Free cash flow is the cash a company generates after subtracting capital expenditures from operating cash flow. It shows how much cash remains after the business funds its operations and invests in its asset base, but it does not by itself prove business quality, valuation attractiveness, or future returns.

The basic relationship is simple: free cash flow starts with operating cash generation and then removes the cash spent on property, equipment, software, facilities, or other long-lived assets. The number is useful because it connects earnings, reinvestment, liquidity, and financial flexibility to actual cash movement.

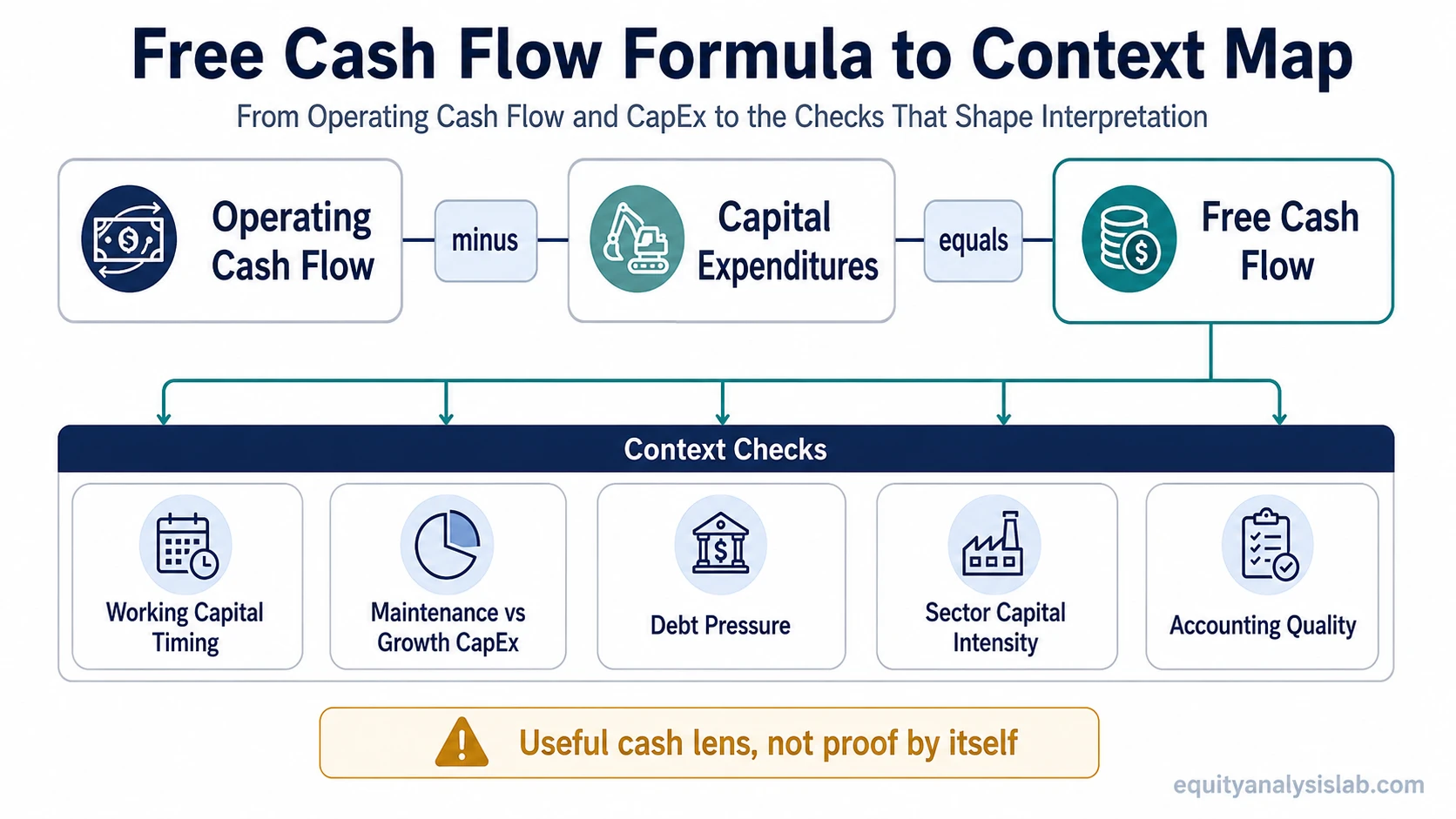

Key Points

- Free cash flow usually equals operating cash flow minus capital expenditures.

