Free cash flow vs operating cash flow separates cash generated by core business operations from cash left after capital expenditures. They are related, but they are not the same metric: operating cash flow comes before the capex adjustment, while free cash flow reflects what remains after that adjustment.

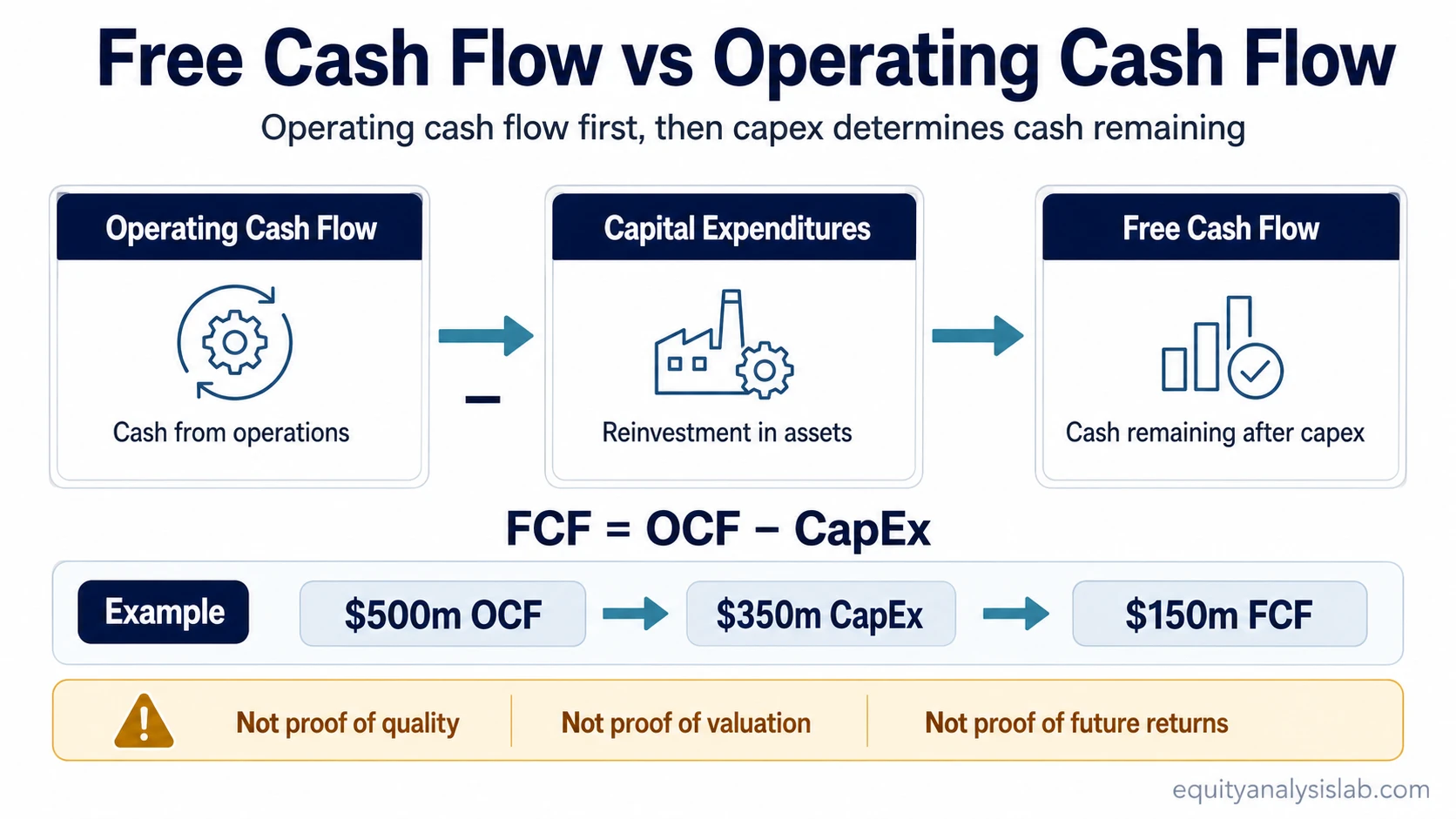

Formula boundary: Free Cash Flow = Operating Cash Flow − Capital Expenditures.

The distinction matters because a company can report strong operating cash flow while leaving much less cash available after reinvestment in property, equipment, technology, stores, factories, or other long-lived assets.

The Core Difference

Operating cash flow focuses on cash generated by the company’s normal business activities. It helps test whether reported earnings are supported by actual operating cash movement.

Free cash flow goes one step further by subtracting capital expenditures from operating cash flow. It estimates how much cash remains after the business funds investment needed to maintain or expand its asset base.

Short distinction: Operating cash flow answers “is the business generating cash from operations?” Free cash flow answers “how much cash remains after required or chosen reinvestment?”

