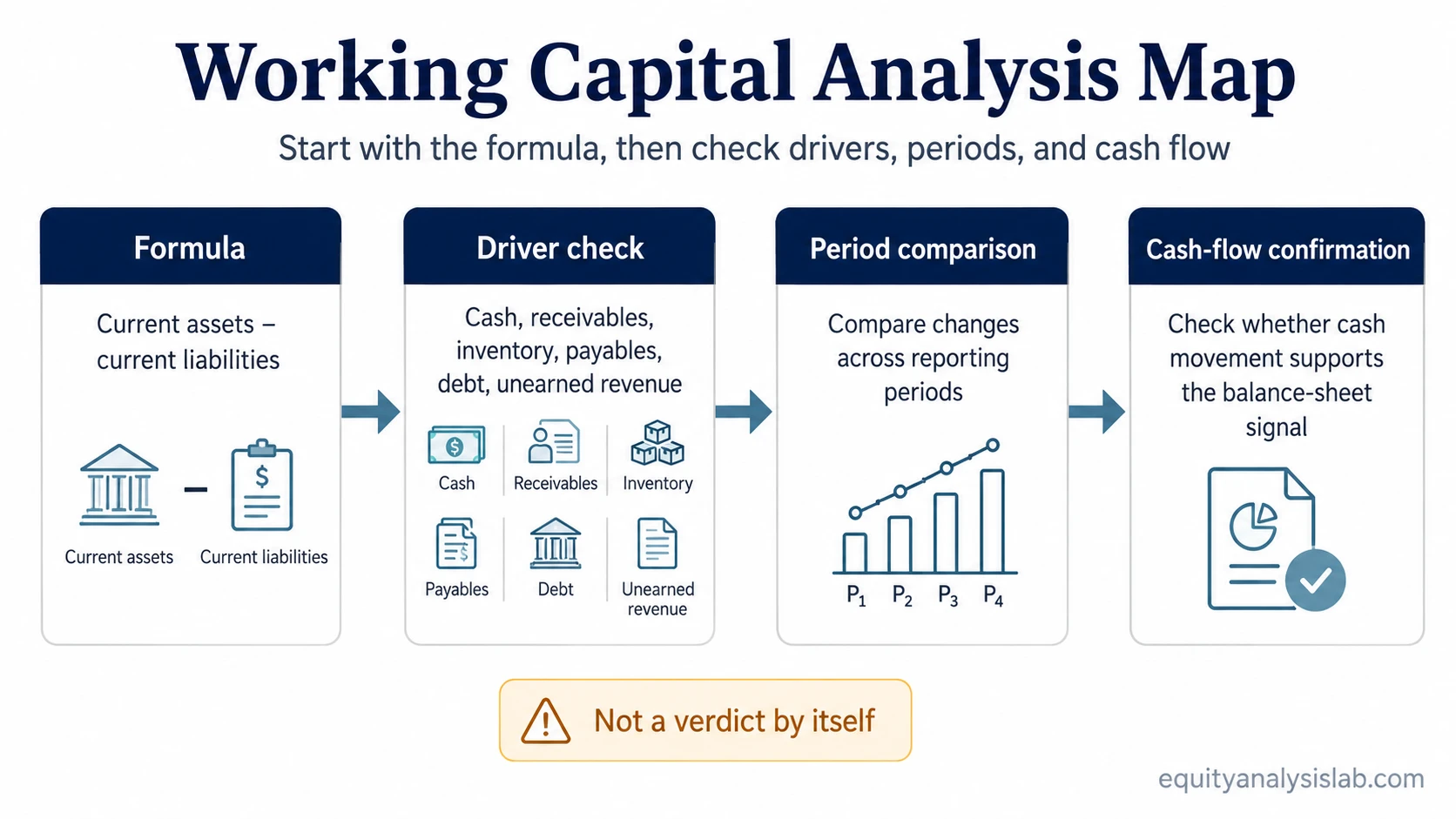

Working capital analysis starts with current assets minus current liabilities, but the useful investor question is not only whether the number is positive or negative. The useful question is what changed, why it changed, and whether cash movement confirms the balance-sheet signal.