- It helps show cash generation after operations and asset investment.

- Positive free cash flow can support flexibility, but it is not proof of investment quality by itself.

- Interpretation depends on working capital, reinvestment needs, debt, sector context, and accounting quality.

What Is Free Cash Flow?

Free cash flow measures cash left after a company covers operating activity and capital expenditures. In practical financial-statement work, it is an investor-facing cash conversion measure: it asks what cash remains after the business has produced operating cash and funded the asset investment needed to keep operating or expand.

That makes free cash flow different from accounting earnings. Net income can include non-cash expenses, accruals, timing estimates, and accounting judgments. Free cash flow focuses on cash movement after CapEx, so it can help show whether reported profit is supported by cash that remains available after investment needs.

Free Cash Flow Formula

Free Cash Flow = Operating Cash Flow – Capital Expenditures

Operating cash flow is usually taken from the operating section of the cash flow statement. Capital expenditures are usually found in the investing section, often as purchases of property, plant, equipment, or similar long-lived assets.

Free cash flow is not always presented as a single standardized GAAP or IFRS line item. Some companies or data providers show it directly, but analysts often calculate it from reported statement inputs. The calculation should therefore be checked against the filing, not treated as a number that always appears in the same place or with the same label.

Because FCF starts from operating cash flow, it should not be read as a replacement for that operating cash measure. It is a post-CapEx measure that answers a narrower question: how much cash remains after the company funds operating activity and reinvests in the asset base.

Free Cash Flow Example

Assume a company reports $500 million in operating cash flow and $180 million in capital expenditures.

| Input | Amount |

|---|---|

| Operating cash flow | $500 million |

| Capital expenditures | $180 million |

| Free cash flow | $320 million |

The arithmetic is $500 million minus $180 million, which equals $320 million of free cash flow. That result does not automatically mean the company is attractive. The interpretation depends on reinvestment needs, working-capital timing, sector capital intensity, balance sheet pressure, and whether the cash generation is repeatable.

What Free Cash Flow Tells Investors

Free cash flow can help investors evaluate how much financial flexibility remains after a company has funded operations and invested in its asset base. Cash generation becomes more informative after asking what the company had to spend to produce it and what obligations still compete for that cash.

When free cash flow is durable, management may have more flexibility to reinvest in the business, reduce debt, hold cash, pay dividends, or repurchase shares. Those are possible uses of cash, not guaranteed outcomes. A company can generate free cash flow and still face weak growth, heavy refinancing needs, poor capital allocation, or valuation risk.

Free cash flow also helps separate reported profitability from cash conversion. A company with strong accounting earnings but weak free cash flow may be investing heavily, experiencing working-capital pressure, or relying on accruals that do not yet translate into cash.

What Free Cash Flow Can and Cannot Tell You

| Free cash flow can help show | Free cash flow cannot prove by itself |

|---|---|

| Cash left after operating cash flow and CapEx | That the stock is undervalued or attractive |

| Potential flexibility for reinvestment, debt reduction, dividends, or buybacks | That management will allocate cash well |

| Whether reported earnings have some cash support | That earnings quality is strong in every period |

| How capital intensity affects cash generation | That low CapEx is always a positive signal |

| Whether cash generation appears stable across multiple periods | That future free cash flow will continue at the same level |

What Free Cash Flow Can Hide

Free cash flow can look stronger or weaker because of timing. A temporary working-capital benefit, delayed supplier payments, lower inventory purchases, or unusual collections can improve operating cash flow for a period without showing a permanent improvement in the business.

