Option spread strategies are multi-leg options structures that combine two or more contracts on the same underlying to shape premium, debit or credit exposure, expiration behavior, payoff boundaries, and short-leg risk.

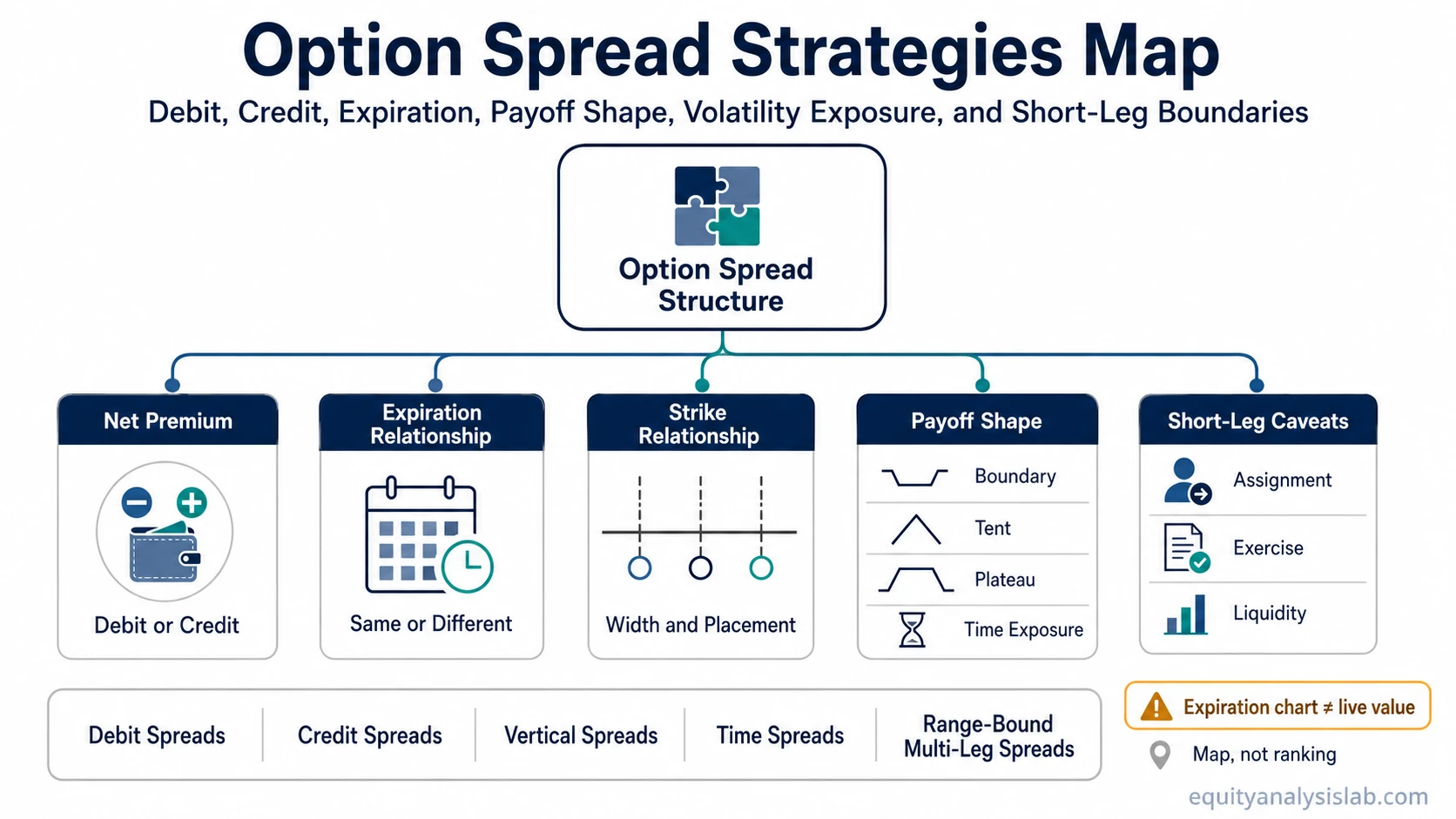

The main task is not ranking spread names. The useful first step is separating how the contracts are built: whether the structure starts from a net debit or net credit, whether the legs share the same expiration, how the strikes are placed, how the payoff changes near expiration, and whether any short option leg creates assignment or exercise considerations.

