In its standard form, an iron condor is a same-expiration four-leg options spread that combines an out-of-the-money put spread with an out-of-the-money call spread. It is commonly structured for a net credit, with defined expiration payoff boundaries before commissions, fees, liquidity friction, and assignment or exercise complications.

The structure has two inner short strikes and two outer long strikes. The inner short strikes define the central expiration range, while the outer long strikes define the outside wings that cap the spread’s expiration loss before costs and contract-specific complications.

What Is an Iron Condor?

An iron condor is an options spread built from four contracts on the same underlying asset and, in the standard version, the same expiration date. The lower side is a put spread, and the upper side is a call spread. The two short options sit closer to the current underlying price, while the two long options sit farther away as protective wings.

- It uses four legs: lower long put, short put, short call, and higher long call.

- It is usually opened for a net credit, before commissions and fees.

- Its expiration breakevens depend on the short strikes and the net credit.

- Its maximum expiration loss depends on the wider spread width minus the net credit, before costs and assignment or exercise complications.

How an Iron Condor Is Built

The lower put side and upper call side create a defined expiration range. The short put and short call form the inner body of the structure. The long put and long call form the outside wings.

| Leg | Relative strike position | Role in structure | What it affects |

|---|---|---|---|

| Lower long put | Lowest strike | Lower protective wing | Caps the lower-side expiration loss before costs and contract complications. |

| Short put | Above the lower long put | Lower inner short strike | Defines the lower edge of the central expiration range and helps determine the lower breakeven. |

| Short call | Below the higher long call | Upper inner short strike | Defines the upper edge of the central expiration range and helps determine the upper breakeven. |

| Higher long call | Highest strike | Upper protective wing | Caps the upper-side expiration loss before costs and contract complications. |

The put side can be understood as the lower boundary of the spread. A separate bear put spread uses put strikes in a directional structure, while the put side inside an iron condor is only one half of a four-leg range structure.

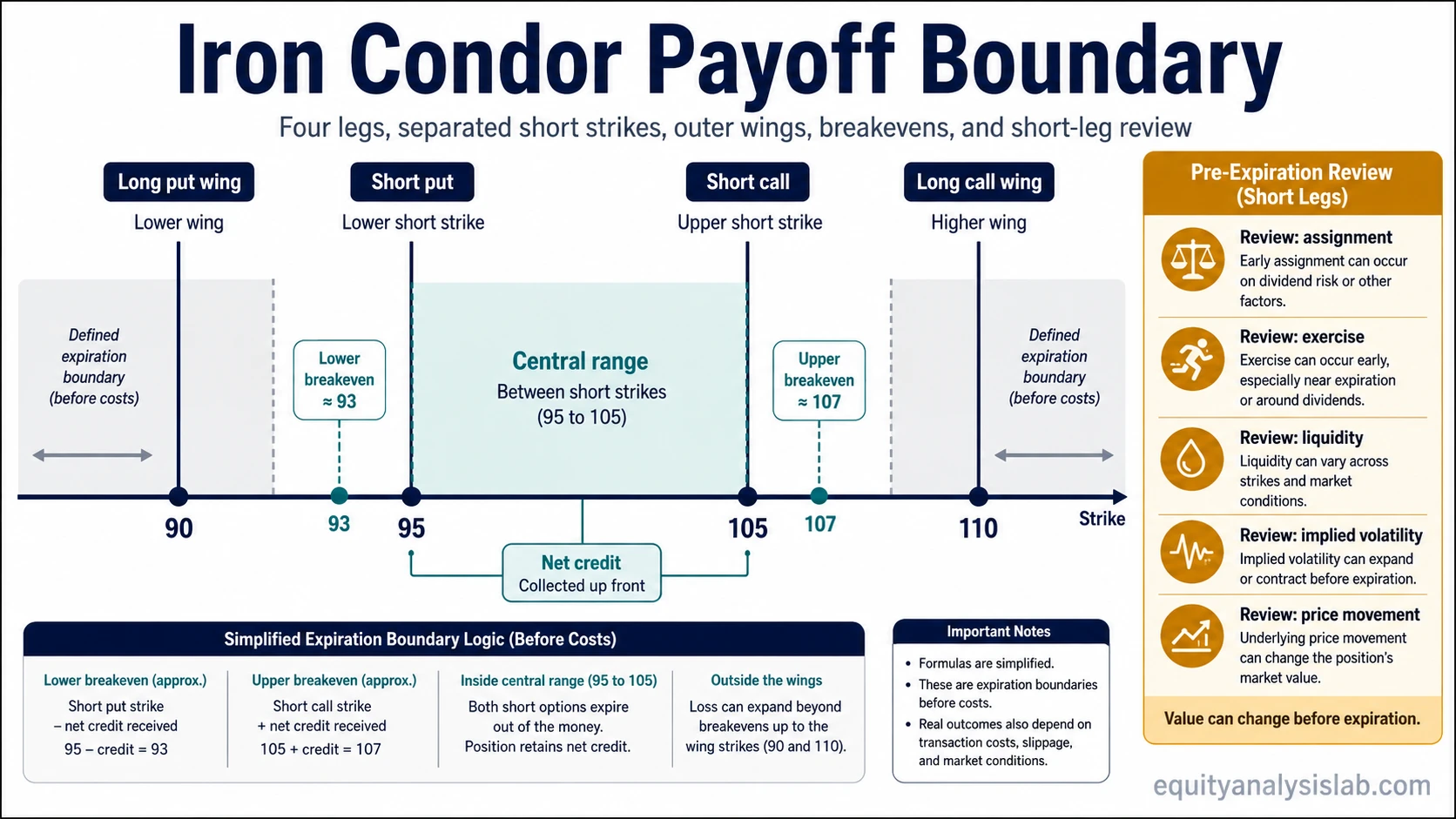

Iron Condor Payoff Boundaries

At expiration, the simplest iron condor payoff depends on the relationship between the underlying price, the four strike prices, and the net credit. These formulas describe expiration boundaries, not the exact market value of the position before expiration.

