved through the business. Equity-related statements or retained earnings schedules help explain how ownership value changed through profit retention, dividends, share issuance, or buybacks.

For investors, financial statements are not proof that a company is high quality or undervalued. They are the starting evidence for asking better questions about profitability, balance-sheet strength, cash conversion, reinvestment needs, and accounting quality.

- Financial statements work best as a set, not as isolated reports.

- The income statement answers profitability questions, but it does not show whether profit became cash.

- The balance sheet shows what the company owns, owes, and retains at a specific date.

- The cash flow statement connects accounting profit to actual cash movement.

- The statement set works best when each investor question is matched to the report that can answer it most directly.

What Financial Statements Show

Financial statements organize company information into separate but connected views. One statement may show that revenue and profit improved, while another may show whether cash collections, debt levels, inventory, receivables, or capital spending changed the quality of that result.

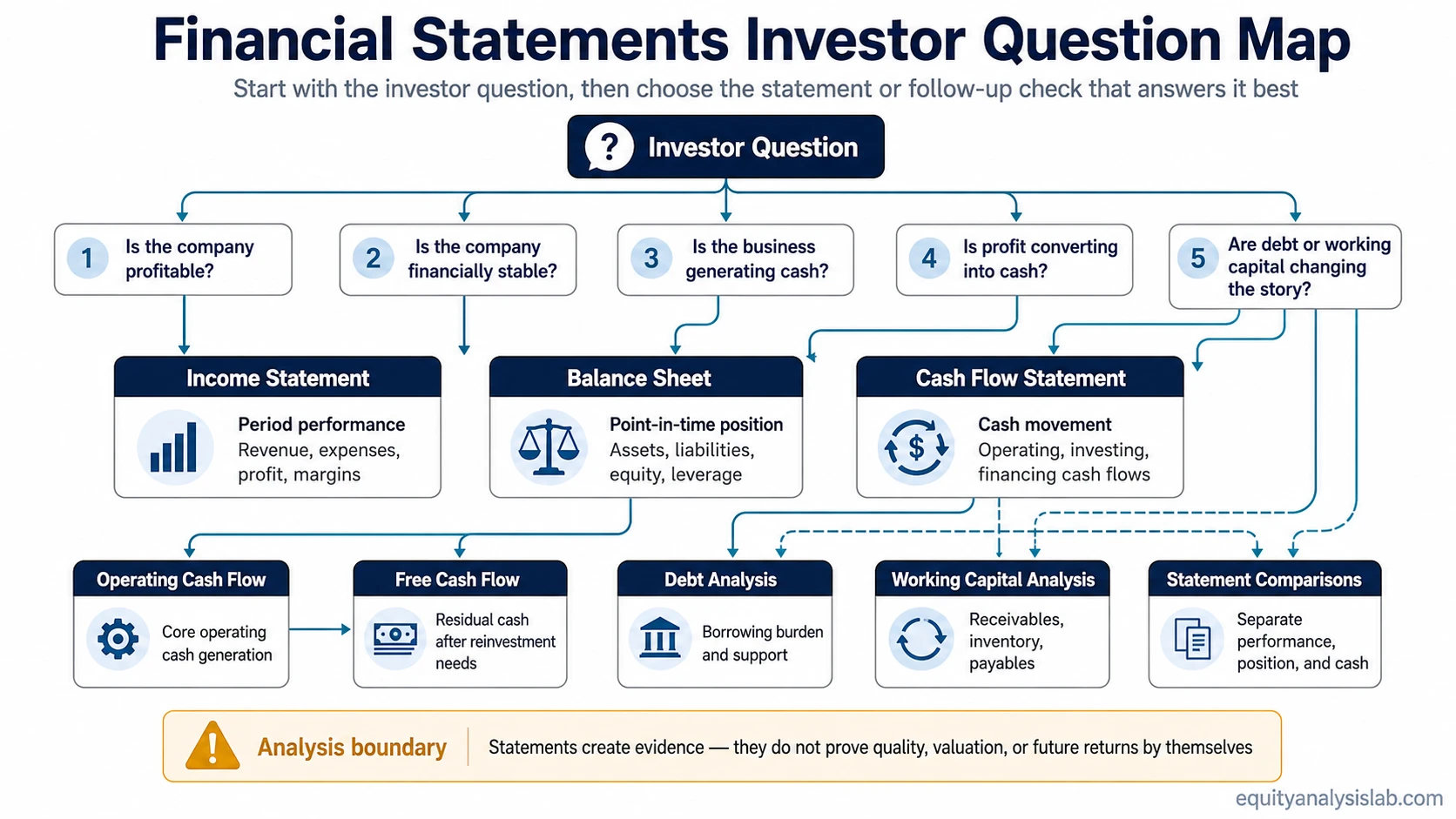

The main investor question is not simply whether the statements look clean. A stronger reading asks what each statement can show, what it cannot show alone, and which follow-up analysis is needed before drawing a conclusion.

