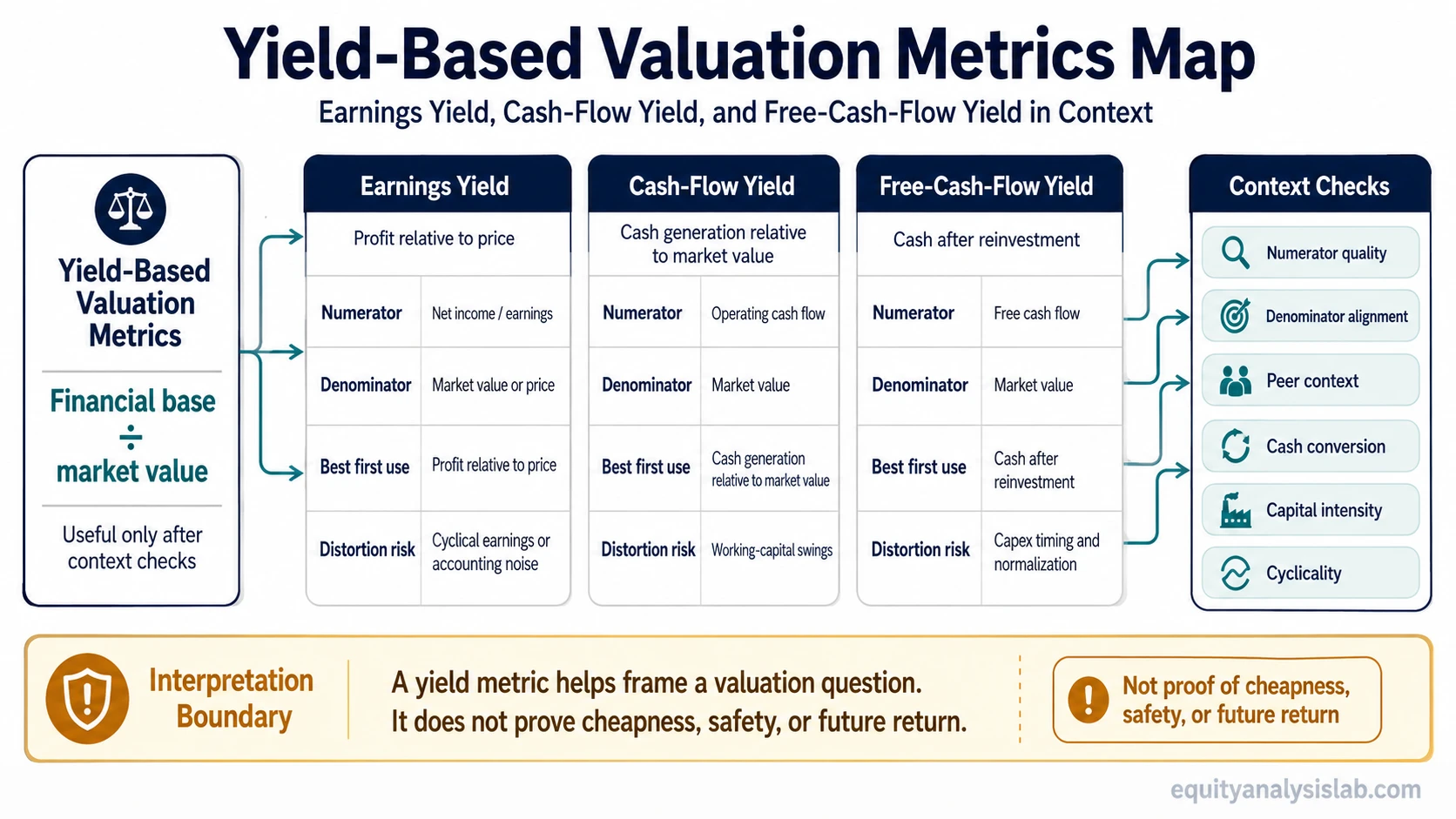

Yield-based valuation metrics compare a company’s earnings or cash-flow base with market value. The useful starting point is not the highest yield by itself, but which yield measure matches the valuation question: earnings yield, cash-flow yield, or free-cash-flow yield.

A higher yield can look attractive, but it does not prove undervaluation, business quality, safety, or future return. The reading depends on what the numerator represents, which market-value denominator is used, whether peers are comparable, and whether earnings or cash flow are durable enough to support the interpretation.

Key Points

- Yield-based valuation metrics express earnings or cash flow as a percentage of market value instead of using a traditional valuation multiple.

- Earnings yield starts with profit, cash-flow yield starts with cash generation, and free-cash-flow yield focuses on cash left after reinvestment or capital spending.

- Numerator quality matters because earnings, operating cash flow, and free cash flow can tell different valuation stories.

- Denominator choice matters because market capitalization, equity value, and enterprise value can answer different capital-claim questions.

- A yield metric is a screening and interpretation tool, not proof that a stock is cheap, attractive, or low risk.

