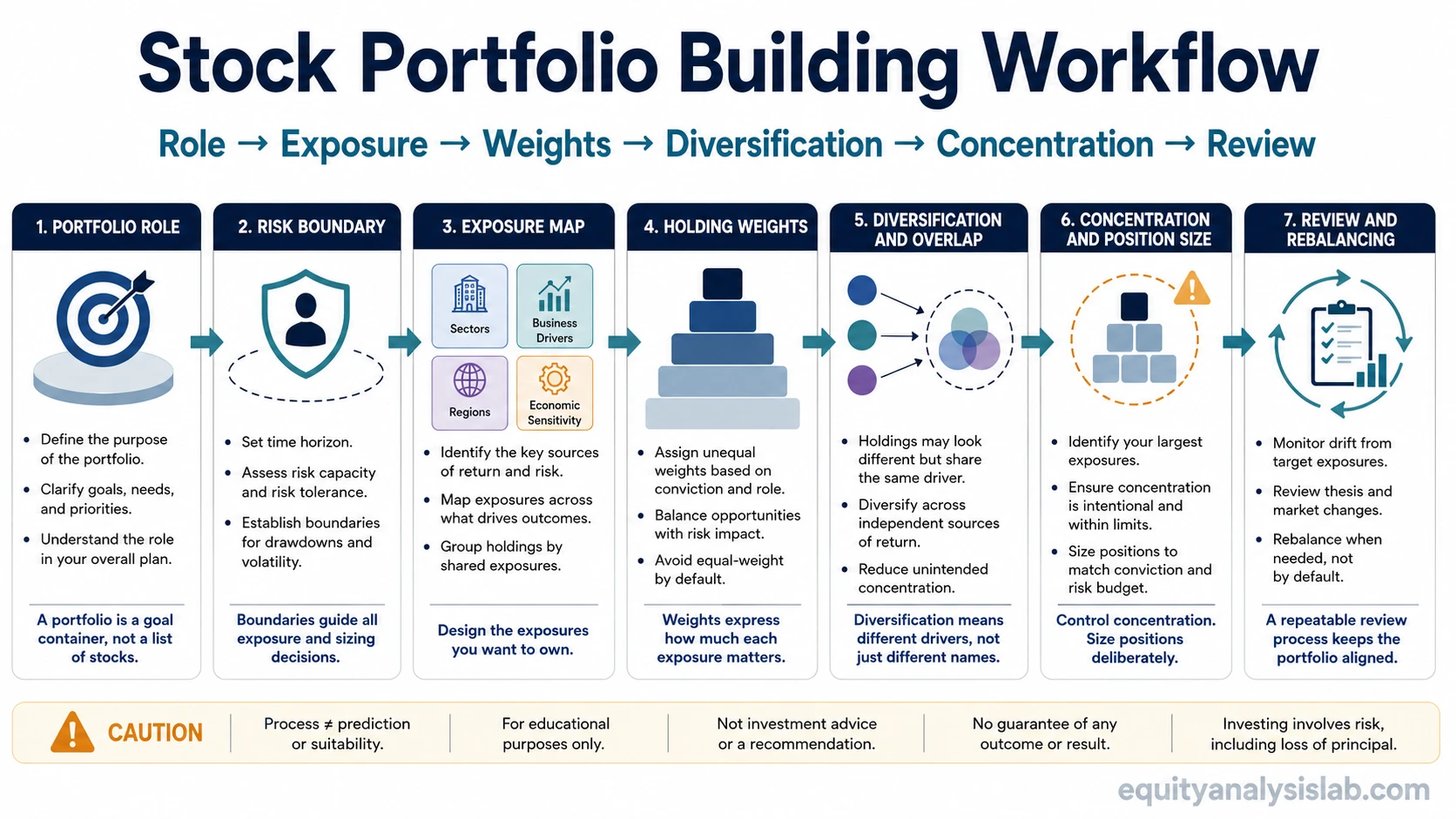

To build a stock portfolio, start by defining the role the portfolio should play, then map that role into exposure, weights, diversification, concentration limits, position sizing, and a repeatable review process.

