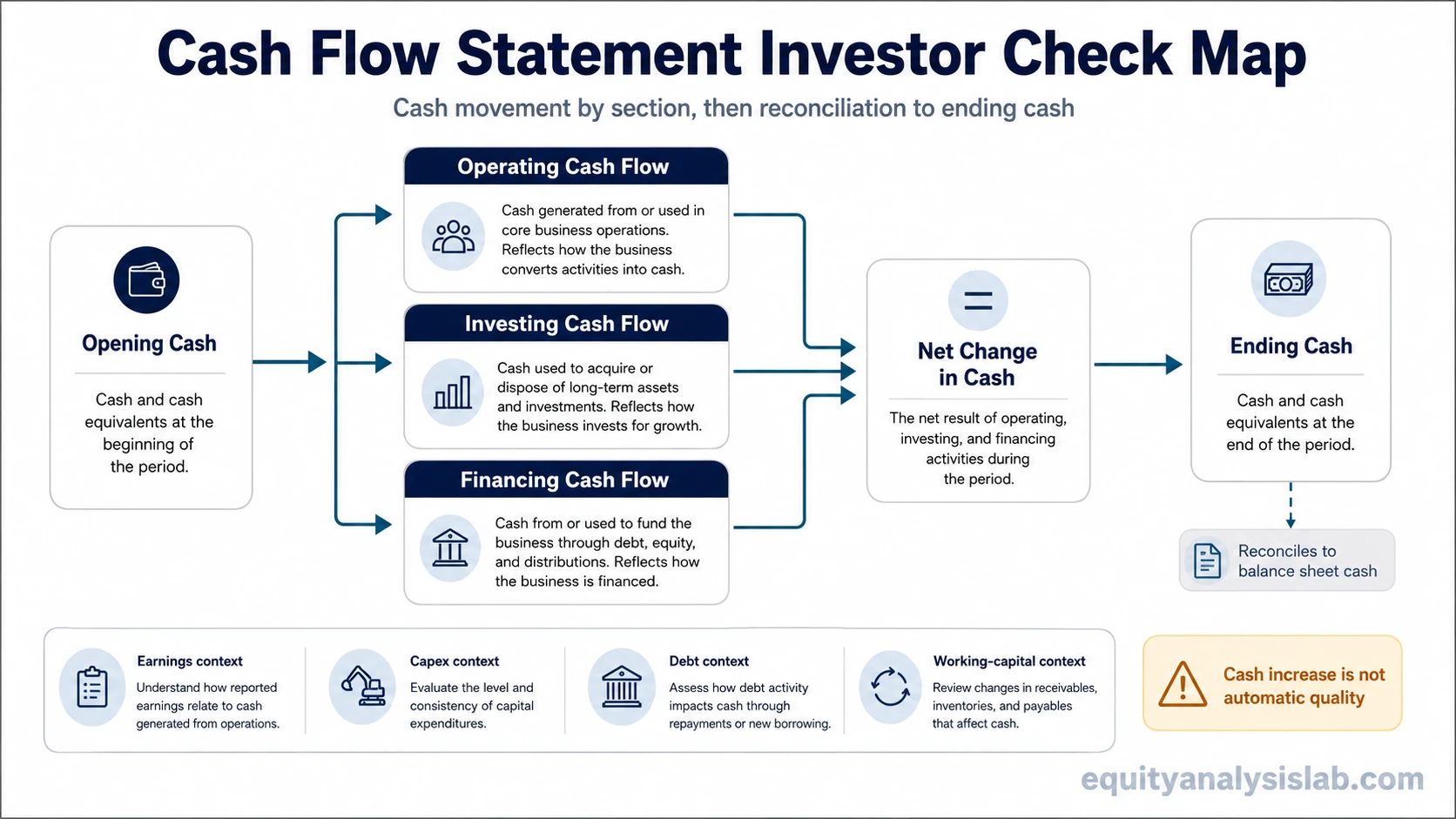

A cash flow statement shows how cash moved into and out of a company during a reporting period. It separates cash from operating, investing, and financing activities, which helps investors test whether reported performance is converting into cash. The statement is useful, but it is not a standalone verdict on business quality, valuation, or future returns.

Definition: A cash flow statement, also called a statement of cash flows, is a financial statement that reports cash inflows and cash outflows over a period and reconciles the change in cash from the beginning of that period to the end.