Definition: An option spread strategy combines multiple option legs so the position has a defined relationship between strikes, expirations, premiums, and payoff behavior. The structure can limit some exposures while introducing others, so the name of the spread is only the starting point.

Key Points

- Option spread strategies use more than one option contract rather than a single standalone option.

- The first mechanical split is usually net debit versus net credit, then strike relationship, expiration relationship, payoff shape, and volatility exposure.

- Short option legs can introduce assignment or exercise considerations before settlement.

- Expiration payoff diagrams simplify the structure and do not fully describe value while the options are still open.

- A broad spread map is most useful when it leads into structure-specific explanations instead of ranking spreads as better or worse.

What Option Spread Strategies Are

An option spread starts by pairing contracts so one leg changes the exposure created by another leg. A long option may be offset by selling another option at a different strike, a short option may be paired with a farther protective leg, or contracts may use different expirations to create time-spread exposure.

Most spreads can be compared through four mechanical questions: what premium is paid or received, whether the contracts share expiration, where the strikes sit relative to each other, and how the payoff behaves if the underlying finishes in different zones at expiration.

That structure does not remove the need to understand volatility, liquidity, bid-ask spreads, exercise style, assignment risk, and account-specific margin treatment. A defined payoff boundary can still behave differently prior to settlement because option value changes with time, implied volatility, rates, dividends where relevant, and movement in the underlying.

The Main Families of Option Spreads

Spread families are easier to compare when they are grouped by construction logic instead of by preference. A debit structure begins with premium paid. A credit structure begins with premium received. A vertical structure uses the same expiration with different strikes. A calendar structure uses different expirations, often around the same or nearby strike. A diagonal structure changes both strike and expiration.

| Spread family | Construction logic | Main comparison point | Boundary to check |

|---|---|---|---|

| Debit spreads | Net premium is paid to establish the structure. | Payoff depends on whether the movement is enough to overcome the debit and strike relationship. | Maximum loss is often linked to the debit, but live option value can still vary. |

| Credit spreads | Net premium is received because a short option is paired with another option leg. | The structure depends heavily on short-leg behavior, strike width, and assignment or exercise conditions. | Defined risk does not mean negligible risk. |

| Vertical spreads | Same expiration, different strikes. | Strike width and direction of exposure shape the payoff boundary. | Expiration payoff can look simple while live valuation remains dynamic. |

| Calendar spreads | Different expirations, often with similar strike placement. | Time decay, term structure, and implied volatility matter more than strike width alone. | The spread is not explained by a single expiration payoff line. |

| Diagonal spreads | Different strikes and different expirations. | Both directional exposure and time-spread exposure interact. | Small changes in volatility or time value can change the interpretation. |

| Range-bound multi-leg spreads | Several legs define a central zone, wing, plateau, or tent-like payoff shape. | Payoff shape, short strikes, and wing width matter more than the label alone. | Short-leg exposure and liquidity can become important while the position is open. |

Debit, Credit, Expiration, and Payoff Shape

A debit spread structure starts from premium paid, so the initial cost is part of the risk boundary. That does not make the structure automatically safer or better; it only identifies the starting cash-flow direction and the way the payoff must be interpreted.

A credit spread starts from premium received and usually contains at least one short option leg. The short leg makes assignment, exercise, and margin treatment part of the analysis, especially when the underlying moves near or through the short strike before expiration.

Expiration relationships create a second layer. Same-expiration spreads often look cleaner on a payoff diagram because all legs settle on the same date. Different-expiration structures can be more sensitive to time value and volatility because one leg continues to exist after another leg expires or changes value at a different rate.

Payoff map note: An expiration payoff chart is a boundary model. It can help compare zones, breakevens, and maximum theoretical outcomes at expiration, but it does not fully describe the spread’s value while the options are still open.

How to Compare Spread Structures Without Ranking Them

A useful comparison begins with structure, not opinion. Two spreads can both be risk-defined and still behave differently because one has a debit profile, one has a credit profile, one is more sensitive to implied volatility, or one contains short strikes closer to the current underlying price.

Comparison sequence: Start with net premium, then check strike width, expiration relationship, payoff shape, volatility exposure, short-leg conditions, liquidity, and transaction costs. The spread name is less informative than the combination of these variables.

