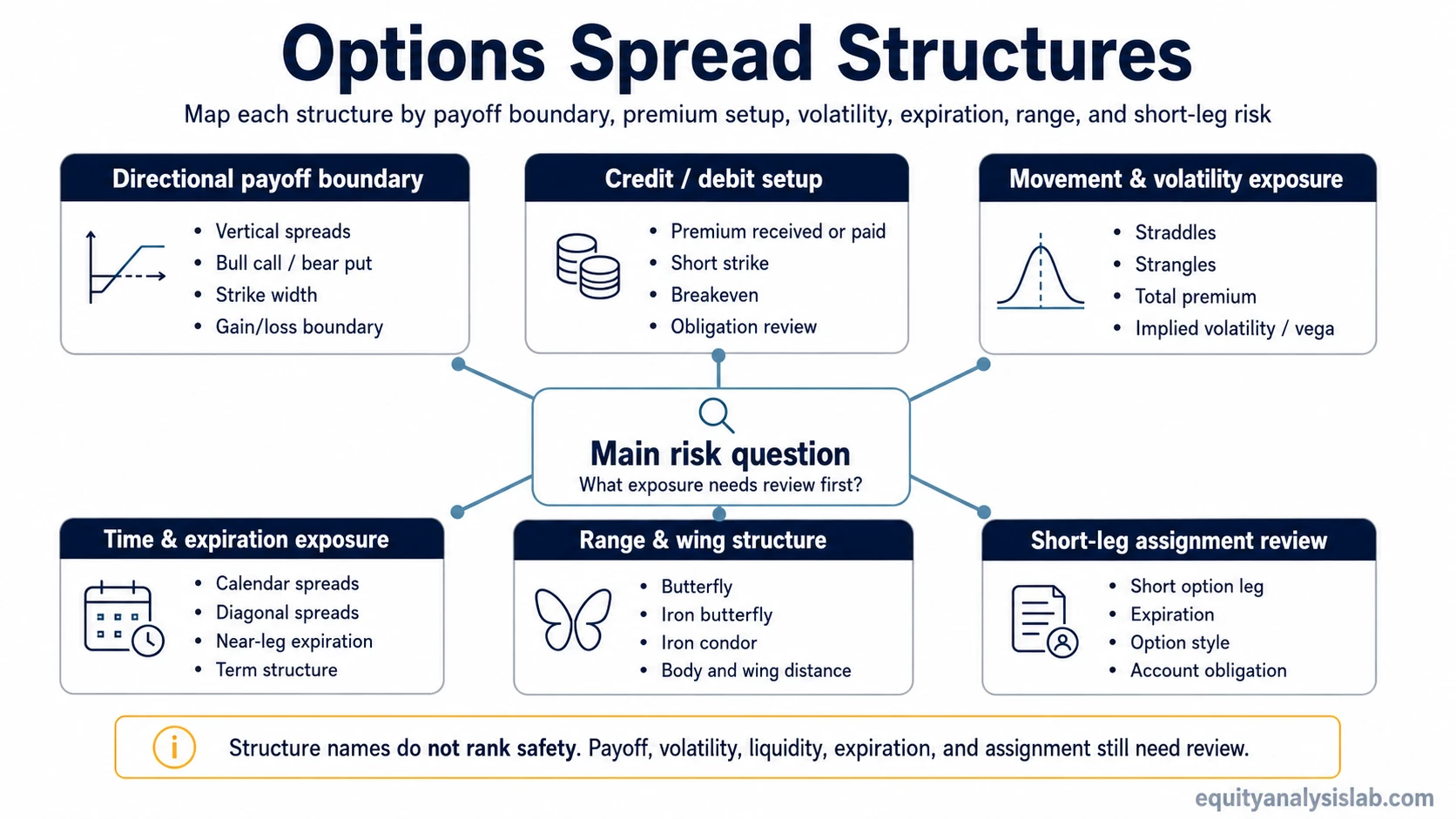

Options spread structures organize multi-leg option positions by strike selection, expiration, credit or debit setup, volatility exposure, payoff boundary, and assignment or exercise risk. The right next concept depends on whether the main question is directional payoff control, volatility or movement exposure, time-structure exposure, range-bound payoff, or the difference between credit and debit setups.

Definition: An options spread structure combines two or more option legs so the position has a specific payoff shape, premium profile, expiration pattern, and risk boundary. The structure can limit or reshape exposure, but short legs, expiration timing, implied volatility, liquidity, and assignment rules still need separate review.

Key Points

- Options spread structures are best separated by the risk variable they change: direction, premium, volatility, time, range, or obligation.

- Vertical spreads usually start with strike width and directional payoff boundaries.

- Credit and debit spreads differ first by whether premium is received or paid, not by whether the position is automatically safer.

- Straddles and strangles focus more on movement size and volatility sensitivity than on direction alone.

- Calendar and diagonal structures add expiration and term-structure risk because the legs do not mature in the same way.

What Options Spread Structures Organize

Options spread structures organize how option legs work together. The main variables are strike placement, expiration date, premium paid or received, short-leg obligation, implied volatility exposure, and the shape of the payoff at expiration.

A spread can narrow the range of possible outcomes compared with a single option, but it also introduces trade-offs. Capped upside, capped downside, premium income, lower entry cost, time decay exposure, and volatility sensitivity can all appear in different combinations.

Practical distinction: payoff shape and volatility exposure are related but not identical. A payoff diagram can show where gains or losses appear at expiration, while implied volatility can still change option value before expiration.

