ETF discount to NAV means an ETF’s exchange market price is below the value of its underlying portfolio. A premium means the ETF’s market price is above NAV. The gap can reflect trading pressure, liquidity, stale pricing, market hours, transaction costs, or creation and redemption limits, so it should be interpreted with context rather than treated as a standalone bargain or warning.

An ETF has two related but different reference points. Its market price is the price at which ETF shares trade on an exchange. Its NAV, or net asset value, is based on the value of the fund’s underlying holdings after fund-level accounting adjustments.

The premium or discount is the relationship between those two numbers. The useful question is not only whether the ETF is above or below NAV, but why the gap exists and whether the quoted NAV is a reliable comparison point at that moment.

What ETF discount to NAV means

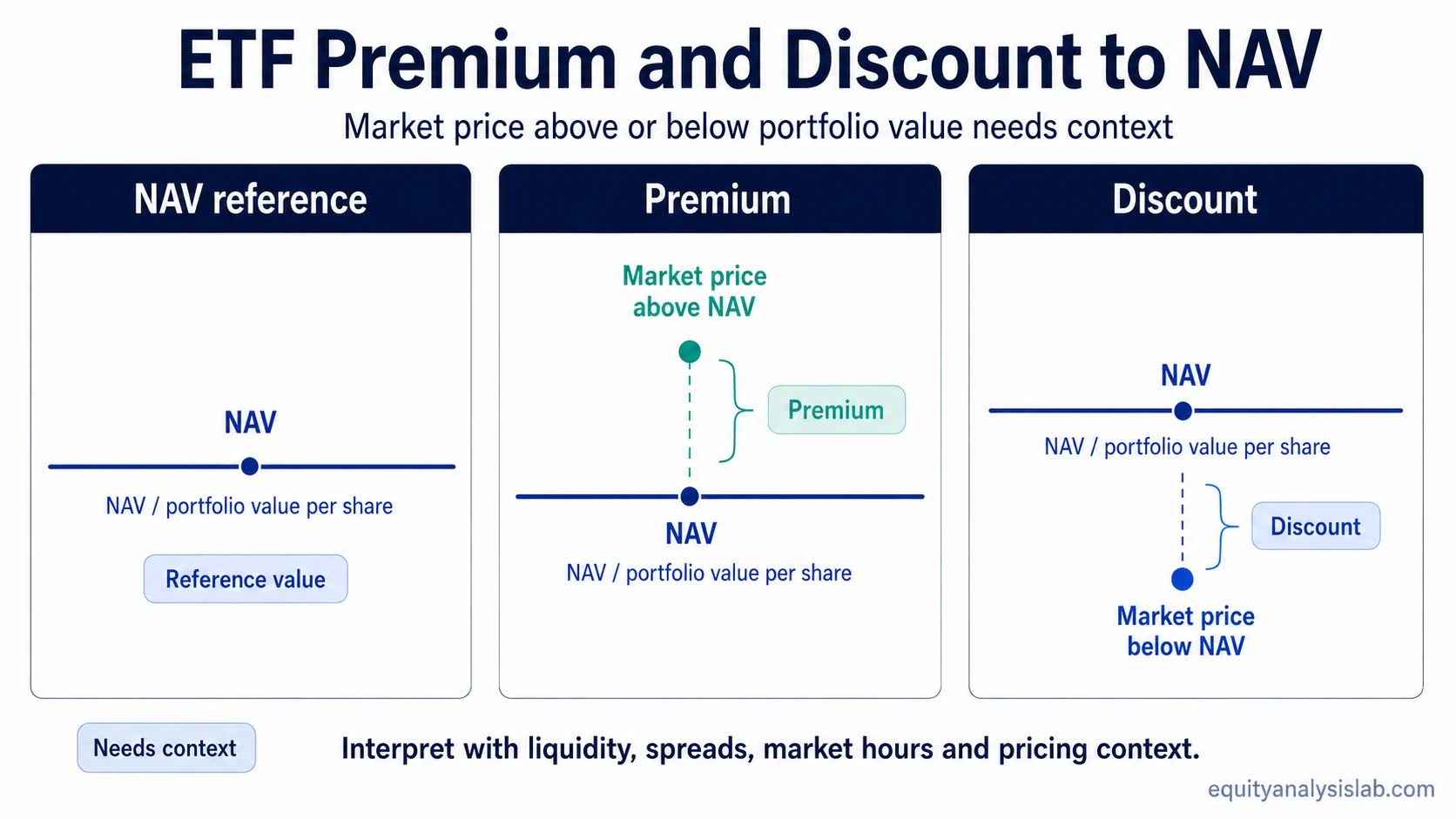

An ETF trades at a discount to NAV when its market price is lower than the per-share value of the fund’s underlying holdings. It trades at a premium when its market price is higher than that value.

- Discount: ETF market price is below NAV.

- Premium: ETF market price is above NAV.

- At or near NAV: ETF market price is close to the fund’s calculated portfolio value.

For example, if an ETF’s NAV is $100 per share and the ETF trades at $99.50, it is trading at a 0.50% discount to NAV. If it trades at $100.50, it is trading at a 0.50% premium to NAV. This example is only a pricing illustration, not a recommendation or evidence that the ETF is attractive or unattractive.

Why ETF prices can trade away from NAV

ETF shares trade continuously on an exchange, while NAV is calculated from the fund’s underlying portfolio. Those two values can diverge because the ETF share price responds to real-time buyers and sellers, while the portfolio value may be based on securities that trade less frequently, close earlier, or require estimated pricing.

A small gap can be normal in many ETFs, especially when the underlying holdings are harder to price intraday. A wider or persistent gap needs more context. It may reflect ETF trading conditions, underlying market conditions, or the limits of the price-discovery process rather than a simple mispricing.

