A balance sheet is a company financial statement that shows what the company owns, what it owes, and what belongs to shareholders at a specific reporting date. Investors use it to assess liquidity, leverage, asset quality, working capital, and financial flexibility, but the numbers need confirmation from earnings, cash flow, footnotes, and prior-period comparisons.

Balance sheet definition: a balance sheet reports a company’s assets, liabilities, and shareholders’ equity at one point in time. It is different from statements that describe activity across a period, because it captures the company’s financial position as of a specific date.

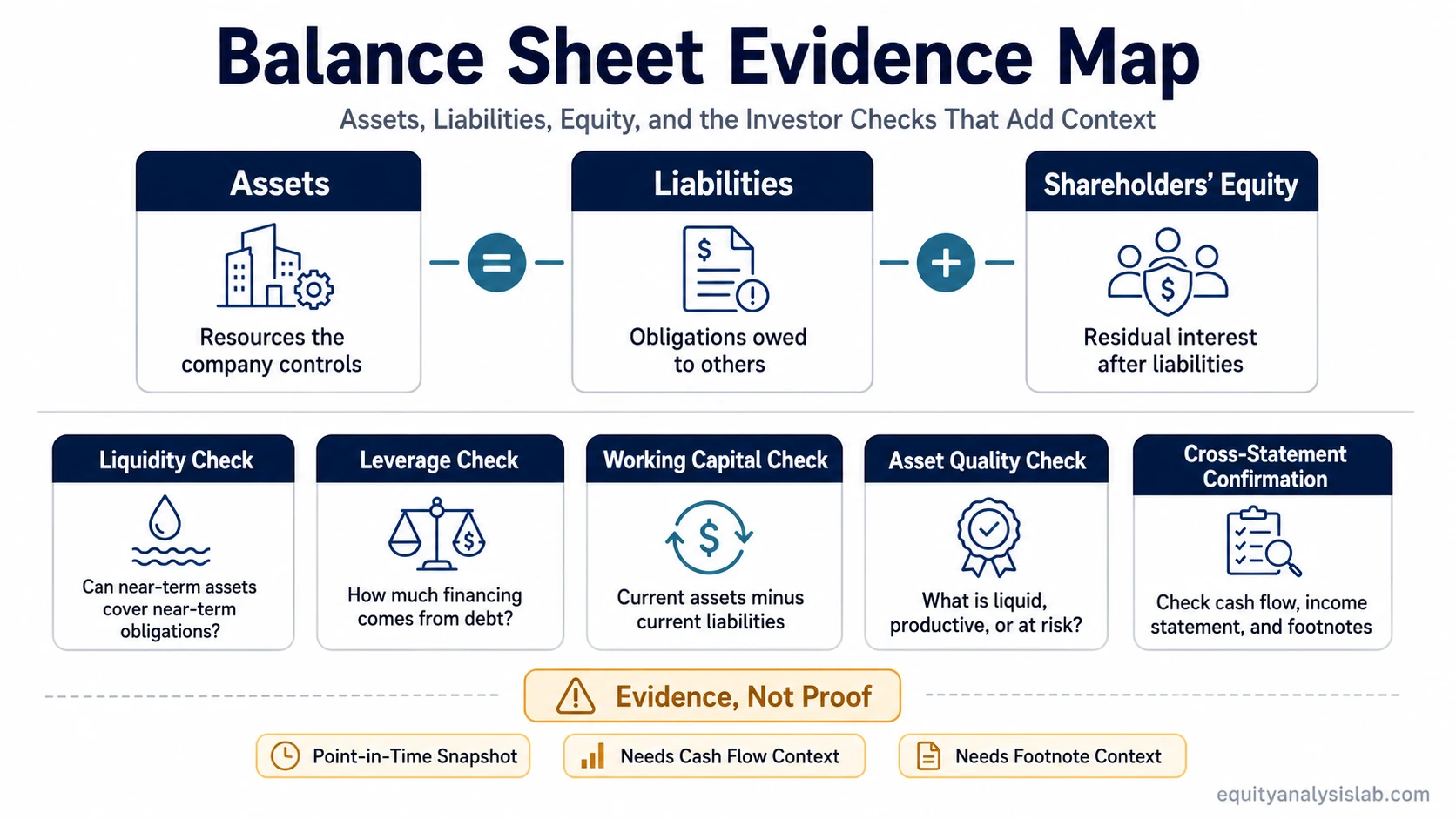

Key Points About a Balance Sheet

- A balance sheet is built around the accounting equation: assets equal liabilities plus shareholders’ equity.