| Zone / formula | What it means | Important caveat |

|---|---|---|

| Net credit | Premium received from the short options minus premium paid for the long wings. | Commissions, fees, and bid-ask spreads can reduce the effective credit. |

| Lower breakeven = short put strike – net credit | The lower expiration price where the structure is approximately breakeven before costs. | The formula assumes a standard same-expiration structure and ignores transaction costs. |

| Upper breakeven = short call strike + net credit | The upper expiration price where the structure is approximately breakeven before costs. | The formula does not describe interim mark-to-market movement. |

| Maximum credit retained | The net credit before costs if all options expire out of the money. | “Maximum” refers to the simplified expiration result, not a guaranteed outcome before expiration. |

| Maximum loss = widest spread width – net credit | The simplified defined expiration loss boundary before commissions, fees, and contract complications. | If the put side and call side have different widths, the wider side controls the simplified maximum loss formula. |

| Below lower long put | The lower wing has reached its defined expiration boundary. | Assignment, exercise handling, and liquidity can still affect the real-world process. |

| Between short strikes | The underlying expires inside the central range. | The central range does not remove risk before expiration. |

| Above higher long call | The upper wing has reached its defined expiration boundary. | Short call assignment or exercise review can matter before final expiration processing. |

Compact Strike Example

For example, assume a same-expiration iron condor uses a 90 long put, 95 short put, 105 short call, and 110 long call. If the net credit is 2.00, the simplified lower breakeven is 93, and the simplified upper breakeven is 107.

In that scenario, the central expiration range sits between the 95 short put and the 105 short call. The outer wings sit at 90 and 110. The simplified maximum expiration loss is the 5-point spread width minus the 2.00 net credit, or 3.00 before commissions, fees, assignment or exercise complications, and changing market values before expiration.

What the Payoff Table Does Not Show Before Expiration

Defined expiration boundaries do not mean the position has a stable value before expiration. The market value of an iron condor can change as the underlying price moves, implied volatility changes, time passes, and liquidity conditions shift.

- Underlying price movement: movement toward either short strike can increase pressure on that side of the structure.

- Implied volatility: volatility expansion can increase option values and change the spread’s mark-to-market value before expiration.

- Time decay: time decay can affect the short and long legs differently depending on strike distance and remaining time.

- Gamma near expiration: price sensitivity can become sharper as expiration approaches, especially near the short strikes.

- Assignment and exercise review: short options can require special attention when they move in the money or approach expiration.

- Liquidity and cost friction: bid-ask spreads, commissions, and multi-leg execution can make the realized result different from the clean formula.

Why Defined Risk Still Needs Review

An iron condor is often described as a defined-risk spread because the long wings cap the simplified expiration loss. That description is useful, but incomplete. It does not remove the need to understand how the legs interact before expiration.

The most common misunderstanding is treating the expiration payoff table as if it were the live value of the spread. Before expiration, the same four strikes can carry a different market value because implied volatility, time remaining, distance from the short strikes, and liquidity all affect the contracts.

Iron Condor vs Iron Butterfly Boundary

An iron butterfly also uses four legs, but its inner short strikes are concentrated at the same central strike or very close together. An iron condor separates the inner short strikes, creating a wider central expiration range and two distinct short-strike boundaries.

The useful distinction is the shape of the central body. The iron butterfly has a tighter centered body, while the iron condor has a separated inner range between the short put and short call.

Common Misunderstandings

- “Defined risk” does not mean no risk. The expiration loss boundary can be defined while the position still moves sharply before expiration.

- The net credit is not the same as guaranteed income. It is the initial premium relationship before costs and later changes in market value.

- The central range is not a prediction. It is a payoff zone created by the chosen strikes and net credit.

- Assignment risk is not erased by the long wings. The wings affect the spread’s boundary, but short-option review can still matter.

Related Options Spread Concepts

Nearby spread structures can clarify the boundary logic. Bear put spread shows a simpler two-leg put-side structure, while iron butterfly shows how a four-leg structure changes when the inner body is concentrated instead of separated.

The iron condor sits between simpler vertical-spread logic and tighter four-leg iron-butterfly logic: it uses the same-expiration boundary idea, but spreads the inner short strikes apart instead of concentrating the body around one central strike.

FAQ

Is an iron condor the same as an iron butterfly?

No. An iron condor separates the inner short put and short call strikes, while an iron butterfly concentrates the inner body around a tighter central strike area. Both are four-leg structures, but their expiration payoff shapes are different.

Does defined risk mean an iron condor cannot lose more than the formula?

The simplified maximum loss formula describes the expiration boundary before commissions, fees, liquidity friction, and assignment or exercise complications. It does not remove the need to review contract behavior before expiration.

Why can an iron condor change value before expiration?

The spread can change value because the underlying price, implied volatility, time remaining, gamma near expiration, bid-ask spreads, and assignment or exercise considerations can all affect the contracts before expiration.

What are the breakevens on an iron condor?

The simplified lower breakeven is the short put strike minus the net credit. The simplified upper breakeven is the short call strike plus the net credit. Both are expiration formulas before costs and other practical complications.