This is why ETF premium and discount analysis belongs with liquidity and structure. The gap means more when it is compared with the ETF’s normal trading pattern, the quality of the underlying market, and the cost of creating or redeeming ETF shares.

What can cause an ETF premium or discount?

Premiums and discounts can come from several sources. Some are temporary trading effects. Others reflect deeper issues in the underlying market or the ETF structure. The same visible gap can have different meanings depending on the cause.

| Cause of premium or discount | What it can imply | What to check before interpreting it |

|---|---|---|

| Short-term ETF supply and demand | Buyers or sellers may be pushing the exchange price away from NAV. | Check whether the gap is brief or persistent, and whether trading volume is unusual. |

| Wide bid-ask spread | The visible trading price may be affected by lower trading depth or higher execution cost. | Review the bid-ask spread, not just the last traded price. |

| Low ETF liquidity | The ETF share price may move more easily because fewer shares are trading at tight prices. | Compare the gap with ETF liquidity, trading volume, and market depth. |

| Stale or estimated NAV | NAV may not fully reflect real-time conditions in the underlying holdings. | Check whether underlying markets are open, closed, illiquid, or using estimated pricing. |

| International market hours | The ETF may trade in one market while some underlying securities are no longer trading. | Compare the ETF trading session with the trading hours of the underlying securities. |

| Fixed-income pricing | Bond prices used in NAV may be estimates, while ETF shares may reflect more current trading pressure. | Check whether the ETF owns bonds or other instruments that may not trade continuously. |

| Creation or redemption frictions | Authorized participants may face costs or constraints that make the gap slower to close. | Review whether market stress, transaction costs, or basket constraints may affect the process. |