A stock portfolio is not just a list of companies. It is a collection of exposures. Two investors can own the same number of stocks and still carry very different risks if their weights, sectors, business drivers, or review rules are different.

This is an educational framework for organizing portfolio decisions. It does not determine whether a specific stock, allocation, or risk level is suitable for any individual investor.

Key Points

- Portfolio construction begins with purpose, time horizon, and risk capacity before individual stock selection.

- Weights turn a stock list into real exposure because larger positions drive more of the portfolio result.

- Diversification depends on what the holdings are exposed to, not only how many names appear in the account.

- Concentration can be intentional, accidental, or hidden through overlapping business drivers.

- Rebalancing is a review discipline for drift, not a prediction tool.

What Building a Stock Portfolio Actually Means

Building a stock portfolio means deciding how ownership risk will be spread across companies, sectors, business models, regions, and position sizes. The process starts with portfolio role and exposure design, then moves into individual stock selection.

The first question is not “which stock should be bought first?” A more useful first question is what kind of exposure the portfolio is supposed to hold. That includes how much of the overall investment plan belongs in stocks, how much risk the investor can absorb, and how long the capital can remain exposed to equity volatility.

That first structural decision connects to the wider mix of assets, cash needs, and time-horizon constraints before individual company analysis begins.

The Main Decisions Before Choosing Stocks

Stock selection comes after the portfolio frame is clear. Without that frame, a collection of individually reasonable companies can still become an unbalanced portfolio.

| Decision | Question to Resolve | Why It Changes the Portfolio |

|---|---|---|

| Portfolio role | What job should the stock portfolio perform? | Separates long-term ownership exposure from short-term speculation or cash-reserve needs. |

| Time horizon | How long can the capital stay exposed? | A longer horizon may allow more tolerance for interim price swings, while a shorter horizon usually limits how much volatility can be absorbed. |

| Risk capacity | How much loss or drawdown could be handled without forcing a bad decision? | Prevents the portfolio from being built around confidence alone. |

| Exposure mix | Which sectors, business types, and economic drivers should be represented? | Determines whether the portfolio is broad, narrow, defensive, cyclical, growth-heavy, income-oriented, or concentrated. |

| Position weights | How large should each holding be relative to the whole portfolio? | Turns a watchlist into an actual exposure map. |

| Review rule | When should drift, concentration, or thesis change be reviewed? | Keeps the portfolio from changing silently as prices and business conditions move. |

How Weights and Overlap Shape Real Exposure

Weights determine which holdings matter most. A small position may add research interest, but a larger position drives more of the portfolio’s risk and return behavior. Position weights should therefore be treated as part of the construction process, not as an afterthought.

Overlap creates a second layer of exposure. Several companies may look separate by name while still depending on similar customer demand, interest-rate conditions, commodity inputs, technology spending, or economic cycles. A portfolio can therefore look diversified by holding count while remaining exposed to one dominant driver.

Concentration is more than a question of how many stocks are owned. A portfolio may be concentrated because one position is very large, because several holdings share the same sector, or because different sectors still depend on the same economic condition.

A Simple Hidden-Concentration Example

A portfolio may contain companies from several ticker names while many of those businesses still depend on the same growth factor, customer group, financing condition, or spending cycle. If those shared drivers weaken together, the portfolio may behave less diversified than the holding count suggested.

The practical issue is not that concentrated exposure is always wrong. The issue is whether the concentration is visible, intentional, and sized in a way that can survive adverse conditions without forcing a poorly timed decision.

Diversification Is Exposure Design, Not a Stock Count

Diversified stock exposure means spreading risk across holdings that do not all depend on the same outcome. More holdings can help, but the number of holdings alone does not prove that risk is spread well.

A stronger diversification check asks what would hurt the portfolio if conditions changed. If the same interest-rate move, commodity shock, earnings cycle, sector downturn, or valuation reset would pressure most holdings at once, the portfolio may be less diversified than it appears.