Free Cash Flow vs Operating Cash Flow Comparison

| Comparison point | Operating cash flow | Free cash flow |

|---|---|---|

| Starting point | Cash flow from operating activities. | Operating cash flow after subtracting capital expenditures. |

| What it measures | Cash generated by the company’s core operations. | Cash left after operating cash generation and capital investment needs. |

| Capex treatment | Does not subtract capital expenditures. | Subtracts capital expenditures directly. |

| Investor question answered | Are operations converting into cash? | How much cash remains after reinvestment? |

| What it can miss | Heavy reinvestment needs, maintenance capex, or growth capex burden. | Temporary investment cycles, uneven capex timing, or growth spending that may be economically productive. |

| Best use | Testing operating cash generation, earnings support, and working-capital effects. | Assessing post-capex flexibility, reinvestment burden, and potential capital allocation capacity. |

How the Formula Connects Them

Free cash flow is commonly calculated from operating cash flow by subtracting capital expenditures; it is a derived cash-flow measure rather than a required standalone financial-statement section. Operating cash flow comes first, then capex is subtracted to estimate cash remaining after reinvestment.

Formula: FCF = OCF − CapEx.

If operating cash flow rises but capex rises faster, free cash flow can still fall. If operating cash flow is stable and capex declines after a heavy investment period, free cash flow can improve without a major change in operating cash generation.

Cash-flow metrics should test the business narrative rather than replace full company analysis. A growing company may need heavy investment, while a mature company may convert a larger share of operating cash into free cash flow.

Same-Company Example

A company reports $500 million of operating cash flow during the year. It also spends $350 million on capital expenditures to maintain facilities, expand capacity, and support future operations.

| Metric | Illustrative amount | Interpretation |

|---|---|---|

| Operating cash flow | $500 million | The core business generated positive cash from operations. |

| Capital expenditures | $350 million | A large share of operating cash was absorbed by reinvestment. |

| Free cash flow | $150 million | Cash remained after capex, but much less than operating cash flow alone suggested. |

Those numbers do not imply that the company is strong, weak, cheap, expensive, or attractive. They only show why operating cash flow and free cash flow can support different readings of the same business.

The Common Confusion Trap

Common mistake: Strong operating cash flow is not the same as abundant cash available for debt reduction, dividends, buybacks, acquisitions, or valuation support. Capital expenditures can absorb a large share of the cash generated by operations.

Weak or negative free cash flow also needs context. FCF can be pressured when a company is deliberately reinvesting in capacity, distribution, technology, or long-term growth. The interpretation depends on business model, industry structure, capital intensity, and whether reinvestment appears economically productive.

When Each Metric Is More Useful

Operating cash flow is the better starting point when the question is operating conversion. It helps assess whether revenue and earnings are turning into cash, whether working capital is absorbing or releasing cash, and whether reported profitability has cash support.

Free cash flow is the better starting point when the question is post-capex flexibility. It helps show how much cash remains after the business funds capital expenditures, which can matter for debt reduction, dividends, repurchases, acquisitions, or balance-sheet flexibility.

Use OCF first when analyzing operating cash generation, earnings support, or working-capital effects.

Use FCF first when analyzing reinvestment burden, capex intensity, or cash remaining after the asset base has been funded.

Diagnostic Questions for Investors

| Diagnostic question | Operating cash flow | Free cash flow |

|---|---|---|

| Is the core business generating cash? | Stronger fit. | Secondary, because it starts after operating cash flow. |

| How much cash remains after capex? | Incomplete without capex. | Stronger fit. |

| Does reinvestment absorb operating cash? | Needs a capex check. | Directly visible. |

| Can the metric be distorted by timing? | Yes, especially through working-capital timing. | Yes, especially through capex cycles or investment timing. |

| Does the metric prove company quality? | No. It is one evidence point. | No. It is one evidence point. |

Limitations of Both Metrics

Operating cash flow limitation: OCF can look healthy while a business still requires heavy capital spending to maintain or grow its asset base.

Free cash flow limitation: FCF can be volatile when capital expenditures are lumpy, cyclical, or concentrated in a growth-investment period.

Neither metric alone proves business quality, undervaluation, financial strength, or future stock returns. A stronger cash-flow reading usually comes from comparing OCF, FCF, capex needs, working-capital behavior, debt obligations, margins, and the business model behind the numbers.

How to Read Them Together

Start with operating cash flow to test whether the business is producing cash from operations. Then compare capital expenditures with operating cash flow to see how much of that cash is required for reinvestment.

The stronger combined reading is not simply “high OCF and high FCF.” The better question is whether operating cash generation, reinvestment needs, and business economics make sense together. A capital-light company and a capital-intensive company can show very different OCF-to-FCF conversion patterns without requiring the same interpretation.

Practical boundary: OCF is closer to operating conversion. FCF is closer to post-capex flexibility. Both need context before they can support an investor judgment.

FAQ

Are free cash flow and operating cash flow the same?

No. Operating cash flow measures cash generated by core operations. Free cash flow starts with operating cash flow and subtracts capital expenditures.

Why can operating cash flow be higher than free cash flow?

Operating cash flow can be higher because it does not subtract capital expenditures. When capex is significant, free cash flow can be much lower than operating cash flow.

Is free cash flow always better for investors than operating cash flow?

No. Free cash flow is useful for post-capex flexibility, but operating cash flow is still important for understanding operating cash generation and working-capital effects.