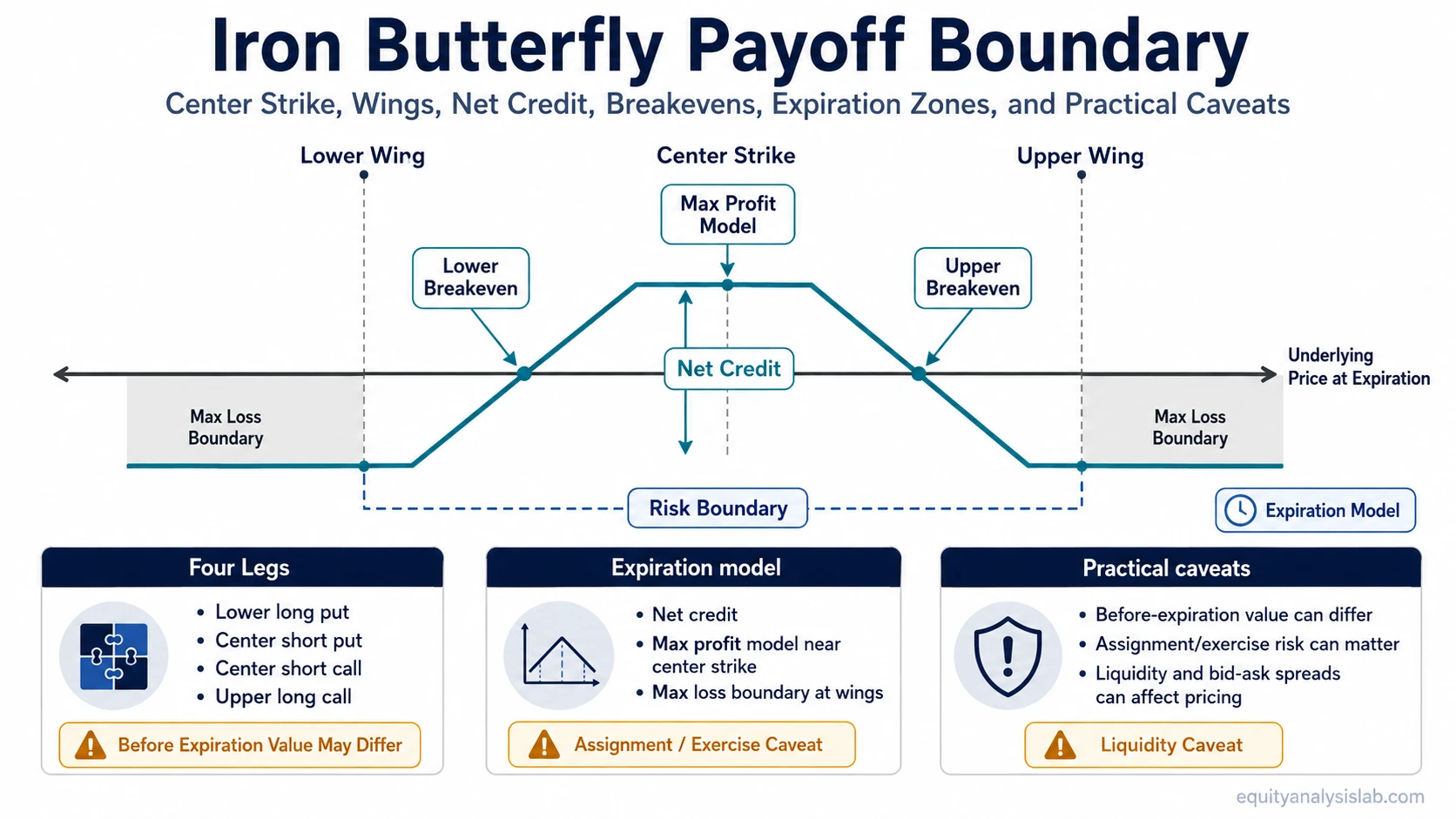

An iron butterfly is a four-leg options spread built around a center short call and short put, with protective long options placed above and below that center strike. The standard short iron butterfly uses the same expiration for all four legs and is opened for a net credit, creating a capped expiration payoff with defined risk boundaries.