Working capital formula: working capital = current assets − current liabilities.

Current assets are resources expected to turn into cash or be used within the normal operating cycle. Current liabilities are obligations expected to be settled within the same short-term window. The formula gives the starting point; the analysis comes from the drivers behind the number.

Key points for working capital analysis

- Working capital comes from current assets minus current liabilities.

- The driver matters more than the headline number.

- Compare at least two periods before interpreting the change.

- Check whether the working-capital story is supported by cash movement.

Working capital analysis starts with the formula, but not the verdict

A positive working-capital balance means current assets exceed current liabilities. A negative balance means current liabilities exceed current assets. Neither result is automatically good or bad for an investor.

A company can report positive working capital because it holds cash and collects from customers quickly. It can also report positive working capital because receivables are growing faster than sales or inventory is building ahead of demand. Those situations carry different meanings even when the formula points in the same direction.

Negative working capital also needs context. It can point to liquidity pressure, but it can also appear in businesses that collect cash before delivering products or services. The analysis should move from the formula to the line items before reaching a conclusion.

Where working capital comes from in the financial statements

Working capital comes from the current section of the balance sheet. Current assets usually include cash, receivables, inventory, and prepaid expenses. Current liabilities usually include payables, accrued expenses, short-term debt, and customer advances or unearned revenue.

The balance-sheet location matters because working capital is a stock measure at one reporting date. It shows what the company owns and owes at that point in time. It does not show whether cash was generated during the period.

Which working-capital line item changed?

The strongest working-capital analysis starts by asking which line item moved. A higher working-capital number created by more cash is different from a higher number created by slower receivable collection or excess inventory. A lower number caused by supplier credit is different from a lower number caused by rising short-term debt.

| Line item | Working-capital side | Investor interpretation question |

|---|---|---|

| Cash and cash equivalents | Current asset | Did liquidity improve, or is cash temporarily elevated before a known obligation? |

| Accounts receivable | Current asset | Are customers paying on time, or are sales being booked before cash is collected? |

| Inventory | Current asset | Is inventory supporting future sales, or is product building faster than demand? |

| Prepaid expenses | Current asset | Is the asset a normal operating prepayment, or is it too small to change the investment read? |

| Accounts payable | Current liability | Is the company using normal supplier terms, or stretching payments to preserve cash? |

| Accrued expenses | Current liability | Are ordinary expenses timing through the balance sheet, or are obligations building unusually? |

| Short-term debt | Current liability | Does the company face near-term refinancing or repayment pressure? |

| Unearned revenue | Current liability | Is the company receiving customer cash upfront, or does the liability create future delivery obligations? |

This driver-based view prevents the headline number from doing too much work. Cash, receivables, inventory, payables, and unearned revenue can each change the same total while pointing to different operating conditions.

Why positive or negative working capital can mislead

Common misread: positive working capital means the company is financially strong, and negative working capital means the company is weak.

Safer interpretation: the sign of working capital is only a first clue. Positive working capital can still hide slow receivables, inventory buildup, or weak cash conversion. Negative working capital can sometimes reflect customer prepayments, efficient supplier terms, or a business model that receives cash before recognizing revenue.

A useful interpretation separates liquidity from operating timing. If receivables and inventory are rising faster than revenue, the company may be tying up more cash in operations. If payables are rising faster than purchases or cost of goods sold, the company may be preserving cash by delaying payment. Those details matter more than the direction of the total.

Compare working capital across periods

A single reporting period can be misleading. Working capital should be compared across at least two periods, and preferably across comparable seasonal periods when the business has seasonal sales or inventory patterns.