Which Spread Structure Should You Read First?

Use the table as a concept map, not as a strategy selector; each structure still needs its own payoff, margin, expiration, liquidity, and assignment review.

| Risk question | Structure family | Relevant concepts | What to check first | Main limitation |

|---|---|---|---|---|

| Need capped directional payoff | Directional / vertical spreads | vertical spread, bull call spread, bear put spread, bull put spread | Strike width, net debit or credit, maximum gain/loss boundary | Capped payoff does not remove loss risk. |

| Need to understand credit versus debit setup | Credit / debit structures | credit spread, debit spread, credit spread vs debit spread | Premium received or paid, short strike, breakeven | Premium changes net economics but does not erase obligation. |

| Need large movement or volatility exposure | Movement / volatility structures | long straddle, long strangle | Total premium, breakeven distance, implied volatility, vega | Implied volatility can be high and the realized move can still be insufficient. |

| Need range-bound payoff | Winged / range structures | butterfly spread, iron butterfly, iron condor, condor vs butterfly | Body and wing distance, short strikes, expiration | Range structures remain exposed to gaps, liquidity changes, and tail movement. |

| Need time or expiration exposure | Time-structure spreads | calendar spread, diagonal spread, poor man’s covered call | Near-leg expiration, long-leg expiration, term structure, vega | Time-spread value and risk can become more sensitive as the near-dated leg approaches expiration. |

| Need assignment review | Short-leg structures | Credit spreads, bull put spreads, iron condors, and other structures with short option legs | Short option leg, expiration, option style, early assignment conditions | A short option leg can create assignment obligations even inside a defined-risk structure. |

Directional, Credit/Debit, Volatility, Range, and Time Routes

Directional payoff structures: vertical spreads, bull call spreads, bear put spreads, and bull put spreads are usually the cleaner starting point when the main issue is directional exposure with a defined payoff boundary. The first checks are strike width, premium, breakeven, and how much gain or loss is capped.

Credit and debit structures: credit spreads and debit spreads separate positions by premium flow. A credit spread begins with premium received and a short-option obligation. A debit spread begins with premium paid and needs enough favorable price, time, or volatility behavior to justify that cost.

Volatility and movement structures: long straddles and long strangles focus on whether the underlying moves enough relative to the total premium paid. Implied volatility and vega matter because the option’s value can change before the underlying reaches a breakeven level.

Range and wing structures: butterfly spreads, iron butterflies, and iron condors concentrate attention around strike placement, wing width, and the price range where the structure performs best. The main risk is that the underlying leaves the expected range or liquidity worsens before the position can be closed or adjusted.

Time-structure spreads: calendar spreads, diagonal spreads, and poor man’s covered calls add an expiration relationship between legs. The near-dated leg, long-dated leg, implied volatility, and assignment risk on any short option leg must be reviewed together.

Payoff Shape and Volatility Exposure Are Different

Payoff shape describes where the structure can gain or lose value at expiration. Volatility exposure describes how changes in implied volatility can affect option value before expiration. The same structure can therefore look controlled on a payoff diagram while still being sensitive to volatility, liquidity, and timing.

A vertical spread is often read through directional payoff boundaries. A long straddle or long strangle is more sensitive to movement size and implied volatility. A calendar or diagonal spread depends on the relationship between different expirations. A butterfly or condor depends heavily on whether price stays near the intended range.

Core distinction: payoff diagrams simplify the expiration outcome. They do not fully show bid-ask spreads, assignment risk on short option legs, early exercise behavior where applicable, volatility changes, or the path the underlying takes before expiration.

What Spread Structures Do Not Remove

Risk boundary: spread structure changes the shape of the position. It does not automatically make the position safe. Premium received changes net economics but does not erase the contract obligation. Defined payoff diagrams may not show liquidity, assignment risk on short legs, early exercise timing, or how the position behaves before expiration.

- Short legs still matter: any short option leg needs review for assignment or exercise rules, especially when expiration, dividends, or moneyness create practical risk.

- Defined risk is not the same as no risk: a spread can cap certain outcomes while still allowing loss, slippage, and unfavorable adjustment costs.

- Implied volatility is not direction: implied volatility affects option value, but it does not predict the underlying’s direction by itself.

- Time changes behavior: spread value and risk can become more sensitive as expiration approaches, especially when one leg expires before another.

- Liquidity can change realized outcomes: wide bid-ask spreads can make closing, adjusting, or valuing the structure harder than a clean example suggests.

- Tail movement can overwhelm the intended range: range-bound and winged structures still need review for gaps, fast moves, and price paths outside the expected zone.

Scope Boundaries

Spread names do not rank strategies from safest to riskiest. They describe how option legs are arranged. The actual risk depends on strike selection, expiration, premium, implied volatility, short-leg exposure, liquidity, option style, and the account impact of assignment.

Full payoff calculations, live option-chain pricing, ticker-specific premiums, and strategy ranking require a narrower structure-specific review. Broad option spread strategies can be useful after the main spread family is clear, but the first decision is still the risk variable that needs to be understood.

Next Concept Paths

Start with credit spread versus debit spread when premium flow is the main confusion. Start with calendar spread or diagonal spread when expiration timing is the main issue. Start with long straddle or long strangle when the main question is movement size and volatility exposure.

For range-bound structures, compare butterfly spread, iron butterfly, and iron condor before moving into a detailed payoff example.