The cash flow statement is strongest as a cash-conversion check. It can show whether profit is supported by cash collections, whether investment spending is absorbing cash, and whether financing activity is filling the gap. The interpretation becomes more reliable when those cash movements are checked against accrual earnings, working capital, capital expenditure, and financing obligations.

Key Points

- A cash flow statement covers a reporting period, not one balance-sheet date.

- Operating, investing, and financing sections separate cash by source and use.

- The statement reconciles cash movement from opening cash to ending cash.

- Cash flow can differ from profit because accounting earnings use accrual rules.

- Positive total cash flow needs context from working capital, capex, debt, dividends, buybacks, and one-time items.

What Is a Cash Flow Statement?

A cash flow statement records actual cash movement during a reporting period. It answers a different question from profit: not how much accounting income was recognized, but how cash changed as the company operated, invested, borrowed, repaid, distributed, or raised capital.

The statement normally starts with opening cash, adds or subtracts net cash from operating, investing, and financing activities, and ends with closing cash. That ending cash balance should connect back to the cash and cash equivalents reported on the balance sheet.

In public-company reports, it usually appears with the core financial statements for the same reporting period as the income statement and balance sheet.

Statement name: “Cash flow statement” and “statement of cash flows” refer to the same financial statement. Public filings, annual reports, and accounting materials may use either label.

Where the Cash Flow Statement Fits With Other Financial Statements

The cash flow statement sits between the income statement and the balance sheet. The income statement records revenue, expenses, and profit under accrual accounting. The balance sheet reports assets, liabilities, and equity at one date. The cash flow statement explains how cash moved during the period between those balance-sheet dates.

This distinction matters because profit and cash can move differently. A company may recognize revenue before customers have paid, record expenses before cash leaves, or build inventory before it appears in sales. The cash flow statement helps separate accounting timing from cash collection and cash use.

| Statement | Main question answered | Timing lens | Cash-flow connection |

|---|---|---|---|

| Income statement | Did the company generate revenue and profit? | Reporting period | Profit may differ from cash because of accrual accounting. |

| Balance sheet | What did the company own, owe, and retain? | One reporting date | Cash balance should reconcile with the ending cash figure. |

| Cash flow statement | How did cash actually move? | Reporting period | Cash source and use are grouped into operating, investing, and financing activities. |

Operating, Investing, and Financing Cash Flows

The three sections of the cash flow statement classify cash by activity. The section matters because the same cash increase can come from operations, asset sales, borrowing, or share issuance.

| Cash flow section | What it shows | Investor check | Limitation |

|---|---|---|---|

| Operating activities | Cash generated or used by the core business, including cash collections, supplier payments, payroll, taxes, and working-capital movements. | Compare operating cash flow with net income to see whether earnings are converting into cash. | Operating cash flow can be temporarily lifted by collecting receivables, delaying payments, reducing inventory, or other working-capital timing effects. |

| Investing activities | Cash spent on or received from long-term assets, acquisitions, capital expenditure, asset sales, and investments. | Check whether cash use reflects reinvestment, maintenance needs, acquisitions, or asset sales. | Negative investing cash flow is not automatically weakness because capital expenditure may support future capacity or replacement needs. |

| Financing activities | Cash raised from or returned to capital providers, including debt issuance, debt repayment, share issuance, dividends, and buybacks. | Look at borrowing, repayment, dividends, and repurchases alongside debt obligations. | Positive financing cash flow can increase cash without improving operations, while repayments and distributions can reduce cash even when operations are healthy. |

Direct vs Indirect Method

The operating section can be presented using the direct method or the indirect method. The direct method lists major cash receipts and cash payments. The indirect method starts with net income and adjusts for non-cash items and working-capital changes.

Public-company filings often present operating cash flow using the indirect method. For investors, the key point is not to treat the method as a different statement. Both formats aim to explain cash from operations, but the indirect method makes the bridge from accrual profit to cash movement more visible.

Reading sequence: Start with the operating cash flow subtotal, then inspect the adjustments that explain why operating cash differed from net income.