The structure is easiest to read by separating observable contract terms from the expiration payoff model. The observable terms are the lower wing, center strike, upper wing, expiration date, and net credit. The risk boundary then depends on the distance between the strikes, the credit received, and where the underlying price settles at expiration.

Key Points

- An iron butterfly combines a short call, short put, lower protective long put, and upper protective long call around the same expiration.

- The center strike is where the short call and short put are placed; the outer long options form the wings.

- Maximum profit is modeled as the net credit if the underlying settles at or near the center strike at expiration.

- Maximum loss is modeled as the wing width minus the net credit when the wings are equal distance from the center strike.

- Before expiration, implied volatility, time remaining, bid-ask spreads, commissions, and assignment risk can make the position value differ from the expiration payoff chart.

What an Iron Butterfly Is

An iron butterfly is a defined-risk, four-leg options spread that combines a short straddle at the center strike with a long option above and a long option below that center. In its standard short form, the structure is usually a net-credit spread because the premium collected from the center short options is greater than the premium paid for the protective wings.

The center strike is the main reference point. The short call and short put sit at that strike, while the long put below and long call above cap the downside and upside loss at expiration. The result is a narrow center area where the payoff model is highest and two outer areas where losses are limited by the long options.

The standard short iron butterfly differs from a reverse or long iron butterfly because the debit-credit relationship and payoff direction change. That means the formulas, risk boundaries, and interpretation are not identical across variants.

How the Four Option Legs Create the Payoff Boundary

An iron butterfly has four option legs on the same underlying asset and the same expiration date. The two center short options create the premium collection and the two outer long options define the risk boundary.

| Leg | Typical position | Role in the structure |

|---|---|---|

| Lower strike put | Long put | Protects the lower side and caps downside loss at expiration. |

| Center strike put | Short put | Collects premium and creates downside exposure between the center strike and lower wing. |

| Center strike call | Short call | Collects premium and creates upside exposure between the center strike and upper wing. |

| Upper strike call | Long call | Protects the upper side and caps upside loss at expiration. |

The center short put and short call are often described as a short straddle. The two long wings convert that uncapped short-straddle exposure into a defined-risk structure. That defined-risk boundary is an expiration-based model; the spread can still change in value before expiration as volatility, time value, and pricing friction change.

Max Profit, Max Loss, and Breakeven Points

For a standard short iron butterfly with equal wing widths, the main formulas use the center strike, wing width, and net credit. They assume the same expiration across all legs and do not include commissions, fees, bid-ask spread, or early assignment effects.

| Payoff item | Simplified formula | Interpretation |

|---|---|---|

| Maximum profit | Net credit received | Occurs in the expiration model if the underlying settles at or very near the center strike. |

| Maximum loss | Wing width minus net credit | Applies to equal-width wings when the underlying settles beyond either outer long option at expiration. |

| Lower breakeven | Center strike minus net credit | The lower expiration price where the payoff model moves from gain to loss before transaction costs. |

| Upper breakeven | Center strike plus net credit | The upper expiration price where the payoff model moves from gain to loss before transaction costs. |

Illustrative formula example: if the center strike is 100, the lower wing is 95, the upper wing is 105, and the net credit is 2, the equal-width wing is 5. The simplified maximum profit is 2, the simplified maximum loss is 3, the lower breakeven is 98, and the upper breakeven is 102. This example is only a contract-structure illustration, not a market example or position recommendation.

If the wings are not equal distance from the center strike, the maximum risk can differ by side. In that case, each side should be evaluated separately rather than using a single wing-width shortcut.