How Yield-Based Valuation Metrics Fit Together

Yield-based valuation metrics are valuation ratios stated as a yield. Instead of asking how many dollars investors pay for one dollar of earnings or cash flow, the yield view asks how much earnings or cash flow is represented by each dollar of market value.

That reversed lens can make valuation comparisons easier to read, especially when comparing earnings-based and cash-flow-based measures. The tradeoff is that a yield percentage can look simpler than the underlying business economics really are. A yield metric still needs context from accounting quality, reinvestment needs, capital intensity, cyclicality, growth expectations, and peer comparability.

Definition: Yield-based valuation metrics express a company’s earnings or cash flow relative to market value, usually as a percentage. They are related to valuation multiples, but they reverse the lens from “price paid for a financial base” to “financial base produced per unit of market value.”

Earnings Yield, Cash-Flow Yield, and Free-Cash-Flow Yield

The main distinction is the numerator. Earnings yield uses profit, cash-flow yield uses cash generation, and free-cash-flow yield focuses on cash remaining after required reinvestment or capital spending. The denominator then determines whether the comparison is framed mainly around equity value, enterprise value, or market capitalization.

| Metric | Main numerator | Common denominator | Best first use | Main distortion risk | Next page |

|---|---|---|---|---|---|

| Earnings yield | Earnings per share, net income, or earnings base | Share price or market value of equity | Comparing earnings relative to price or market value | Accounting earnings can be cyclical, distorted, negative, or temporarily inflated | earnings yield |

| Cash-flow yield | Operating cash flow or another cash-flow base | Market capitalization, equity value, or enterprise value depending on the calculation | Checking whether accounting profit is supported by cash generation | Working-capital movements, one-off cash effects, and denominator mismatch can distort the reading | cash-flow yield |

| Free-cash-flow yield | Free cash flow after capital spending or required reinvestment | Market capitalization, equity value, or enterprise value depending on the valuation frame | Assessing cash left after reinvestment needs | Capital expenditure timing, maintenance versus growth investment, and cyclicality can change the signal | free cash flow yield |

How to Choose the Right Yield Metric

Use earnings yield when the main question is how much accounting profit exists relative to price or market value. It is most useful when earnings are positive, reasonably normalized, and comparable across companies in the same industry or business model group.

Use cash-flow yield when the main question is whether reported earnings are supported by cash generation. This can be useful when accrual accounting, working-capital swings, or non-cash expenses make earnings alone less informative.

Use free-cash-flow yield when the main question is how much cash remains after the business funds necessary reinvestment. This is often more demanding than an earnings-based view, because it forces the valuation reading to account for capital spending and cash conversion.

Practical check: The metric should match the business question. Earnings yield is not a substitute for cash-flow yield when cash conversion is weak. Cash-flow yield is not a substitute for free-cash-flow yield when capital spending is structurally high. Free-cash-flow yield is not always cleaner if free cash flow is temporarily inflated by underinvestment or unusual working-capital movements.

Where Yield-Based Valuation Metrics Can Mislead

Limitation: A high yield can reflect low market expectations, weak growth, cyclicality, distress, accounting distortion, or market skepticism. A low yield can reflect durable growth, lower perceived risk, high expectations, or overvaluation. The yield alone does not decide which interpretation is correct.

Negative earnings can make earnings yield unusable or hard to compare. Distorted cash flow can make cash-flow yield look stronger or weaker than the underlying business really is. Free cash flow can also be misleading when capital expenditure is unusually low, temporarily delayed, or not representative of the company’s long-term reinvestment needs.

Peer context matters because different industries convert revenue into earnings and cash flow in different ways. A software company, a bank, an industrial manufacturer, and a commodity producer can all show very different yield profiles for reasons that have little to do with simple cheapness or expensiveness.

Denominator and Numerator Alignment

Earnings, operating cash flow, and free cash flow are not interchangeable. Earnings can include accruals and non-cash items. Operating cash flow can be affected by working-capital timing. Free cash flow depends on how capital spending and reinvestment are treated.

The denominator must also match the claim being made. Market capitalization usually frames the comparison around common equity. Enterprise value can be more useful when debt, cash, and the full operating business need to be considered. Mixing an equity-level numerator with an enterprise-level denominator, or the reverse, can create a cleaner-looking number that answers the wrong question.

Example: A company can show a strong earnings yield while free cash flow is weak because the business needs heavy reinvestment. Another company can show a lower earnings yield but stronger cash conversion because reported profit turns into cash more consistently. The better comparison depends on the business model, reinvestment needs, balance-sheet structure, and peer group.

What to Read Next

Start with earnings yield when the main question is profit relative to price or equity market value.

Use cash-flow yield when the main question is cash generation relative to market value, especially when earnings quality or accrual accounting needs a second check.

Move to free-cash-flow yield when the main question is cash remaining after reinvestment or capital spending.

Each metric is strongest when it is used for the question it was built to answer. A more defensible valuation comparison often comes from checking numerator quality, denominator fit, peer context, and cash-conversion durability rather than treating any single yield as a standalone conclusion.