A butterfly spread is a same-expiration options spread built around three strike prices and a 1-2-1 body-and-wings structure. The position creates a defined expiration payoff profile, with the strongest theoretical payoff near the middle strike and defined loss outside the wings before costs, liquidity effects, taxes, margin treatment, and assignment or exercise outcomes.

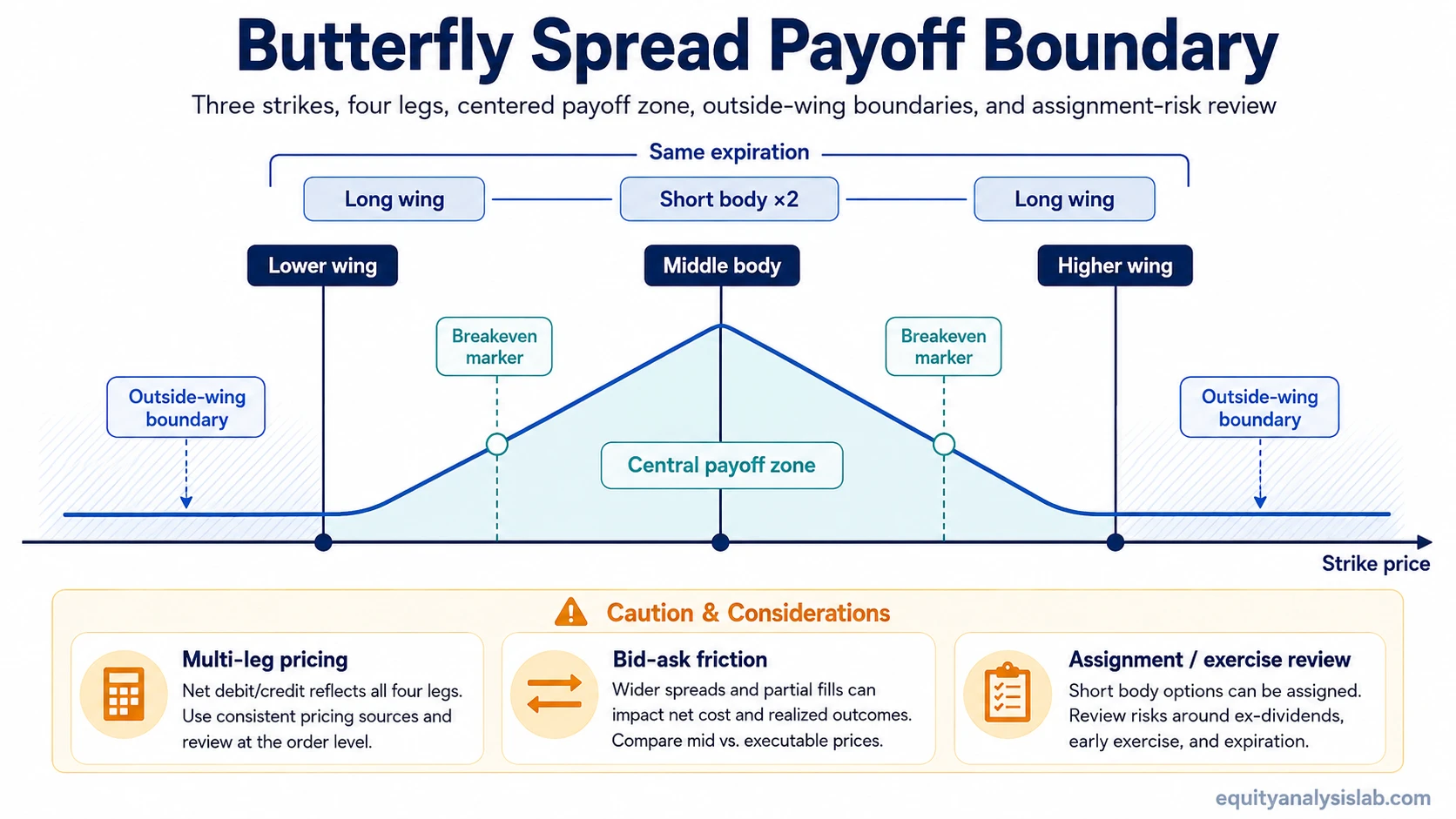

Definition: A butterfly spread combines four options at three strike prices. A standard long butterfly usually uses one lower-strike option, two middle-strike options, and one higher-strike option with the same expiration. The middle strike forms the body of the structure, while the outer strikes form the wings.

The structure is usually discussed as either a call butterfly or a put butterfly. Both versions can create a similar expiration payoff shape, but the contracts used, assignment exposure, liquidity, and pre-expiration behavior still need separate review.

Key Points

- A butterfly spread uses three strike prices and four option legs in a 1-2-1 structure.

- The payoff is most concentrated near the middle strike at expiration, before costs and account-level effects.

- The outer strikes define the expiration loss boundary, but they do not remove liquidity, assignment, exercise, or pre-expiration price risk.