What the Expiration Payoff Chart Does Not Show

An iron butterfly payoff chart is useful because it shows the expiration boundary in a compact shape. It is incomplete because it does not fully show how the spread may be priced before expiration.

| Payoff chart shows | Payoff chart does not fully show |

|---|---|

| The center strike where the expiration payoff is highest. | How implied volatility changes can alter the spread value before expiration. |

| The upper and lower breakeven points under simplified assumptions. | How much extrinsic value remains before expiration. |

| The capped loss outside the wings at expiration. | The effect of wide bid-ask spreads, commissions, or low liquidity across four option legs. |

| The net-credit payoff shape at expiration. | Early assignment or exercise risk on short options, especially around expiration or in-the-money conditions. |

| The basic relationship between strike width, credit, max profit, and max loss. | The actual price at which the full four-leg structure could be opened or closed in a live market. |

Important limitation: the expiration payoff chart is a boundary map, not a complete valuation model. Before expiration, the spread can be affected by volatility, time decay, dividend expectations where relevant, exercise style, liquidity, and the market price of each option leg.

Iron Butterfly vs Nearby Spread Structures

An iron butterfly is related to several spread structures, but its center-strike design gives it a narrower payoff profile than many nearby spreads. The key distinction is that the short call and short put share the same center strike.

| Structure | Main difference | Why the distinction matters |

|---|---|---|

| Iron butterfly | Short call and short put sit at the same center strike, with long wings outside. | The payoff model is concentrated around a narrow center area. |

| butterfly spread structure | Broader family of butterfly-style spreads, which can be built with calls, puts, or combinations depending on the variant. | The iron butterfly is one specific four-leg, credit-oriented version of the broader butterfly idea. |

| wider credit spread structure | The short call and short put are placed at different strikes rather than the same center strike. | The expiration profit zone is wider, but the structure is not the same as a center-strike iron butterfly. |

| bear put spread | A directional put debit spread using two put legs rather than a four-leg center-strike structure. | It isolates downside directional exposure instead of combining a short call and short put at a center strike. |

The distinction matters because the same words “defined risk” and “spread” can describe very different payoff shapes. The iron butterfly is centered around one strike, while nearby structures may distribute exposure across a wider range or express a more directional payoff.

Risks and Limits Before Expiration

The formula view can make an iron butterfly look cleaner than it may feel in real pricing. Four option legs mean four bid-ask spreads, four legs that may move differently, and more sensitivity to execution friction than a single-option position.

A before-expiration quote can therefore move even when the underlying remains near the center strike. A change in implied volatility, a shift in remaining extrinsic value, or a wide market across one leg can change the displayed spread value before the expiration payoff boundary is reached.

| Risk or limitation | Why it matters |

|---|---|

| Assignment and exercise | Short options can create assignment risk, especially if they are in the money or near expiration. Exercise style and contract terms matter. |

| Implied volatility | Changes in implied volatility can change the spread value before expiration even when the underlying price has not moved much. |

| Time decay | Time decay affects the value of the short center options and the long wings, but the net effect depends on price location and volatility. |

| Liquidity and bid-ask spreads | A four-leg spread can be sensitive to poor fills, wide markets, and transaction costs. |

| Unequal wings | If the distance from the center strike to each wing differs, upside and downside risk boundaries may not be symmetrical. |

These limits do not make the structure good or bad by themselves. They define what the payoff formulas leave out and why the contract structure should be separated from any real-world position outcome.

FAQ

What is an iron butterfly in options?

An iron butterfly is a four-leg options spread with a short call and short put at the same center strike, plus a protective long put below and a protective long call above. The standard short version is usually opened for a net credit and has capped profit and capped loss at expiration.

How is max profit calculated on an iron butterfly?

In the simplified standard short iron butterfly model, maximum profit equals the net credit received. This assumes the underlying settles at or very near the center strike at expiration and ignores transaction costs and before-expiration pricing changes.

How is max loss calculated on an iron butterfly?

For an equal-width short iron butterfly, simplified maximum loss is the wing width minus the net credit received. If the wings are unequal, each side should be evaluated separately.

What are the breakeven points for an iron butterfly?

In the simplified equal-width model, the lower breakeven is the center strike minus the net credit, and the upper breakeven is the center strike plus the net credit. These formulas are expiration-based and do not include commissions, bid-ask spreads, or early assignment effects.

Is an iron butterfly the same as an iron condor?

No. An iron butterfly has the short call and short put at the same center strike. An iron condor places the short call and short put at different strikes, creating a wider middle range in the simplified expiration payoff.