- Assets show resources the company controls, liabilities show obligations, and equity shows the residual claim of shareholders.

- Current and long-term categories help investors separate near-term liquidity from longer-term financing and asset structure.

- A balance sheet is evidence, not proof. It can suggest financial strength or pressure, but it cannot confirm business quality, earnings durability, or cash conversion by itself.

What Is a Balance Sheet?

A balance sheet is one of the core financial statements used in company analysis. It summarizes a company’s financial position at a reporting date by separating resources, obligations, and shareholder claims into a structured statement.

The basic equation is:

Assets = Liabilities + Shareholders’ Equity

The equation means that every asset must be financed either by obligations to creditors or by capital attributable to shareholders. If a company has $500 million of assets and $300 million of liabilities, shareholders’ equity is $200 million. The equation balances because the resources controlled by the company must have a financing source.

The balance sheet usually appears in quarterly and annual reports. The reporting date matters because the statement does not show everything that happened during the full period. It shows the financial position at the end of that period.

What a Balance Sheet Shows

A balance sheet shows the composition of a company’s financial position. The most important reading is not only the total number for each category, but also the quality, timing, and change in those line items compared with prior periods.

| Balance sheet area | What it shows | Investor interpretation |

|---|---|---|

| Assets | Resources controlled by the company | Cash, receivables, inventory, property, goodwill, and other assets can indicate operating capacity, liquidity, and asset quality. |

| Liabilities | Obligations owed to creditors, suppliers, employees, lenders, or other parties | Debt, payables, leases, and other obligations help investors judge leverage, maturity risk, and financial flexibility. |

| Shareholders’ equity | The residual claim after liabilities are subtracted from assets | Equity can change through retained earnings, losses, share issuance, buybacks, dividends, and other capital structure movements. |

Current assets and current liabilities usually relate to amounts expected to convert into cash or come due within about one year or the normal operating cycle. Long-term assets and long-term liabilities relate to longer-duration resources and obligations. That classification helps investors separate short-term liquidity from longer-term capital structure.

Assets, Liabilities, and Equity

Assets can include cash, marketable securities, accounts receivable, inventory, property and equipment, goodwill, intangible assets, deferred tax assets, and other resources. Not all assets have the same quality. Cash is more immediately usable than inventory, and receivables depend on customer collection. Goodwill and intangible assets can be important, but they may also require extra judgment when business conditions change.

Liabilities can include accounts payable, accrued expenses, short-term debt, long-term debt, lease obligations, deferred revenue, pension obligations, and other commitments. The total liability number matters, but so does timing. A company with debt due soon can face different risk than a company with similar debt due much later. For deeper leverage interpretation, the related debt profile belongs in debt analysis rather than in the balance sheet alone.

Shareholders’ equity represents the accounting residual after subtracting liabilities from assets. It does not automatically equal market value. Equity can rise because of retained profits or share issuance, and it can fall because of losses, dividends, buybacks, or accumulated other comprehensive income. A rising equity balance can be useful evidence, but the source of the increase matters.

How Investors Read a Balance Sheet

Investors usually read a balance sheet by looking for changes in liquidity, leverage, working capital, asset quality, and financial flexibility. The useful question is not only whether the company has more assets than liabilities, but whether those assets are durable, liquid, collectible, and supported by cash generation.

| Question | Balance sheet evidence | Why it needs context |

|---|---|---|

| Can the company meet near-term obligations? | Cash, current assets, current liabilities, working capital | Working capital may look strong because receivables or inventory increased, not because cash improved. |

| Is leverage rising? | Short-term debt, long-term debt, lease obligations, total liabilities | Debt maturity, interest cost, covenant risk, and cash flow coverage change the interpretation. |

| Are assets high quality? | Receivables, inventory, goodwill, intangibles, restricted cash | Some assets depend on estimates, collection risk, resale value, or impairment assumptions. |

| Is the company financially flexible? | Cash, unused borrowing capacity, liability timing, capital structure | Flexibility depends on the company’s future cash needs, business cyclicality, and financing access. |

Working capital is one of the first balance sheet areas investors check because it connects operations to liquidity. A company may show revenue growth while tying up more cash in receivables or inventory. That is why the balance sheet should be read beside the cash flow statement, not as a stand-alone proof of financial strength.