CapEx timing can also distort the number. A company may report high free cash flow in a year when it delays investment, then report lower free cash flow when deferred spending returns. The distinction between maintenance CapEx and growth CapEx matters because underinvestment can make current free cash flow look better while weakening future competitiveness.

Sector context is critical. Capital-light software businesses, retailers, manufacturers, utilities, telecom companies, and commodity producers can have very different normal free cash flow patterns. A low or negative FCF number may be routine during an investment cycle, while a high number may be less impressive if the business is shrinking or deferring necessary asset spending.

Free cash flow should also be checked against accounting quality. A company can show positive free cash flow while still facing revenue-recognition questions, margin pressure, stock-based compensation dilution, refinancing needs, or other issues that require deeper statement review.

Free Cash Flow vs Profit and Operating Cash Flow

Profit, operating cash flow, and free cash flow answer different questions. Profit or net income measures accounting earnings after expenses, taxes, and accounting judgments. Operating cash flow measures cash generated from the company’s operations before subtracting capital expenditures.

Free cash flow goes one step further by subtracting CapEx. That makes it more focused on cash remaining after asset investment, but also more sensitive to reinvestment timing and capital intensity. It should not replace the income statement or the operating section of the cash flow statement; it adds a post-CapEx lens to the analysis.

FCFF and FCFE are related valuation concepts, but they are not the same as the simple free cash flow measure used here. Those variants adjust the cash-flow lens for capital-structure and valuation-model purposes, so they belong in a more specific valuation discussion rather than the core definition of free cash flow.

How to Check Free Cash Flow in Context

Free cash flow is most useful when it is checked across several periods rather than judged from one year. A single strong year can reflect working-capital timing, delayed CapEx, or a temporary cash benefit. A single weak year can reflect heavy investment rather than business deterioration.

The balance sheet helps show whether free cash flow is large enough relative to cash needs, leverage, maturities, and liquidity. A company with positive FCF may still have limited flexibility if debt obligations or refinancing pressure absorb much of the available cash.

Free cash flow should also be reviewed alongside reinvestment requirements and debt obligations. When a business needs constant asset spending to remain competitive, the headline FCF number can overstate flexibility if maintenance investment is being deferred.

A practical review usually asks five questions: whether operating cash flow is repeatable, whether CapEx is normal or unusually low, whether working capital helped or hurt the period, whether debt and liquidity create pressure, and whether the company’s sector normally requires heavy reinvestment.

| Check | What it helps clarify |

|---|---|

| Operating cash flow trend | Whether cash generation is recurring or volatile |

| CapEx level | Whether reinvestment needs are heavy, light, deferred, or unusually high |

| Working capital movement | Whether cash flow is helped or hurt by timing |

| Debt and liquidity | Whether FCF is enough to support obligations and refinancing needs |

| Sector capital intensity | Whether “low” or “high” FCF is normal for the business model |

Free Cash Flow FAQ

Is free cash flow the same as profit?

No. Profit usually refers to accounting earnings, while free cash flow measures cash remaining after operating cash flow and capital expenditures. A company can report profit while producing weak free cash flow, or generate strong cash flow during a period when accounting earnings are affected by non-cash items.

Is free cash flow the same as operating cash flow?

No. Operating cash flow measures cash generated from operations before capital expenditures. Free cash flow subtracts CapEx, so it focuses on cash remaining after the business invests in long-lived assets.

Is negative free cash flow always bad?

No. Negative free cash flow can reflect heavy investment, working-capital timing, or a temporary capital-spending cycle. It becomes more concerning when weak cash generation persists, debt pressure rises, or investment spending does not support future business strength.

Does high free cash flow mean a stock is undervalued?

No. High free cash flow can be useful, but valuation depends on expectations, durability, growth, risk, capital allocation, balance sheet strength, and the price investors pay for the cash flow stream.