How Investors Read a Cash Flow Statement

The cash flow statement becomes more useful when each section is tied to a specific interpretation question. Total cash movement is only the first layer. The source of the movement usually matters more than the headline number.

| Investor question | Where to look | What a stronger read may require | What can mislead the read |

|---|---|---|---|

| Is reported profit converting into cash? | Operating cash flow compared with net income. | Recurring operating cash generation supported by collections, margins, and stable working-capital behavior. | Temporary working-capital release, delayed payments, or one-time cash benefits. |

| Is cash being reinvested in the business? | Investing activities, especially capital expenditure and acquisitions. | Capex that makes sense relative to maintenance needs, growth plans, depreciation, and business model intensity. | Calling all negative investing cash flow “bad” without separating maintenance, growth, acquisitions, and asset purchases. |

| Is the company relying on outside financing? | Financing activities, including debt issuance, repayments, share issuance, dividends, and buybacks. | Financing activity that is consistent with leverage, maturity schedule, liquidity, and capital-allocation policy. | Positive cash flow driven mainly by new borrowing or share issuance rather than operations. |

| How much cash remains after reinvestment? | Operating cash flow and capital expenditure. | A separate free cash flow review that accounts for reinvestment needs. | Treating operating cash flow as fully available when the business requires heavy ongoing capex. |

| Did cash improve for a durable reason? | All three sections together. | Operating cash supported by core business activity, with investing and financing flows explained by strategy and balance-sheet context. | Asset sales, reduced investment, one-time collections, or financing inflows that lift cash temporarily. |

Cash Conversion and Accrual Earnings

Cash flow can test whether reported performance is turning into cash, but it still needs context from working capital, capex, financing, and accrual earnings. Strong reported profit with weak operating cash flow may indicate collection delays, inventory build, aggressive revenue recognition, or timing differences that need closer review.

The opposite can also happen. Operating cash flow may look strong because receivables were collected, payables increased, inventory fell, or a temporary working-capital release occurred. That does not automatically mean earnings quality improved. Recurring cash generation tied to core operations carries more weight than cash created by timing alone.

Common Cash Flow Statement Mistakes

Mistake: Treating positive total cash flow as proof that operations improved.

Positive net cash flow can come from borrowing, issuing shares, selling assets, reducing investment, or releasing working capital. Those sources can increase cash even when operating performance is weak or incomplete.

Limitation: The cash flow statement does not explain business quality by itself. Operating cash flow, capital expenditure, financing activity, and ending cash need to be read with profit, margins, balance-sheet strength, debt maturity, and reinvestment requirements.

A negative investing section can reflect useful reinvestment rather than weakness. A positive financing section can reflect necessary capital raising rather than strength. A positive operating section can still deserve caution if cash was lifted mainly by temporary working-capital movement. The statement is most useful when it separates those possibilities instead of forcing one conclusion.

Simple Cash Flow Statement Example

A company reports $50 million of net income, but operating cash flow is only $20 million because receivables rose during the period. Investing cash flow is negative $35 million because the company bought equipment, while financing cash flow is positive $40 million because it issued debt.

The ending cash balance may rise even though operations produced less cash than profit. The useful question is not whether cash increased, but which section supplied the cash, whether receivables later convert into collections, whether the equipment spending is maintenance or growth investment, and whether the added debt fits the balance sheet.

Related Cash Flow and Financial Statement Concepts

The cash flow statement explains the full movement of cash across operating, investing, and financing activities. Related measures narrow the lens.

- Operating cash flow: focuses on cash generated or used by core operations before isolating investing and financing activity.

- Free cash flow: narrows the question to cash remaining after capital expenditure or reinvestment needs.

- Income statement profit: shows accrual performance that may or may not convert into cash during the same period.

- Debt analysis: connects financing cash flows with obligations, maturity, interest burden, and balance-sheet risk.

FAQ

What does a cash flow statement show?

A cash flow statement shows how cash moved into and out of a company during a reporting period. It classifies cash movement into operating, investing, and financing activities and reconciles the change in cash.

Why can cash flow differ from profit?

Cash flow can differ from profit because income statements use accrual accounting. Revenue, expenses, receivables, payables, inventory, depreciation, and other non-cash or timing items can make profit and cash move differently.

Is positive cash flow always good?

Positive cash flow is not automatically good. Cash can increase because of borrowing, share issuance, asset sales, working-capital timing, or reduced investment, not only because operations improved.

What are the three sections of a cash flow statement?

The three sections are operating activities, investing activities, and financing activities. Operating activities relate to core business cash movement, investing activities relate to long-term assets and investments, and financing activities relate to capital providers.