The basic trend question is simple: did working capital rise or fall, and which line item explains the move? The better follow-up is whether the change fits the business context. A retailer may build inventory before a major selling season. A software company may show higher unearned revenue when customers pay upfront. A manufacturer may show higher receivables if customers are taking longer to pay.

| Change observed | Possible interpretation | What to check next |

|---|---|---|

| Receivables rise faster than revenue | Sales may not be converting into cash as quickly. | Customer collection timing, allowance for doubtful accounts, and operating cash flow. |

| Inventory rises faster than sales | Demand may be slower than production or purchasing. | Inventory turnover, markdown risk, and management commentary. |

| Payables rise sharply | The company may be using supplier financing or delaying cash outflows. | Days payable, supplier concentration, and whether the pattern is recurring. |

| Unearned revenue rises | Customers may be paying before revenue is recognized. | Future delivery obligations and whether upfront cash is repeatable. |

Cross-check working capital against cash flow

The working-capital story should be checked against cash movement, not read only from the headline balance-sheet number. The cash flow statement shows how changes in receivables, inventory, payables, and other operating items affected cash from operations during the period.

If net income looks strong but operating cash flow is weak, working capital may explain part of the gap. Receivables may have increased because customers have not paid yet. Inventory may have absorbed cash before products were sold. Payables may have temporarily helped cash flow if the company delayed supplier payments.

Cash-flow rule of thumb: increases in receivables or inventory usually use cash; increases in payables usually delay cash outflow.

Cash-conversion measures can help organize that review. Days sales outstanding, days inventory outstanding, days payable outstanding, and the cash conversion cycle are not required for every quick analysis, but they can show whether cash is being collected, stored in inventory, or delayed through supplier payments. The goal is to test whether accounting profit is becoming cash.

This is also where working capital connects to cash remaining after capital expenditures. A company can report profit, but if receivables and inventory absorb cash before capital spending is considered, the free-cash-flow picture can look different from the income-statement picture.

Illustrative example: similar profit, different cash timing

Consider two hypothetical companies that each report $10 million of operating profit.

Company A collects most customer payments quickly, keeps inventory stable, and pays suppliers on normal terms. Its profit is more likely to show up in operating cash flow because fewer dollars are tied up in receivables or inventory.

Company B reports the same profit, but receivables rise by $6 million and inventory rises by $4 million while payables increase by only $1 million. The income statement still shows profit, but cash is being absorbed by working capital.

In that simplified case, the working-capital movement absorbs $9 million of cash before other operating adjustments: $6 million tied up in receivables plus $4 million tied up in inventory, partly offset by $1 million of additional payables.

The example does not prove that Company B is a poor business. It shows why working capital analysis should move from the headline formula to the drivers and then to cash-flow confirmation.

What working capital cannot prove alone

Working capital cannot prove valuation attractiveness, future returns, business quality, or solvency by itself. It is one financial-statement signal that needs context from revenue growth, margins, debt maturity, cash flow, capital expenditure needs, industry structure, and the company’s operating model.

A high working-capital balance may be useful if it reflects cash strength and disciplined collection. It may be less attractive if it reflects stale inventory or slow customer payments. A low or negative balance may be risky if near-term obligations exceed available resources. It may be less concerning if customer prepayments are normal and repeatable.

The practical investor checklist is: calculate the number, identify the driver, compare periods, test the cash-flow effect, and avoid treating the headline balance as a complete conclusion.

FAQ

Why is the working-capital formula not enough by itself?

The formula shows current assets minus current liabilities, but it does not explain which line item changed or whether the change helped or hurt cash conversion. The driver behind the number matters more than the headline total.

Can negative working capital ever be healthy?

Yes, in some business models. Negative working capital can be less concerning when customers pay upfront and the company can meet future delivery obligations without near-term liquidity pressure.

How does working capital affect cash flow?

Working-capital changes affect operating cash flow because receivables, inventory, payables, and related items change when cash is collected, spent, delayed, or received in advance.