- Net debit or net credit changes the breakeven math and the way the position should be interpreted.

- A clean payoff diagram can still differ from the realized result when bid-ask spreads, commissions, slippage, early exercise, or implied volatility changes matter.

How a Butterfly Spread Is Structured

A basic long call butterfly uses calls at a lower strike, a middle strike, and a higher strike with the same expiration. A basic long put butterfly uses puts at the same three-strike layout. The common structure is described as 1-2-1 because it normally contains one long option on one wing, two short options at the middle strike, and one long option on the other wing.

The middle strike is the center of the payoff profile. The outer strikes define the wings and limit the expiration payoff range. In a balanced butterfly, the distance from the lower strike to the middle strike is usually the same as the distance from the middle strike to the higher strike.

| Part of the structure | Typical role | What it affects |

|---|---|---|

| Lower strike wing | Defines one outside boundary of the spread | Helps frame the lower side of the expiration payoff map |

| Middle strike body | Usually contains two short options in a standard long butterfly | Creates the central payoff zone and the main assignment point to review |

| Higher strike wing | Defines the other outside boundary of the spread | Helps frame the upper side of the expiration payoff map |

| Same expiration | Keeps the payoff map tied to one expiration date | Separates a butterfly spread from time-spread structures such as calendar spreads |

A butterfly is narrower and more centered than a simple vertical spread. For example, a bull call spread uses two call strikes, while a butterfly adds a middle body and a second wing. That extra structure changes the payoff from a broad directional spread into a more concentrated boundary map.

Payoff Boundary Map

The payoff profile depends on the option type, strike spacing, premium paid or received, and whether the spread is evaluated at expiration or before expiration. The cleanest version is a simplified balanced long butterfly opened for a net debit.

| Expiration area | Simplified interpretation | Risk review |

|---|---|---|

| Below the lower wing | The spread is typically outside the central payoff zone | For a long debit butterfly, the theoretical expiration loss is usually limited to the net debit paid, before costs and account-level effects |

| Near the middle strike | The spread is closest to its strongest theoretical expiration payoff | Actual outcome can still be reduced by transaction costs, bid-ask spreads, exercise handling, and assignment effects |

| Above the higher wing | The spread is again outside the central payoff zone | For a long debit butterfly, the theoretical expiration loss is usually limited to the net debit paid, before costs and account-level effects |

This boundary map is not the same as a recommendation. It is a way to understand how the contracts interact at expiration. Before expiration, the position can reprice as time value, implied volatility, skew, liquidity, and the underlying price change.

Maximum Profit, Maximum Loss, and Breakeven

For a simplified balanced long call butterfly opened for a debit, the maximum theoretical expiration payoff usually occurs if the underlying finishes near the middle strike. A common simplified formula is the distance between the lower strike and the middle strike, minus the net debit paid. This formula assumes equal wing width and does not include commissions, slippage, taxes, exercise handling, margin treatment, or assignment outcomes.

The maximum theoretical expiration loss for that simplified long debit butterfly is usually the net debit paid. That loss can occur if the underlying finishes outside the wings at expiration. The real account result can still differ because multi-leg spreads have execution costs and operational risks that a simplified payoff formula does not show.

| Item | Simplified long debit butterfly formula | Important qualifier |

|---|---|---|

| Maximum theoretical expiration payoff | Wing width minus net debit paid | Usually centered near the middle strike in a balanced long butterfly |

| Maximum theoretical expiration loss | Net debit paid | Before commissions, slippage, taxes, margin effects, and assignment or exercise outcomes |

| Lower breakeven | Lower strike plus net debit paid | Applies to a simplified balanced long call butterfly opened for a debit |

| Upper breakeven | Higher strike minus net debit paid | Applies to a simplified balanced long call butterfly opened for a debit |

Other butterfly variations can change the calculation. A credit butterfly, broken-wing butterfly, unbalanced butterfly, iron butterfly, or structure with uneven strike spacing should not be evaluated with the same shortcut without checking the exact contracts and premium.

Call Butterfly vs Put Butterfly

A call butterfly and a put butterfly can be built around the same lower, middle, and higher strikes. At expiration, they can produce a similar centered payoff shape when the strike spacing and premium are comparable. The difference is the contract type used to create that shape.

A call version uses calls across the three strikes. A put version uses puts across the three strikes. The choice can affect liquidity, pricing, assignment exposure, and how the position behaves before expiration. It should not be reduced to a simple bullish or bearish label.

The distinction is different from a bear put spread, which uses two put strikes and normally expresses a more directional vertical-spread payoff. A butterfly uses a centered three-strike structure instead of a two-strike directional boundary.

Volatility and Time-to-Expiration Behavior

A butterfly spread is often discussed through its expiration payoff diagram, but the position does not trade only at expiration value before expiration arrives. The legs still carry time value, implied volatility exposure, and sensitivity to how the market prices different strikes.