Stock selection still matters. Company quality, valuation, balance-sheet strength, cash-flow durability, and business model risk can all affect whether a holding deserves a place. But those company-level checks work best after the portfolio’s exposure map is clear.

Portfolio Concepts to Review Next

Once the broad workflow is clear, the deeper work is to separate each portfolio-construction decision and review it on its own terms.

| Concept | Portfolio Question | Use in the Workflow |

|---|---|---|

| Asset allocation | How much of the wider plan should be exposed to stocks? | Sets the broad stock-versus-non-stock boundary before individual holdings are selected. |

| Concentration | Which positions or shared drivers dominate portfolio behavior? | Identifies whether risk is intentionally focused or accidentally clustered. |

| Diversification | Are risks spread across genuinely different exposures? | Tests whether the portfolio depends on several independent drivers or one dominant theme. |

| Position sizing | How much should each holding affect the total portfolio? | Connects conviction, uncertainty, downside tolerance, and portfolio impact. |

| Portfolio review and rebalancing | When should drift, overweight exposure, or thesis change be addressed? | Keeps the portfolio aligned with the intended structure as prices and fundamentals change. |

A Beginner Mistake Map

| Mistake | Why It Creates Risk | Cleaner Check |

|---|---|---|

| Starting with favorite stocks | The portfolio may become a collection of ideas without a clear exposure structure. | Define portfolio role, time horizon, and risk capacity first. |

| Counting holdings as proof of diversification | Many holdings can still share the same sector, valuation driver, or economic sensitivity. | Check overlap across business drivers, sectors, and position weights. |

| Ignoring position size | A single large position can dominate the result even if the portfolio contains many smaller holdings. | Map each holding by percentage impact on the full portfolio. |

| Treating rebalancing as market timing | Review discipline can become a prediction exercise instead of a structure check. | Review drift, concentration, thesis change, and risk tolerance against the original plan. |

| Using model portfolios as shortcuts | A model allocation may not match the investor’s goals, risk capacity, time horizon, tax context, or knowledge base. | Use examples only as learning references, not as universal instructions. |

A Repeatable Stock Portfolio Workflow

- Define the portfolio role. Decide whether the stock portfolio is meant to provide long-term ownership exposure, income support, business participation, or another clearly defined objective.

- Set the risk boundary. Identify the level of volatility, drawdown, or liquidity pressure that could be tolerated without forcing a bad decision.

- Map broad exposure. Decide which sectors, regions, business types, and economic drivers should be represented, limited, or avoided.

- Select holdings after the exposure map is clear. Review business quality, valuation, financial strength, and thesis fit without letting one attractive company distort the whole portfolio.

- Assign position weights. Size holdings so that each position’s impact reflects uncertainty, role, downside tolerance, and total portfolio exposure.

- Check overlap and concentration. Look for repeated exposure to the same sector, factor, customer base, financing condition, or economic driver.

- Set a review rhythm. Revisit drift, thesis changes, risk changes, and position weights on a defined schedule or after material company-level changes.

What This Process Does Not Prove

A portfolio-building process does not prove that selected stocks will perform well, that losses will be avoided, or that a particular allocation is suitable for every investor. It only creates a more structured way to connect goals, exposures, weights, diversification, concentration, and review rules.

The process also does not replace security analysis. A well-balanced portfolio can still contain weak businesses, expensive valuations, fragile balance sheets, or earnings assumptions that fail. Portfolio construction and company analysis need to work together rather than replace each other.

FAQ

How many stocks do you need to build a stock portfolio?

There is no universal stock count that proves a portfolio is well built. The more important checks are position weights, overlap, sector exposure, business drivers, and whether one adverse condition could pressure many holdings at the same time.

Is rebalancing a way to predict the market?

No. Rebalancing is better understood as a review process for drift, overweight positions, changed risk, or changed thesis conditions. It does not predict which stocks or sectors will perform best.