Start with the ETF question first. An ETF is an exchange-traded fund that holds a basket of assets and trades on an exchange, but that definition is not enough to compare funds well.

Two funds can both carry the ETF label while giving investors very different exposure, cost structure, trading behavior, distribution pattern, tracking profile, and tax treatment. The useful first step is to separate the question: what the fund owns, how it works, what it costs, how it trades, how it distributes income, and what comparison comes next.

ETF analysis should separate education from fund selection. The same structure can support broad equity exposure, sector exposure, bond exposure, commodity exposure, thematic exposure, factor exposure, active management, or more specialized strategies, but each route needs its own exposure, cost, liquidity, tracking, distribution, and tax review.

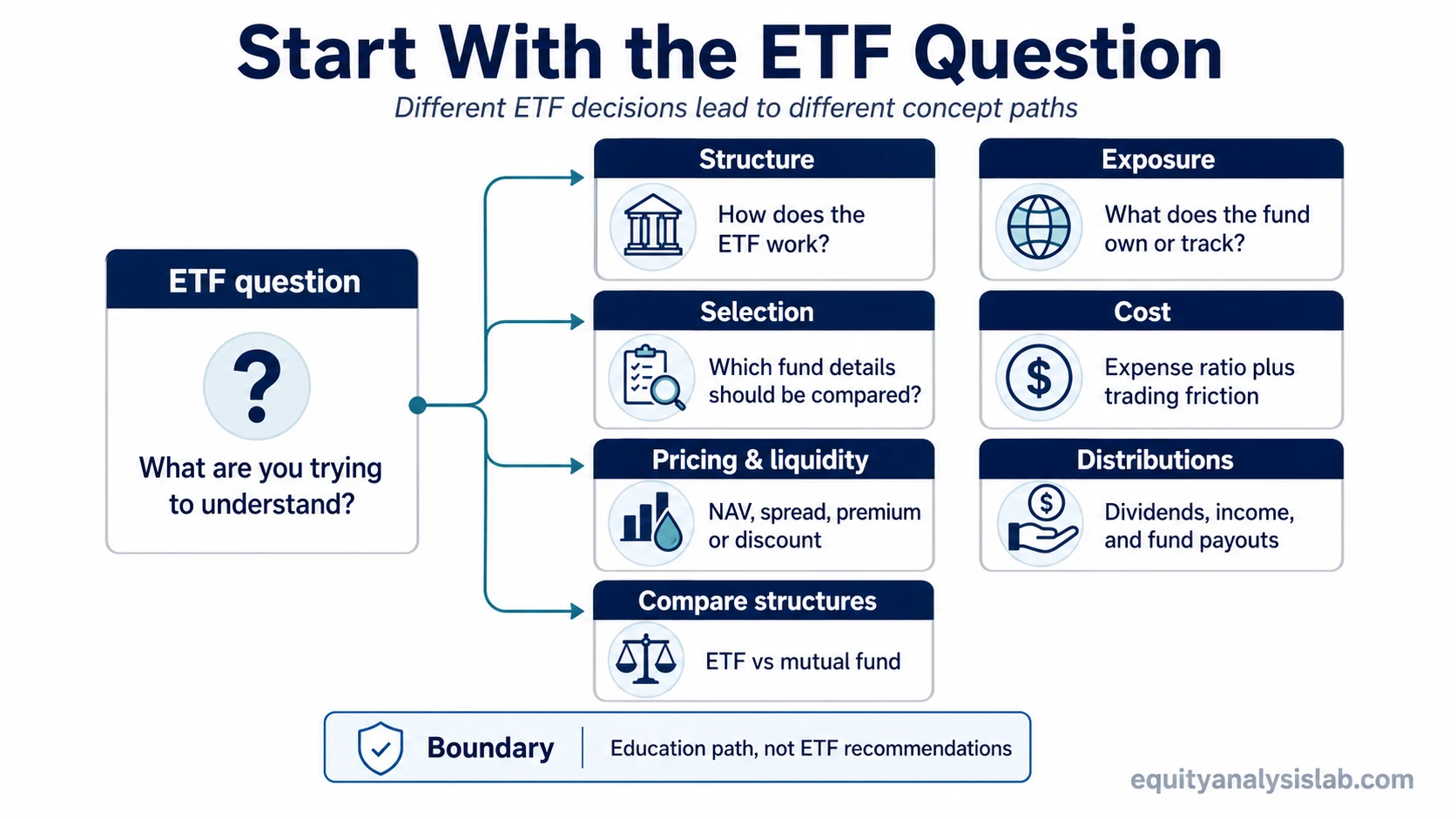

Start with the ETF question

The fastest way to approach ETFs is to match the decision to the right concept before comparing funds side by side.

| Investor question | Start here | Why it matters |

|---|---|---|

| What is an ETF and how does the structure work? | ETF basics | Structure affects how the fund holds assets, trades during the day, and connects market price with underlying value. |

| What exposure does the fund provide? | ETF types | Index, sector, bond, commodity, thematic, factor, and active funds can behave differently even when they all use the ETF format. |

| How should two funds be compared? | ETF selection | Selection depends on holdings, weighting, cost, liquidity, tracking, distributions, and fit with the investor’s objective. |

| What does the fund cost to own or trade? | Expense ratio and bid-ask spread | The stated annual cost is only one part of the investor experience; trading friction can also matter. |

| How closely does the trading price reflect fund value? | NAV and ETF premium or discount | ETF shares trade in the market, so market price and underlying value can temporarily differ. |

| How liquid is the fund? | ETF liquidity | Liquidity depends on the ETF shares, the underlying holdings, market conditions, and the trading spread. |

| How does income, distribution, or tax behavior work? | ETF tax and distribution mechanics | Distributions, dividends, capital gains, and tax treatment can change the after-tax experience. |

| How is an ETF different from another fund structure? | ETF vs mutual fund | The comparison is not only about cost; trading structure, pricing, management style, and distributions can differ. |

What an ETF is, in one sentence

An ETF is a fund that holds a portfolio of assets and trades on an exchange, giving investors a way to access an exposure through a listed fund share.