A narrow centered payoff can be affected by changes in implied volatility. If implied volatility rises, falls, or shifts unevenly across strikes, the spread can change value even when the underlying price has not moved much. Time decay can also affect the legs differently as expiration approaches.

Limitation: Saying that a butterfly spread has defined expiration risk does not mean the position is simple before expiration. The visible payoff shape is only one layer. Liquidity, volatility, assignment, exercise, tax treatment, and execution friction can all change the practical result.

Assignment and Exercise Review

Many butterfly structures contain short options at the middle strike. Short options can create assignment exposure when the option style and market conditions allow exercise. This is especially important for American-style equity options, which can generally be exercised before expiration.

The long wings help define the expiration payoff map, but they do not erase the need to understand assignment and exercise procedures. A short middle option may be assigned, while a long wing may require a separate exercise or closing decision. Account permissions, settlement rules, margin treatment, and broker procedures can affect what happens after assignment or exercise.

This assignment review is also relevant when comparing a butterfly to other short-option structures such as a bull put spread. The name of the spread does not fully describe the operational risk. The actual contracts, option style, expiration, moneyness, and account treatment matter.

Illustrative Butterfly Spread Example

Assume a simplified balanced long call butterfly uses a lower strike at 95, a middle strike at 100, and a higher strike at 105. The structure buys one 95 call, sells two 100 calls, and buys one 105 call with the same expiration. If the net debit is 1.00, the wing width is 5.00.

In that simplified example, the maximum theoretical expiration payoff before costs would be 4.00, calculated as the 5.00 wing width minus the 1.00 net debit. The lower breakeven would be 96.00, and the upper breakeven would be 104.00. Below the lower wing or above the higher wing, the simplified theoretical expiration loss would usually be the 1.00 debit.

Example boundary: This example is only a payoff illustration. It is not a real trade, recommendation, forecast, or account-level result. Actual outcomes can be reduced or changed by commissions, slippage, bid-ask spreads, taxes, liquidity, margin treatment, early assignment, exercise handling, and closing decisions before expiration.

How a Butterfly Spread Differs From Nearby Structures

A butterfly spread should not be treated as a generic name for every defined-risk options position. The three-strike body-and-wings structure separates it from vertical spreads, condors, calendar spreads, and iron butterflies.

| Structure | Main difference | Why the distinction matters |

|---|---|---|

| Vertical spread | Usually two strikes and two legs | Simpler directional payoff boundary |

| Butterfly spread | Three strikes and four legs in a 1-2-1 layout | Payoff is concentrated around the middle strike |

| Iron butterfly | Uses both calls and puts around a central strike area | Premium setup, contract mix, and assignment exposure can differ from a standard call or put butterfly |

| Condor | Uses a wider middle range rather than one central body strike | Payoff zone is usually spread across a range rather than centered on one strike |

| Calendar spread | Uses different expirations | Time structure becomes central instead of a same-expiration body-and-wings map |

When the Payoff Diagram Can Mislead

The payoff diagram is clearest at expiration. Before expiration, the options still have time value and implied volatility sensitivity. A position can look near the center of the diagram and still reprice unfavorably if the market changes how it values the legs.

Another weak interpretation is assuming defined expiration loss means the position is simple to close or manage. Multi-leg spreads can become harder to exit when markets widen. Short middle options can introduce assignment concerns. Long wings can protect the expiration map while still requiring exercise and settlement awareness.

Risk-review frame: A butterfly spread should be read in layers: contract structure, expiration payoff, pre-expiration volatility behavior, liquidity, transaction costs, and assignment or exercise mechanics. The name of the spread is not enough to describe the full risk profile.

FAQ

What is a butterfly spread?

A butterfly spread is a same-expiration options spread with three strike prices and four option legs arranged in a 1-2-1 structure. It creates a defined expiration payoff profile centered around the middle strike.

Is a butterfly spread bullish or bearish?

A butterfly spread is not purely bullish or bearish by name alone. Its interpretation depends on the strikes, option type, premium, current underlying price, and whether the structure is being evaluated at expiration or before expiration.

What is the maximum profit on a butterfly spread?

In a simplified balanced long butterfly, the maximum theoretical expiration payoff is usually near the middle strike, after accounting for the net premium. Actual results can be reduced by transaction costs, slippage, bid-ask spreads, and account-level factors.

What is the maximum loss on a butterfly spread?

In a simplified long butterfly opened for a debit, the maximum theoretical expiration loss is usually the net debit paid, before commissions, slippage, taxes, and account-level effects. Other butterfly variations can have different risk calculations.

Can a butterfly spread have assignment risk?

Yes. Many butterfly structures include short options at the middle strike. Short options can create assignment exposure, especially with American-style options or near expiration. Assignment and exercise procedures should be reviewed separately from the payoff diagram.

Why do liquidity and bid-ask spreads matter?

A butterfly spread has multiple legs, so execution friction can matter across the full structure. Wide bid-ask spreads, thin markets, commissions, and slippage can reduce or overwhelm the theoretical payoff shown in a simplified diagram.