Balance Sheet as Evidence, Not Proof

A balance sheet can show that a company has cash, low debt, or a large equity base, but it cannot prove that the company is a good investment. It does not show whether future earnings will grow, whether cash flow will remain durable, whether management will allocate capital well, or whether the stock price already reflects the financial position.

The balance sheet is strongest when it is used as evidence inside a broader company-analysis process. A large cash balance may be valuable, but its meaning depends on future cash needs, capital allocation, debt maturities, and operating performance. A high debt balance may be manageable if cash flows are stable and maturities are well spaced, but dangerous if profits are cyclical and refinancing risk is high.

What a Balance Sheet Cannot Establish Alone

- It does not confirm earnings quality without checking profitability and accruals.

- It does not establish cash conversion without reviewing operating cash flow and free cash flow.

- Asset quality still needs footnotes, aging schedules, inventory assumptions, impairment risk, and accounting estimates.

- Debt safety depends on interest cost, maturity timing, covenants, and refinancing conditions.

- It cannot prove investment attractiveness because valuation, business quality, risk, and expectations also matter.

Balance Sheet Checks and Related Statements

The balance sheet becomes more reliable when its line items are checked against related statements. A company story may sound strong, but cash-flow confirmation is needed before the interpretation becomes more dependable.

The cash flow statement helps show whether reported balance sheet strength is supported by actual cash movement. For example, rising receivables may support reported revenue, but weak cash collection can change the interpretation.

Profitability context from the company’s earnings statement helps explain why retained earnings, inventory, receivables, and tax-related balances may have changed. A balance sheet can show what changed, but period performance helps explain why it changed.

Free cash flow analysis can help investors judge whether accounting profits are turning into cash after operating and capital spending needs. That check is especially important when a company appears profitable but requires heavy reinvestment or shows persistent working-capital drag.

A Simple Balance Sheet Example

Consider a hypothetical company with $120 million in cash, $180 million in receivables and inventory, $300 million in long-term assets, $150 million in current liabilities, and $250 million in long-term liabilities.

| Category | Amount | Interpretation |

|---|---|---|

| Total assets | $600 million | Cash, operating assets, and long-term assets controlled by the company. |

| Total liabilities | $400 million | Current and long-term obligations owed to outside parties. |

| Shareholders’ equity | $200 million | The residual accounting claim after liabilities are subtracted from assets. |

The accounting equation balances because $600 million of assets equals $400 million of liabilities plus $200 million of equity. The example does not prove that the company is financially strong. Investors would still need to ask how much of the receivables will be collected, how quickly inventory turns into sales, when the liabilities come due, and whether the company converts earnings into cash.

Common Balance Sheet Mistakes

- Treating cash as automatically surplus: cash may be needed for operations, debt repayment, acquisitions, buybacks, dividends, or cyclical downturns.

- Ignoring restricted cash: some cash balances are not freely available for general corporate use.

- Reading book equity as market value: shareholders’ equity is an accounting measure, not a direct estimate of what the company is worth in the market.

- Overlooking receivable and inventory quality: rising current assets can be positive or negative depending on collection risk, demand, and inventory obsolescence.

- Ignoring footnotes: debt terms, lease obligations, contingencies, pension assumptions, and accounting estimates can materially change the interpretation.

FAQ

What is meant by balance sheet?

A balance sheet is a financial statement that shows a company’s assets, liabilities, and shareholders’ equity at a specific reporting date. It summarizes what the company owns, what it owes, and what remains for shareholders in accounting terms.

What is on a balance sheet?

A balance sheet contains assets, liabilities, and shareholders’ equity. Common line items include cash, receivables, inventory, property and equipment, goodwill, accounts payable, debt, leases, retained earnings, and other equity balances.

Why does the balance sheet have to balance?

The balance sheet balances because assets must be financed by either liabilities or shareholders’ equity. The equation is assets equal liabilities plus shareholders’ equity.

Is a strong balance sheet enough to make a stock attractive?

No. A strong balance sheet can be useful evidence, but it does not prove valuation, future earnings, cash conversion, capital allocation quality, or investment suitability. It should be interpreted with other statements and broader company analysis.