The Main Financial Statements and What Each One Answers

Each financial statement has a different job. Reading them in the wrong order can make a company look stronger or weaker than the full statement set supports.

| Investor question | Primary statement or page | What it helps answer | What it does not answer alone |

|---|---|---|---|

| Is the company profitable? | Income statement | Revenue, expenses, operating income, net income, margins, and period performance. | Whether reported profit converted into cash or required heavy capital investment. |

| Is the company financially stable? | Balance sheet | Assets, liabilities, equity, leverage, liquidity, and financial position at a specific date. | Whether the company is earning enough profit or generating enough cash over time. |

| Is the business generating cash? | Cash flow statement | Operating, investing, and financing cash movement across the period. | Whether reported earnings are durable, competitively strong, or attractively valued. |

| Is profit converting into operating cash? | Operating cash flow | Cash generated or consumed by the company’s core operations. | How much cash remains after capital spending and reinvestment needs. |

| How much residual cash may remain after reinvestment? | Free cash flow | Cash left after operating needs and capital expenditures, depending on the definition used. | Whether management will allocate that cash well or whether valuation already reflects it. |

Investor Reading Path

The best starting point depends on the question the investor is trying to answer. Matching the question to the right statement avoids forcing every issue into one long accounting tutorial.

| Starting question | Use this path | Why this route fits |

|---|---|---|

| “Is the company making money?” | Income statement | Start with revenue, expenses, profit, and margins before moving into cash quality. |

| “Is the company carrying too much debt?” | Balance sheet → how to analyze debt | Debt risk usually needs both the balance-sheet position and the company’s ability to support obligations. |

| “Is reported profit becoming cash?” | Cash flow statement → operating cash flow → free cash flow | Cash conversion is clearer when operating cash generation and residual cash are separated. |

| “Is working capital absorbing cash?” | How to analyze working capital | Receivables, inventory, and payables can change the cash meaning of reported profit. |

| “Which statement am I confusing?” | Balance sheet vs income statement or free cash flow vs operating cash flow | Comparison pages help separate nearby concepts before the analysis moves deeper. |

How Investors Read Statements Together

The useful analysis often starts where the statements disagree. If net income rises but operating cash flow weakens, the investor may need to check whether receivables are growing faster than collections, inventory is building, or expenses are being recognized differently from cash movement. If debt increases while cash flow is flat, the balance sheet may change the interpretation of otherwise stable earnings.

The income statement, balance sheet, and cash flow statement therefore work as cross-checks. The income statement can show performance, the balance sheet can show financial strain or flexibility, and the cash flow statement can test whether accounting profit is supported by cash movement.

Example: Profit and Cash Flow Can Tell Different Stories

Suppose a company reports higher net income because sales increased. That result may look positive on the income statement. If the cash flow statement shows weak operating cash flow at the same time, the investor would need to check whether customers have been billed but not yet collected, inventory has increased, or working-capital needs are absorbing cash.

This does not automatically make the company weak. It means the statement set is asking for a cash-conversion check before the reported profit is treated as high quality.

Priority Paths Through Financial Statement Analysis

Start with the investor question, then move to the statement or comparison that gives the cleanest next answer.

| Priority path | Start here | Then check | Use when the question is about |

|---|---|---|---|

| Profitability path | Income statement | Margins, operating income, net income, and later cash conversion. | Revenue growth, expenses, profitability, and earnings direction. |

| Financial position path | Balance sheet | Assets, liabilities, equity, liquidity, leverage, and debt risk. | Solvency, balance-sheet strength, and financial flexibility. |

| Cash-quality path | Cash flow statement | Operating cash flow and free cash flow. | Cash generation, reinvestment needs, and profit quality. |

| Debt-risk path | Balance sheet | Debt analysis. | Borrowing burden, refinancing risk, and debt support. |

| Working-capital path | Working capital analysis | Receivables, inventory, payables, and operating cash flow effects. | Why profit and cash flow may diverge. |

| Statement-confusion path | Statement comparisons | Balance sheet vs income statement, and free cash flow vs operating cash flow. | Separating position, performance, and cash-based measures. |

What Financial Statements Cannot Prove

Financial statements can support analysis, but they do not prove business quality, predict future returns, or show that a stock is undervalued. A company can have clean statements and still face weak growth, competitive pressure, poor capital allocation, expensive valuation, dilution, or forward risk.

They also do not replace judgment. Investors still need to interpret accounting choices, business model durability, cash flow support, management decisions, and valuation context. The statements create the evidence base; they do not make the investment conclusion by themselves.

Where Financial Statement Analysis Stops

Financial statement analysis for investors is not the same as bookkeeping, accounting software selection, or a full technical accounting course. Detailed statement-level work belongs with the specific report, cash-flow measure, or comparison being analyzed.

Financial Statements FAQ

What are the main financial statements?

The main financial statements are the income statement, balance sheet, and cash flow statement. Equity-related statements or retained earnings schedules may also help explain changes in ownership value, retained profit, dividends, share issuance, or buybacks.

Why is one financial statement not enough?

One statement can show only part of the company. Profit may improve while cash flow weakens, or debt may rise while earnings look stable. Reading statements together helps investors test whether the numbers support the same story.