The structure matters because the ETF share is not the same thing as one stock, one bond, one commodity, or one private portfolio. The fund’s holdings, index or strategy, creation and redemption process, market price, and underlying value all affect how the ETF behaves.

For the full mechanics, start with how ETFs work. The practical question is not only “what is an ETF?” but which part of ETF analysis matters for the decision being made.

Choose the exposure before comparing costs

ETF comparison starts with exposure. A low-cost fund can still be the wrong match if it owns the wrong assets, weights them in the wrong way, tracks a benchmark the investor does not understand, or uses a strategy that behaves differently from the label.

Broad equity index ETFs, sector ETFs, bond ETFs, commodity ETFs, thematic ETFs, factor ETFs, leveraged or inverse ETFs, and an actively managed ETF can all sit under the same ETF umbrella. Their risks are not interchangeable.

Identify what the fund is designed to hold or track before judging whether the fee, liquidity, or distribution pattern fits the investor’s objective.

Use selection criteria after the structure is clear

After the exposure is clear, ETF selection becomes more practical. The comparison can move from the label to the actual fund details: holdings, weighting method, expense ratio, trading spread, liquidity, tracking behavior, distribution history, and tax mechanics.

For a selection workflow, use how to choose an ETF. For side-by-side fund analysis, use how to compare ETFs.

| Check | Question to answer |

|---|---|

| Holdings | What does the fund actually own? |

| Weighting | Are the largest positions driving most of the exposure? |

| Cost | What is the ongoing expense ratio, and are there trading costs to consider? |

| Liquidity | Can the ETF be bought or sold efficiently under normal and stressed conditions? |

| Tracking | How closely does the fund follow the benchmark or strategy it claims to represent? |

| Distributions | How does the fund handle dividends, interest, capital gains, or other distributions? |

Cost is more than the expense ratio

The expense ratio is usually the first cost investors notice, but it is not the only cost-related variable. A fund can have a low stated fee while still creating a worse experience if trading spreads are wide, liquidity is thin, tracking is poor, or the fund structure does not match the investor’s holding period.

Cost analysis should also consider tracking difference and tracking error. Tracking difference looks at the gap between fund return and benchmark return over time, while tracking error focuses on the variability of that gap.

Exact fees, yields, spreads, assets, and performance data are fund-specific. Current details belong in the fund provider materials, prospectus, or official fund documents.

Liquidity and pricing can change the investor experience

ETF shares trade on an exchange, so the quoted market price matters. The spread between the bid and ask price can affect the cost of entering or exiting a position, especially in less liquid funds or unsettled markets.

NAV is the fund’s net asset value. ETF shares can trade near NAV, above it at a premium, or below it at a discount. A premium or discount does not automatically make a fund attractive or unattractive, but it is a signal that market price and underlying value are not identical at that moment.

Liquidity also depends on what the ETF owns. A fund that holds very liquid large-cap stocks is different from a fund that holds less liquid bonds, niche securities, derivatives, or hard-to-trade exposures.

Dividends, distributions, and taxes need their own check

Some ETFs distribute dividends, interest, capital gains, or other income. Others may be designed more for price exposure than income. The distribution pattern can affect cash flow, reinvestment decisions, and after-tax results.

ETF dividends are best reviewed through the fund’s holdings, distribution policy, and payout history. Start with ETF dividends when the question is income, and follow the tax and distribution mechanics path when the question is treatment.

Tax outcomes can vary by fund structure, jurisdiction, account type, holding period, and investor situation. General ETF education is not a substitute for tax advice or current fund documentation.

A simple ETF comparison scenario

An investor comparing two broad-looking ETFs may first notice that one has a lower expense ratio. That is useful, but incomplete. One fund may hold a market-cap-weighted index with heavy concentration in a few large companies, while another may use a different weighting method or a narrower exposure.

The next question decides the next step. If the issue is exposure, the ETF types path matters. If the issue is cost, the expense ratio and spread matter. If the issue is execution, liquidity, NAV, and premium or discount matter. If the issue is income or after-tax result, dividends and distribution mechanics matter.

The same ETF label can hide different holdings, weighting, trading conditions, tracking behavior, and distribution outcomes.

Common ETF mistakes to avoid

An ETF is not automatically safe because it is diversified. Diversification can reduce single-security exposure, but it does not eliminate market risk, sector risk, interest-rate risk, currency risk, liquidity risk, tracking risk, or fund-structure risk.

A broad label is also not enough. “Equity ETF,” “bond ETF,” “dividend ETF,” or “thematic ETF” does not reveal the full portfolio, weighting method, liquidity profile, distribution behavior, or tax effect.

Specific ETF facts should be checked against current provider materials, the prospectus, and official fund documents before making any fund-level decision.

FAQ

Are ETFs the same as stocks?

No. ETF shares trade on an exchange like stocks, but an ETF is a fund that holds a basket of assets. The investor is buying a fund share, not direct ownership of every underlying holding.

Are ETFs always safer than individual stocks?

No. ETFs can reduce single-company exposure when they are diversified, but they still carry risk. The fund’s holdings, concentration, strategy, leverage, liquidity, tracking behavior, and market exposure all matter.

What should be checked before comparing ETFs?

Start with exposure, holdings, weighting, cost, liquidity, tracking, distributions, and tax mechanics. A lower expense ratio is useful, but it is not enough by itself.