Premium alone is especially incomplete. A smaller net debit or larger credit can look attractive in isolation, but the structure may have narrower payoff room, stronger volatility sensitivity, less favorable liquidity, or assignment conditions that require closer reading.

Where Different Spread Structures Fit in the Map

Different spread structures answer different mechanical questions. The categories below separate them by construction logic and caveat, while leaving detailed payoff mechanics to the structure-specific explanations.

| Structure | Typical construction logic | Main boundary to understand | Main caveat | Further structure to study |

|---|---|---|---|---|

| Directional debit vertical | Long option paired with another option at a different strike and same expiration. | Net debit, strike width, and expiration zone. | The debit does not explain live option value by itself. | bull call spread structure |

| Bearish debit vertical | Put-based vertical structure with same-expiration legs at different strikes. | Debit paid, lower strike boundary, and expiration payoff zone. | The structure still depends on timing, volatility, and liquidity. | bear put spread |

| Short-premium vertical | Short option paired with a farther option leg to define the boundary. | Credit received, strike width, and short-leg zone. | Assignment and exercise conditions can matter before expiration. | put-credit spread structures |

| Time-spread structure | Options use different expirations, often around a similar strike area. | Time value, implied volatility, and expiration sequencing. | A single expiration payoff line can be misleading. | calendar spread |

| Tent-shaped multi-leg spread | Long and short legs form a central payoff area with wings. | Center strike, wing width, and payoff tent. | Maximum labels are expiration-model outputs, not full real-time valuation. | butterfly-style spreads |

| Range-bound credit structure | Call-side and put-side spreads combine into a wider defined-risk structure. | Short strikes, wing width, net credit, and plateau zone. | Short-leg, liquidity, and gap risk still require attention. | iron condor structures |

Common Mistake: Treating Premium or Payoff Charts as the Whole Risk

Common mistake: Comparing spreads only by premium received, premium paid, or maximum payoff can hide the real interpretation layers: volatility exposure, assignment, exercise, liquidity, bid-ask spread, transaction cost, time decay, and live option value.

A payoff chart can make a spread look precise because it usually displays fixed expiration zones. Real option value before expiration is more fluid. Implied volatility can change, time decay can affect each leg differently, and short options can create practical conditions that do not appear in a simplified payoff diagram.

Liquidity also matters. A spread with several legs may have wider bid-ask friction than a single option, and the cost of entering or exiting each leg can affect the practical interpretation of the structure. These frictions are not a reason to dismiss spreads by default; they are part of the comparison.

Simple Option Spread Strategy Example

An investor comparing spread families may begin with two broad candidates: one structure starts with a debit and another starts with a credit. The debit structure may have a clearer initial cost boundary, while the credit structure may introduce a short strike that requires assignment and exercise awareness.

The next comparison is mechanical rather than selective: whether the legs share expiration, how far apart the strikes are, what the payoff shape looks like at expiration, how live value can change, and whether the structure depends heavily on implied volatility or short-leg behavior.

That sequence keeps the comparison anchored in structure. Once the mechanical family is clear, the next distinction is the specific spread type, because each structure has its own payoff boundary, volatility sensitivity, and short-leg caveats.

Limitations Before Comparing Any Spread

Expiration-only payoff: Many payoff diagrams describe expiration outcomes. They do not fully explain mark-to-market value before expiration.

Assignment and exercise: Any structure with short option legs can require attention to assignment, exercise style, dividends where relevant, and broker-specific processing.

Volatility exposure: The spread name alone does not reveal how implied volatility changes may affect the position before expiration.

Liquidity and costs: Multi-leg structures can be affected by bid-ask spreads, leg execution, transaction costs, and contract availability.

Account rules: Margin, approval level, tax treatment, and exercise handling can vary by broker, account type, jurisdiction, and product.

FAQ

What is the difference between a debit spread and a credit spread?

A debit spread begins with net premium paid, while a credit spread begins with net premium received. The distinction affects the starting cash-flow profile, but it does not determine whether the structure is suitable or low risk.

Why can an expiration payoff chart be incomplete?

An expiration payoff chart models outcomes at expiration. Before expiration, option value can change because of time decay, implied volatility, movement in the underlying, liquidity, and short-leg conditions.

Do defined-risk spreads remove assignment or exercise risk?

No. Defined-risk structures can still contain short option legs, and short legs may create assignment or exercise considerations before expiration depending on contract terms and market conditions.