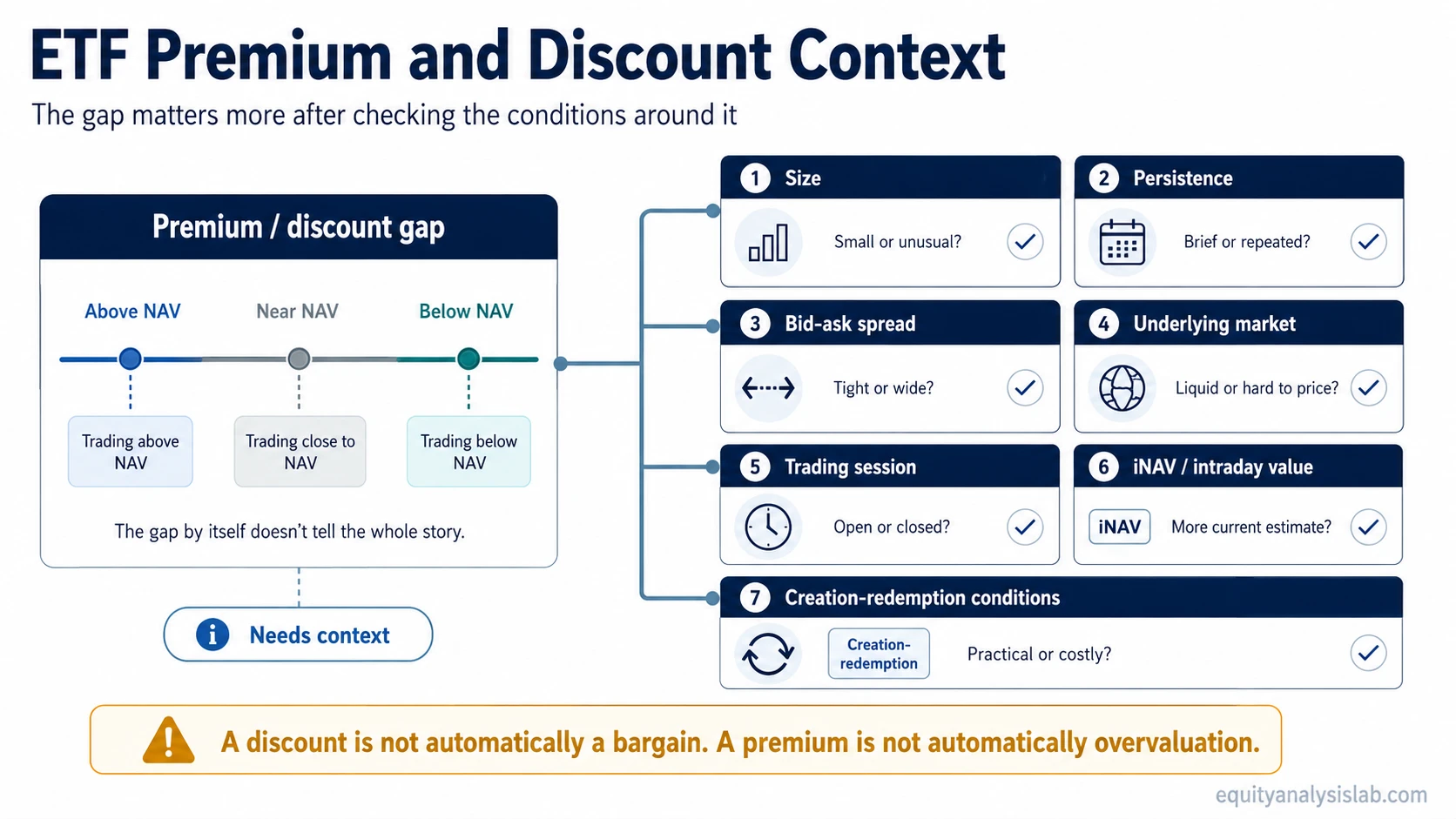

What to check before interpreting the gap

A discount or premium becomes more useful when it is treated as a diagnostic clue rather than a conclusion. Before interpreting the number, check whether the gap is unusual for that ETF, whether the underlying holdings are easy to price, and whether the quoted trading price is reliable.

- Size: A tiny gap may be normal; a larger gap needs context.

- Persistence: A one-day discount means less than a repeated or widening pattern.

- Spread: A wide spread can make the last traded price less informative.

- Underlying market: Bonds, international securities, and less liquid holdings can make NAV less current.

- Trading session: Closed underlying markets can make ETF prices and NAV look temporarily misaligned.

- Intraday value: Where available, iNAV or other intraday value indications can help compare the ETF’s trading price with a more current portfolio estimate.

- Creation/redemption health: The ETF mechanism may help reduce gaps, but only when it is economically practical for participants to act.

The most useful interpretation usually comes from combining the premium or discount with liquidity, spreads, underlying asset class, intraday value information, and the ETF’s normal pattern. A discount that appears during market stress can mean something different from a discount that appears during a calm trading session with tight spreads.

Why a discount is not automatically a bargain

A discount to NAV can look attractive because the ETF appears to trade below portfolio value. That interpretation can be too simple. The discount may exist because the NAV is stale, the ETF is hard to trade, the underlying assets are under stress, or the cost of closing the gap is high.

A premium is not automatically overvaluation either. In some situations, the ETF price may be reflecting newer information than the most recent NAV. This can happen when an ETF trades while some underlying markets are closed or when the portfolio contains securities that do not update continuously.

The safer interpretation is to treat the premium or discount as a question to investigate. The gap shows a relationship between price and reported value; it does not explain the reason by itself.

How creation and redemption affect premiums and discounts

The ETF structure includes a primary-market process called creation and redemption. Authorized participants can create ETF shares by delivering a basket of securities to the ETF issuer, or redeem ETF shares for the underlying basket. This mechanism can help ETF supply adjust when market price moves away from portfolio value.

If an ETF trades at a premium, creating new ETF shares may help increase supply. If an ETF trades at a discount, redeeming ETF shares may help reduce supply. In both cases, the mechanism can support price alignment, but it is not automatic or costless.

ETF arbitrage depends on trading costs, market liquidity, basket access, hedging conditions, and the ability to transact in the underlying holdings. During market stress or when underlying securities are hard to price, premiums and discounts can persist longer than expected.

Example: reading a discount with context

Assume an ETF reports a NAV of $100 and trades at $99.20, showing a 0.80% discount. The first reading is simple: the ETF market price is below the reported portfolio value. The better interpretation asks why.

If the ETF has a tight bid-ask spread, normal volume, open underlying markets, and a discount that is much larger than usual, the gap may deserve closer attention. If the ETF holds bonds or international securities that are not trading actively, the reported NAV may be less current than the ETF market price.

The same 0.80% discount can therefore mean different things. It may reflect temporary trading pressure, stale underlying pricing, poor liquidity, or practical limits in the creation/redemption process. The number is useful only after those conditions are checked.

Where ETF discount to NAV fits in ETF analysis

ETF discount to NAV is one part of ETF structure analysis. It should be read alongside spread, liquidity, underlying holdings, trading session, fund structure, and the ETF’s normal premium/discount history.

For broad, liquid equity ETFs, small premiums or discounts may be routine. For bond ETFs, international ETFs, commodity-linked ETFs, or funds holding less liquid securities, the gap can require more interpretation because NAV may be less current or harder to calculate precisely.

The practical goal is not to label every discount as cheap or every premium as expensive. The goal is to understand whether the ETF’s exchange price is giving a useful real-time signal, whether NAV is a reliable reference, and whether trading conditions make the gap meaningful.

FAQ

Is an ETF discount always a bargain?

No. A discount can reflect stale pricing, weak liquidity, market stress, wide spreads, or creation and redemption friction. It needs context before it can be interpreted.

Why can bond ETFs trade away from NAV?

Bond ETFs can show premiums or discounts because some bonds trade less frequently than exchange-listed ETF shares. NAV may rely on evaluated or estimated bond prices, while the ETF share price can react more quickly to current demand and liquidity conditions.

Why can international ETFs show wider premiums or discounts?

International ETFs can trade while some underlying markets are closed. In that situation, the ETF market price may reflect newer information than the latest NAV calculation for the underlying securities.

Can ETF arbitrage close every premium or discount?

No. Arbitrage can help reduce gaps, but it is not costless or guaranteed. Liquidity, transaction costs, market stress, and underlying basket constraints can weaken the mechanism.